CIO Letter – Apr 2025: Embracing Uncertainty in a Resilient Way

Highlights:

#1

Amid renewed concerns over U.S. tariff policy, global financial markets experienced another round of selloffs in March, with the S&P 500 and MSCI ACWI Index declining by -5.75% and -3.67%, respectively. In contrast, China attracted notable rotational inflows, driving the HSCEI Index up by +1.14% over the month.

#2

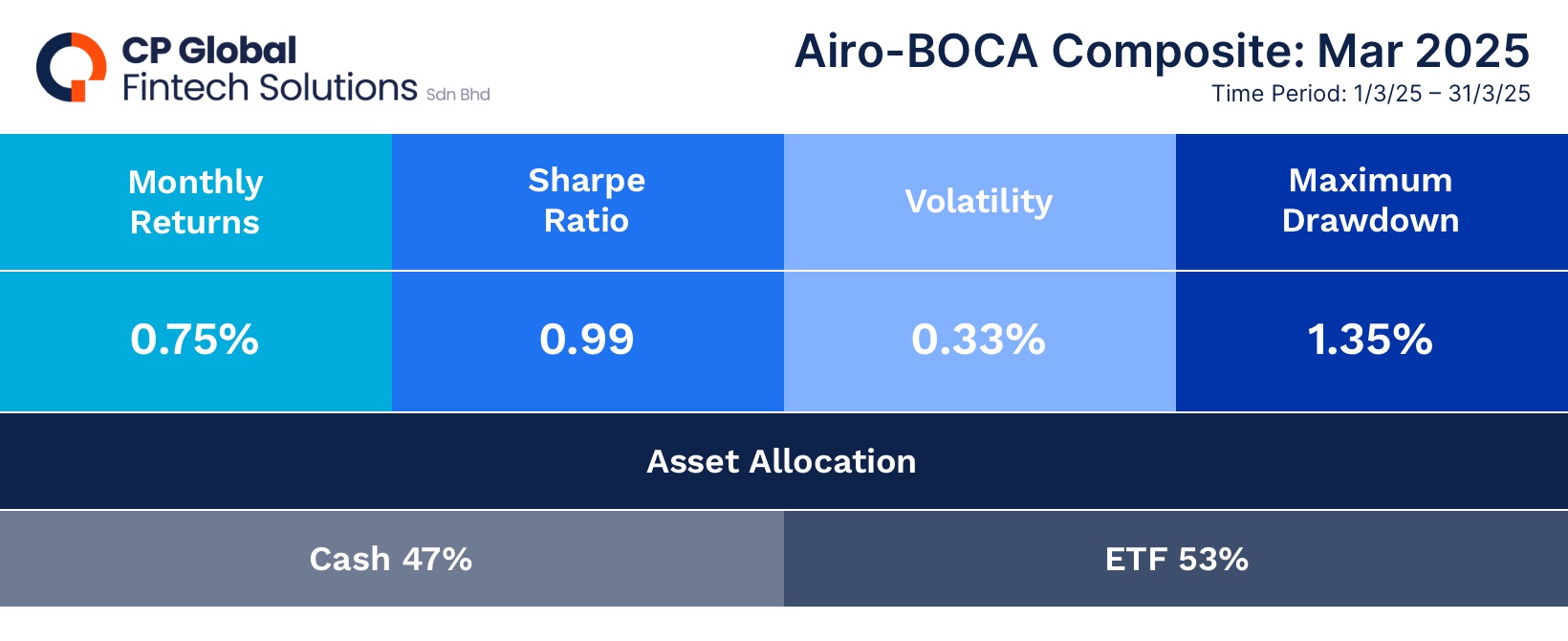

In comparison, the Airo-BOCA Composite outperformed both the S&P 500 and MSCI ACWI, delivering a resilient positive return at +0.75% in March. This absolute and relative outperformance was largely driven by gains in long positions in copper, gold, and gold miners. Meanwhile, the Airo-Shariah Composite posted a return of -3.96%, yet still managed to outperform the S&P 500.

#3

Tariff negotiations between the U.S. and its trading partners continue to progress at a sluggish pace. While recent market corrections have partially priced in the uncertainty surrounding U.S. tariffs, we remain cautious. Financial markets are inherently averse to uncertainty and are unlikely to respond positively until there is greater clarity and tangible progress in negotiations–a process that will take time to materialize.

#4

Persistent inflationary pressures and signs of a macroeconomic recover in Japan have been key drivers behind the Yen’s recent strength. Year-to-date, the JPY has appreciated approximately +11% against the USD. Despite strong economic data and a firmer currency, the interest rate market is not pricing in a rate hike at the upcoming Bank of Japan meeting on May 1st–highlighting a potential disconnect between underlying fundamentals and market expectations.

#5

The U.S. corporate earnings season for Q1 2025 has begun, with banks reporting stronger results, driven by elevated trading revenues amid heightened market volatility. As usual, the technology sector will be in the spotlight, with investors closely watching capital expenditure plans as a key indicator of future growth prospects.

– – –

Dear Valued Investors,

Driven by renewed concerns over U.S. tariffs, global financial markets experienced another wave of selloffs in March, with the S&P 500 and MSCI ACWI Index declining by -5.75% and -3.67%, respectively. In contrast, there were some notable rotational flows into China, where the HSCEI Index posted a gain of +1.14% for the month.

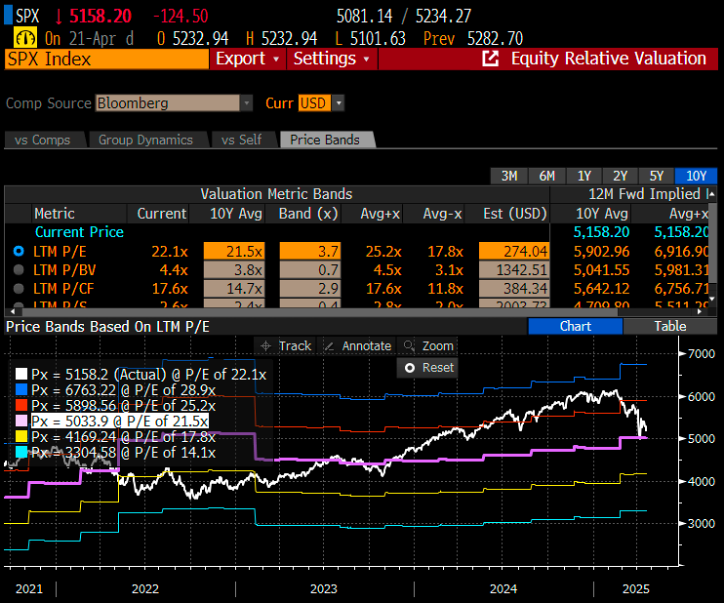

Following the recent market correction, the S&P 500 is now trading at its average price-to-earnings (P/E) valuation within its 10-year historical range. In other words, U.S. equities appear neither overvalued nor undervalued at current levels. However, based on historical precedent, further downside remains possible, particularly if there is no meaningful improvement in macroeconomic or corporate fundamentals in the near term.

Chart 1: After the recent severe correction, S&P500 is trading at the average PE of its 10-year PE bands.

In comparison, the Airo-BOCA Composite outperformed both the S&P 500 and MSCI ACWI, delivering a resilient positive return of +0.75% in March. The absolute and relative outperformance was primarily driven by gains in long positions in copper, gold, and gold miners. Meanwhile, the Airo-Shariah Composite, posted a return of -3.96%, yet still outperformed the S&P 500 over the same period.

Tariff negotiations between the U.S. and other trading partners continue to progress at a slow pace. While recent market corrections have partially priced in the uncertainty surrounding U.S. tariff policies, we remain cautious. Financial markets are inherently sensitive to uncertainty and are unlikely to respond positively until there is greater clarity and concrete progress in negotiations–something that may take time to materialize.

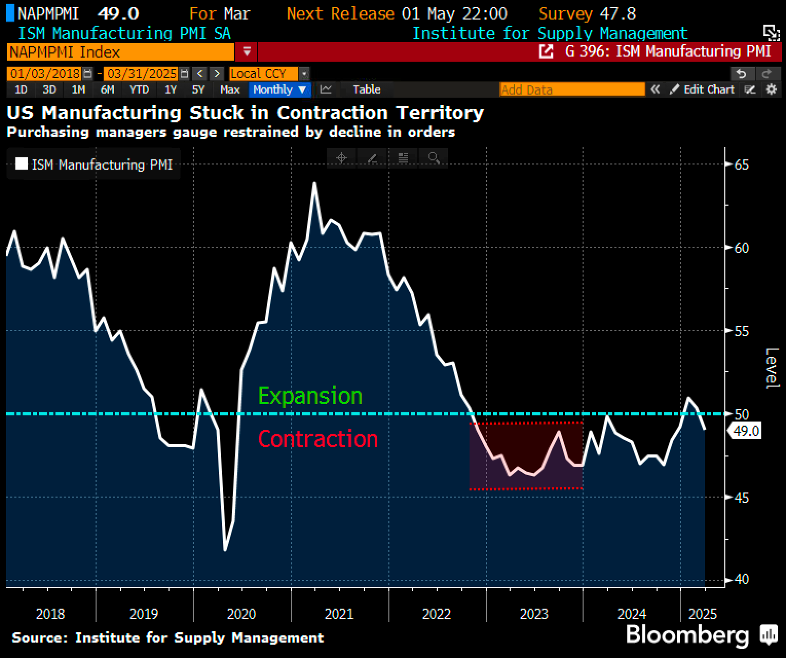

From a macroeconomic perspective, the U.S. Manufacturing PMI has slipped back into contraction after a brief return to expansion in recent months. This signals a potential further deterioration in forward-looking manufacturing activity, especially as tariff implementations begin to take effect in the coming months–assuming no meaningful resolution is reached.

Chart 2: ISM Manufacturing PMI slipped into contraction again

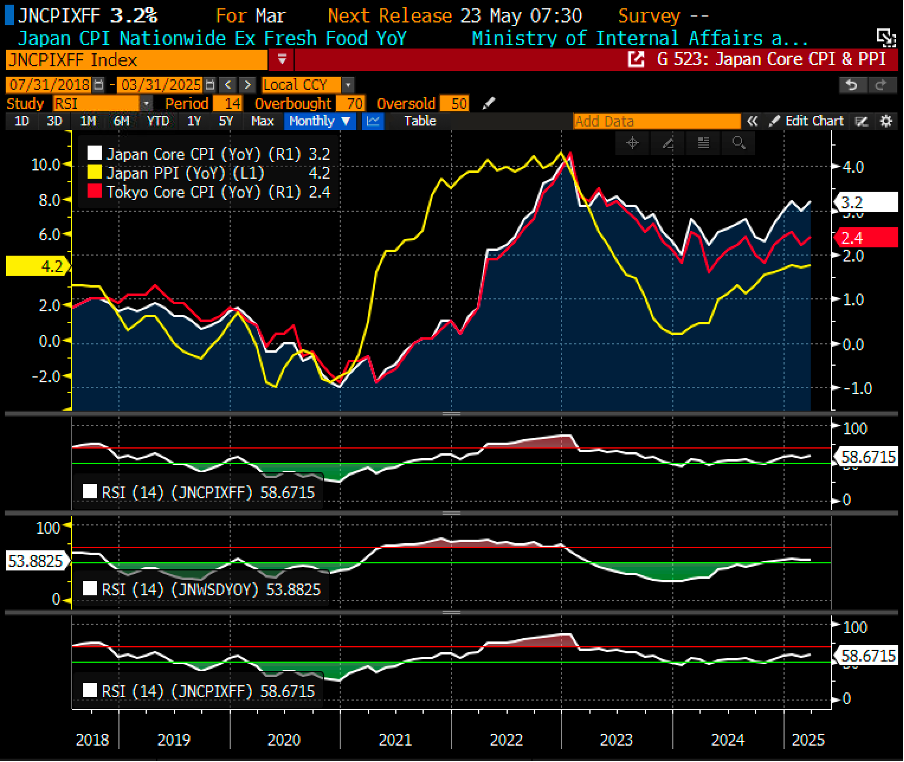

The persistent inflationary pressures in Japan, coupled with a recovering macroeconomic outlook, have been the key drivers of the strengthening Yen. Year-to-date, the JPY has appreciated by approximately +11% against the USD. Despite the strong inflation, growth data, and currency movement, however, the interest rate market does not anticipate a rate hike at the upcoming Bank of Japan (BOJ) decision on May 1st. This creates a potential misalignment between fundamental factors and market expectations, suggesting a risk of a selloff in Yen carry trades if the BOJ were to unexpectedly hike the interest rate in May.

Chart 3: Japan, Tokyo Core CPI & PPI are getting hotter in March 2025

On the micro front, the U.S. corporate earnings season for Q1 2025 has begun, with banks reporting stronger earnings driven by heightened trading revenues and volatile financial markets. However, the technology sector will once again be the main focus. Market participants are expected to closely monitor the capital expenditure plans of tech companies, as these may offer valuable insights into their future growth prospects.

Given that the Nasdaq 100 is currently trading slightly above its 10-year average P/E ratio, it is neither considered expensive nor cheap at this point. However, disappointing earnings results and weaker forward guidance remain key risk factors that could trigger further market corrections.

Chart 4: Nasdaq100 is trading right above the average PE of its 10-year PE bands

April 23rd, 2025

William Yii

CIO, CP Global Fintech Solutions

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.