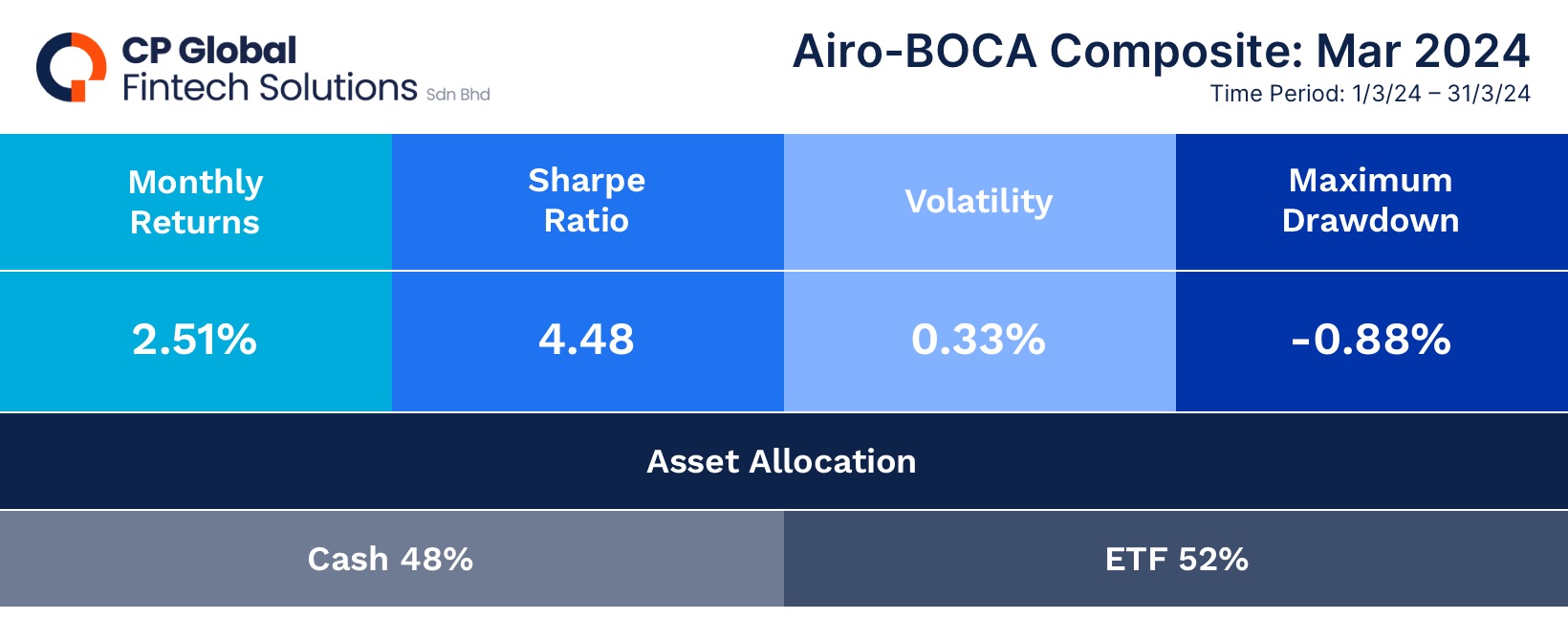

CIO Letter – Apr 2024: +2.51% Airo-BOCA’s Overall Composite Return in March 2024

Highlights:

#1

Gold has been buzzling hot with a +7.92% relentless rally in March, primarily driven by the dovish stance from global central banks, which have begun to reduce interest rates. As a result, holdings in gold and gold miners contributed +1.65% to Airo-BOCA’s overall composite return of +2.51% for March 2024.

#2

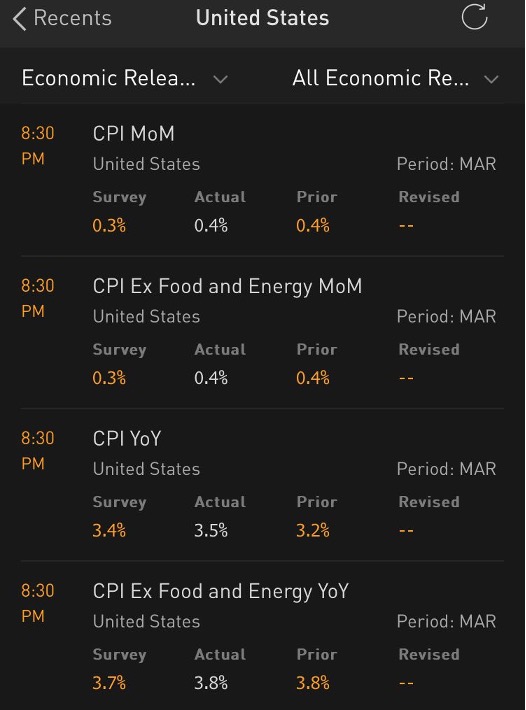

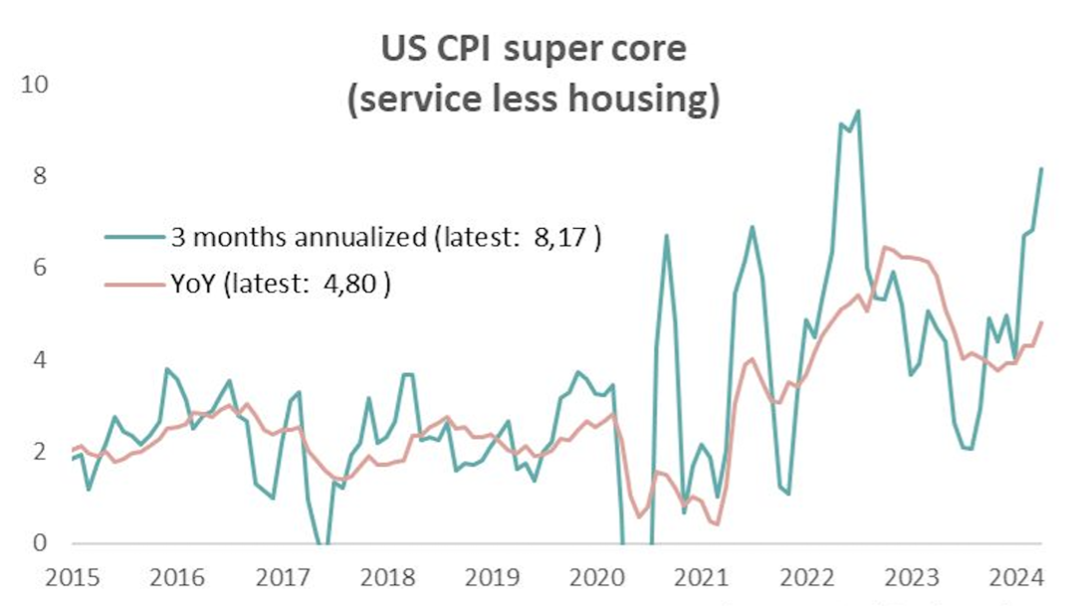

The U.S disinflationary path continues to be volatile, with March registering another higher CPI for the third consecutive month for both the Headline and Core CPI. Furthermore, its Supercore CPI hit a fresh high since bottoming in October 2023.

#3

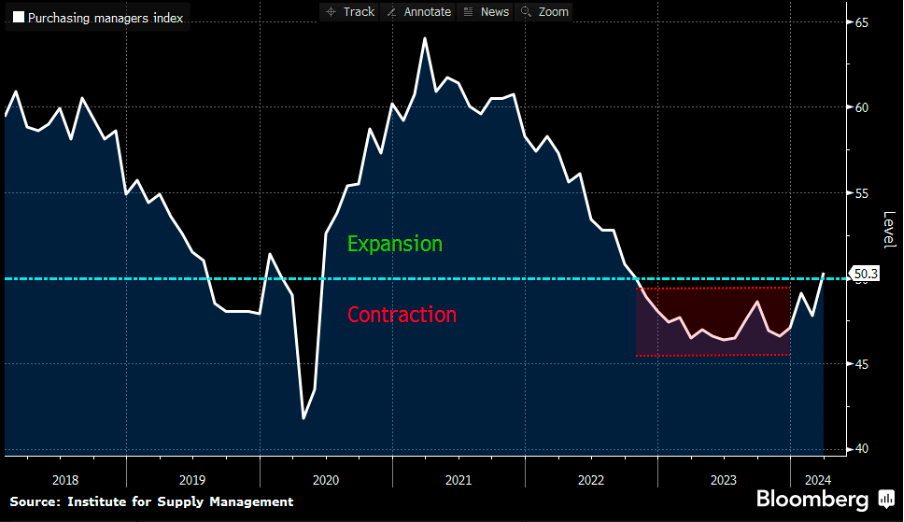

On macro growth front, soft macro data in March presented a mixed picture. The MNI Chicago PMI, Richmond Fed. Manufacturing Index and Dallas Fed. Manufacturing Activity worsened further into contraction. In contrast, the widely monitored ISM Manufacturing PMI shifted back into an expansionary growth for the first time since October 2022.

#4

Amidst the emerging signs of U.S. manufacturing growth and the uncertain trajectory of disinflation, Airo’s strategy continues to be agile in terms of cash deployment, simultaneously maintaining an actively dynamic rebalancing approach during this period.

– – –

Dear Valued Investors,

Gold was the best performing asset in March 2024 as it rallied +7.92% on the back of a dovish interest rate stance by the global central banks. The Swiss National Bank cut its interest rate to 1.50% from 1.75% for the first time since pausing its rate in June 2023. Both Brazil and China also pursued their respective interest rate cuts in March that added to the dovish sentiment with a positive implication to gold, commodities as well as the broader equity markets.

With the stellar rally in gold, Airo-BOCA composite returned +2.51% in March with the bulk of positive return attributed to the holdings in gold and gold miners’ at +1.65%. At the same time, global equity (MSCI ACWI index) and the U.S equity (S&P500) returned +3.26% and +3.10% respectively.

Table 1: AIRO-BOCA Composite ~ Performance Matrix (March 2024)

The U.S disinflationary trajectory continues to be volatile, with March registering another higher consumer price index (CPI) on a year-on-year (YoY) basis for the third consecutive month for both the Headline CPI and Core CPI. On a month-on-month basis, both Headline CPI and Core CPI also remained sticky versus February’s reading.

Furthermore, the U.S’ Supercore CPI (i.e. Core CPI Services ex-housing) hit a fresh high since bottoming in October 2023 at 4.80% YoY. On an annualized basis, the Supercore CPI was even more glaring at +8.17% YoY and denoted the recent renewed strength in the U.S inflationary pressure.

Table 2: U.S Inflation ~ hotter for the third consecutive month

Chart 1: U.S Supercore CPI ~ at a 3-month annualized +8.17% YoY

On macro growth front, soft macro data in March presented a mixed picture. The MNI Chicago PMI (at 41.4 from 44.0), Richmond Fed. Manufacturing Index (at -11 from -5) and Dallas Fed. Manufacturing Activity (at -14.4 from -11.3) all worsened further into growth contraction. In contrast, the widely monitored ISM Manufacturing PMI (at 50.3 from 47.8) has shifted back into an expansionary growth for the first time since October 2022.

Chart 2: ISM Manufacturing PMI ~ an initial green shoot for the U.S manufacturing growth

Amidst the emerging signs of U.S. manufacturing growth and the uncertain trajectory of disinflation, Airo’s strategy continues to be agile in terms of cash deployment, simultaneously maintaining an actively dynamic rebalancing approach during this period.

Apr 12th, 2024

William Yii

CIO, CP Global Fintech Solutions.

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.