CIO Letter – Apr 2023: Maintaining high cash allocation to seek for safer returns

– – –

Highlights:

#1

Airo-BOCA composite closed March 2023 with +1.52% while MSCI All Country World Index (ACWI) and S&P500 Index (SPX) were up +3.33% and +3.51%, respectively. It’s worth noting that during the bear market rallies, indices tend to outperform as they are fully invested by default. Airo’s current investment strategy, however, warrants maintaining a high level of cash that could provide a safer path for sustainable investment returns.

#2

The U.S banking crisis has resulted in a series of events in the financial markets, from the insolvency of Silicon Valley Bank, Signature Bank, to the acquisition of Credit Suisse by United Bank of Switzerland. As a result, the bond market underwent a swift re-pricing, downplaying the earlier expectations of further rate hikes as becoming a low probability outcome.

#3

Macro growth data continued to point towards further deterioration, with indicators such as Durable Goods Orders, Factory Orders, Empire Manufacturing, Real Retail Sales, ISM Manufacturing, ISM Services and the various Fed Manufacturing & Services indices all experiencing negative plunges. These reaffirmed the current negative macro growth backdrop in the U.S.

#4

On the back of the U.S banking crisis and further weakening of the macro growth trajectory, the rally in the S&P500 during March seemed rather puzzling. One major driver for the rally was the panic rotation of investment flows from the banking sector to the technology sector, which was acting like a defensive proposition.

#5

However, the rally in technology with no fundamental driver on an absolute basis had driven its valuation back to the trailing PE high of 29x, supported by FY2023 EPS growth of a mere +2.7%. The dislocation between the technology sector’s valuation and its forward earnings growth potential becomes even more glaring in the face of macro growth deterioration.

#6

Airo remains optimistic that the broader downtrend in equity markets will eventually reverse, despite the current difficult macro environment. However, we opine that better times are still ahead of us and therefore maintaining a high cash allocation remains a safer option for now from a capital preservation perspective. Rest assured that Airo will continue to seek out and capitalize on potential market mispricing opportunities to generate positive alpha steadily for the BOCA portfolios.

– – –

Dear Valued Investors,

Airo-BOCA composite closed March 2023 with +1.52% while MSCI All Country World Index (ACWI) and S&P500 Index (SPX) were up +3.33% and +3.51%, respectively. Airo’s positive returns in March were mainly driven by the realized profits from the short positions in the China H-Share (FXP) and U.S energy (ERY) sectors. In addition, the core overweight positions in gold (IAU) and miners (GDX, SIL) continued to outperform as expected.

It’s worth noting that during the bear market rallies, indices tend to outperform as they are fully invested by default. Airo’s current investment strategy, however, warrants maintaining a high level of cash that could provide a safer path for sustainable investment returns.

Table 1: Airo-BOCA YTD Performance (in USD) – As of March 2023

Source: Interactive Brokers, Airo Malaysia, Bloomberg.

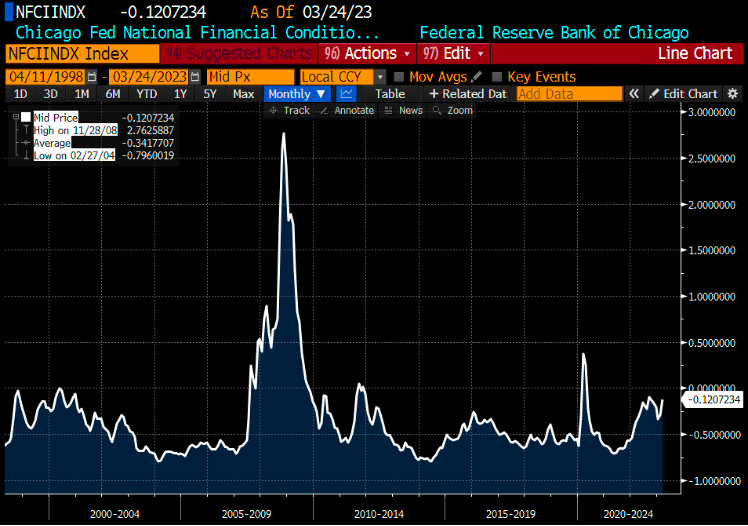

The U.S banking crisis has resulted in a series of events in the financial markets, from the insolvency of Silicon Valley Bank, Signature Bank, to the acquisition of Credit Suisse by United Bank of Switzerland. As a result, the bond market underwent a swift re-pricing, downplaying the earlier expectations of further rate hikes as becoming a low probability outcome. Indeed, the banking crisis could potentially lead to further credit tightening, limiting banks’ lending activities and credit growth going forward. This also implies that the overall financial condition is likely to stall further.

Chart 1: The Chicago Fed National Financial Conditions Index ~ pointing to a potential tightening of financial conditions in the near future

Source: Bloomberg, Airo Malaysia

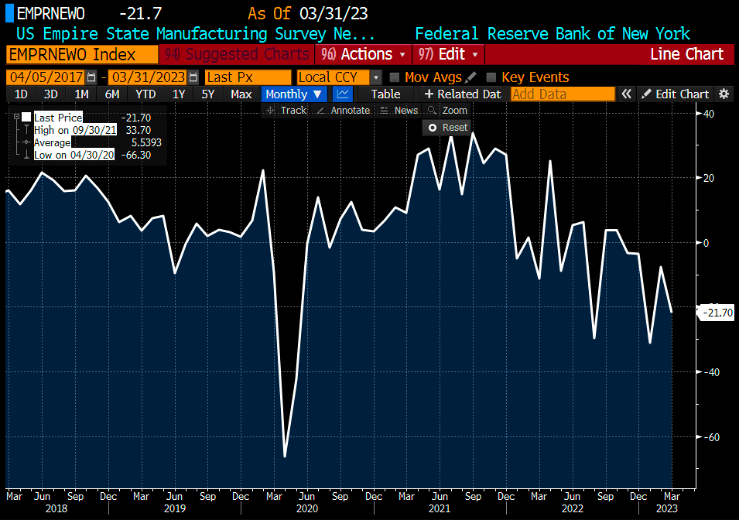

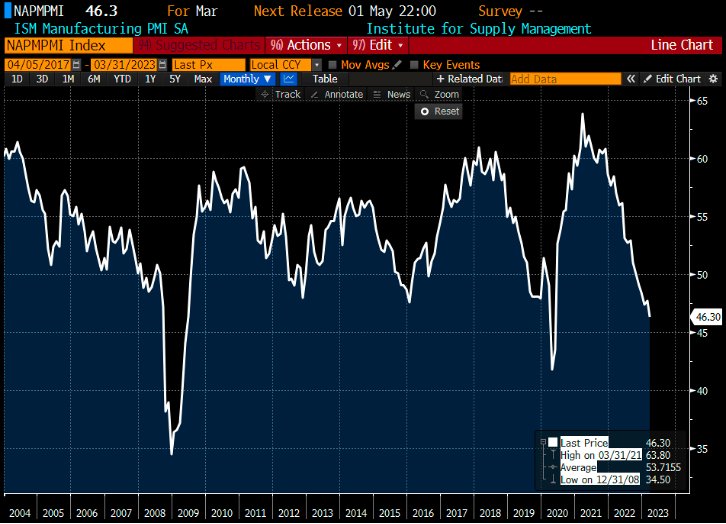

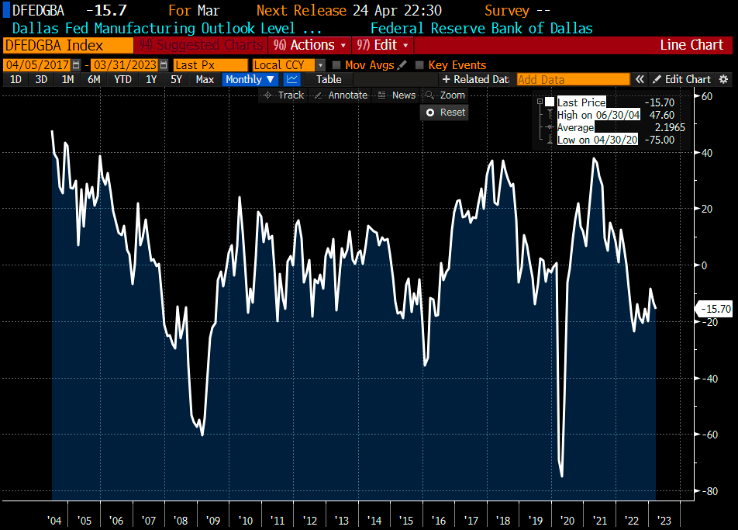

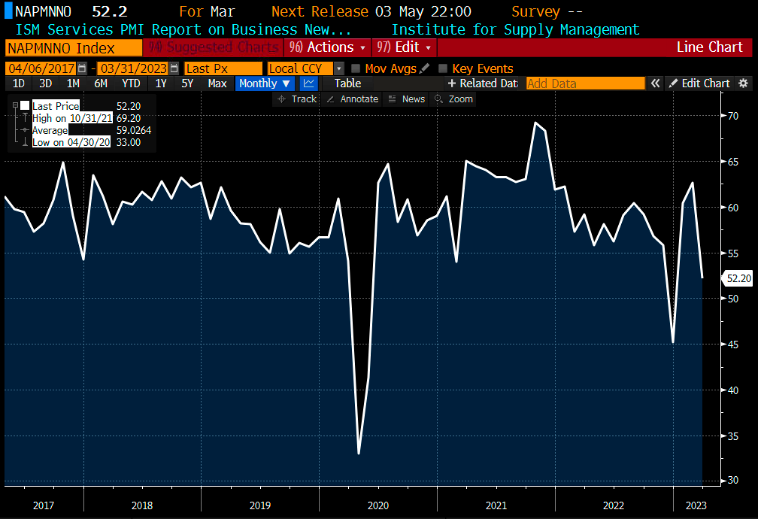

Macro growth data continued to point towards further deterioration, with indicators such as Durable Goods Orders, Factory Orders, Empire Manufacturing, Real Retail Sales, ISM Manufacturing and the various Fed Manufacturing & Services indices all experiencing negative plunges. In fact, ISM Services New Orders PMI saw a big plunge to 52.2 in March from 62.6 in February. The demand stickiness in the services sector is likewise being challenged with the on-going broader macro contraction. These reaffirmed the current negative macro growth backdrop in the U.S.

Chart 2: Empire Manufacturing New Orders ~ negative growth continued

Source: Bloomberg, Airo Malaysia

Chart 3: ISM Manufacturing PMI ~ negative growth continued

Source: Bloomberg, Airo Malaysia

Chart 4: Dallas Fed. Manufacturing Activity ~ plunging outlook continued

Source: Bloomberg, Airo Malaysia

Chart 5: ISM Services New Orders PMI ~ saw a huge plunge to 52.2 from 62.6

Source: Bloomberg, Airo Malaysia

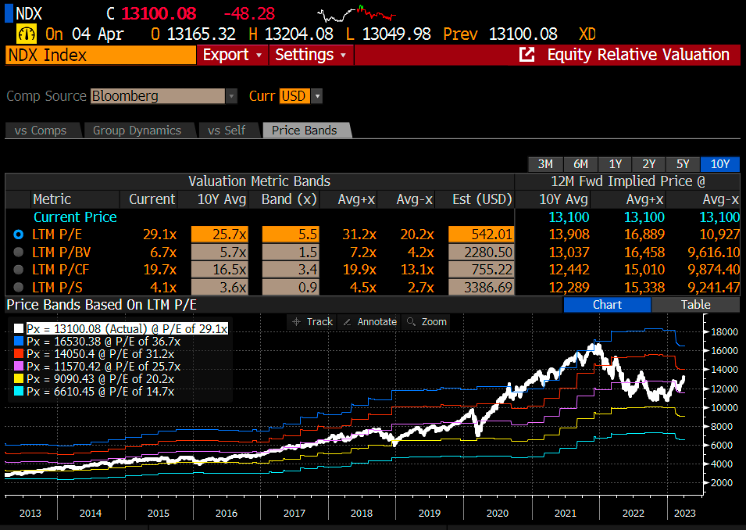

On the back of the U.S banking crisis and further weakening of the macro growth trajectory, the rally in the S&P500 during March seemed rather puzzling. One major driver for the rally was due to the panic rotation of investment flows from the banking sector to the technology sector, which was acting like a defensive proposition. As a result, for the month of March, the Nasdaq100 index outperformed almost +15% relative to the U.S Banking index.

Chart 6: Nasdaq100 outperformed the U.S Banking Index by +15% in March 2023

Source: Bloomberg, Airo Malaysia

However, the rally in technology sector with no absolute fundamental driver had driven its valuation back to the trailing PE high of 29x, supported by FY2023 EPS growth forecast of a mere +2.7%. The dislocation between the technology sector’s valuation and its forward earnings growth expectation becomes even more glaring in the face of macro growth deterioration. As such, Airo continues to see the overvaluation in the technology sector as an asymmetrical risk vs. reward condition to be taken advantage of in the interim.

Chart 7: Nasdaq100’s Valuation ~ back to the high of 29x PE on no absolute fundamental rationale

Source: Bloomberg, Airo Malaysia

Airo remains optimistic that the broader downtrend in equity markets will eventually reverse, despite the current difficult macro environment. However, we opine that better times are still ahead of us and therefore maintaining a high cash allocation remains a safer option for now from a capital preservation perspective.

Rest assured that Airo will continue to seek out and capitalize on potential market mispricing opportunities to generate positive alpha steadily for the BOCA portfolios.

Apr 5th, 2023

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.