Aug 2022: Staying nimble, alert and flexible

Highlights:

#1

Due to the paper loss in our hedging positions, Airo-BOCA composite closed the month of July at -3.35% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) at +7.07% and +9.11% respectively. However, on a YTD basis as of July, Airo-BOCA composite maintained its positive return at +0.75% versus ACWI & SPX at -15.09% & -13.34% respectively.

#2

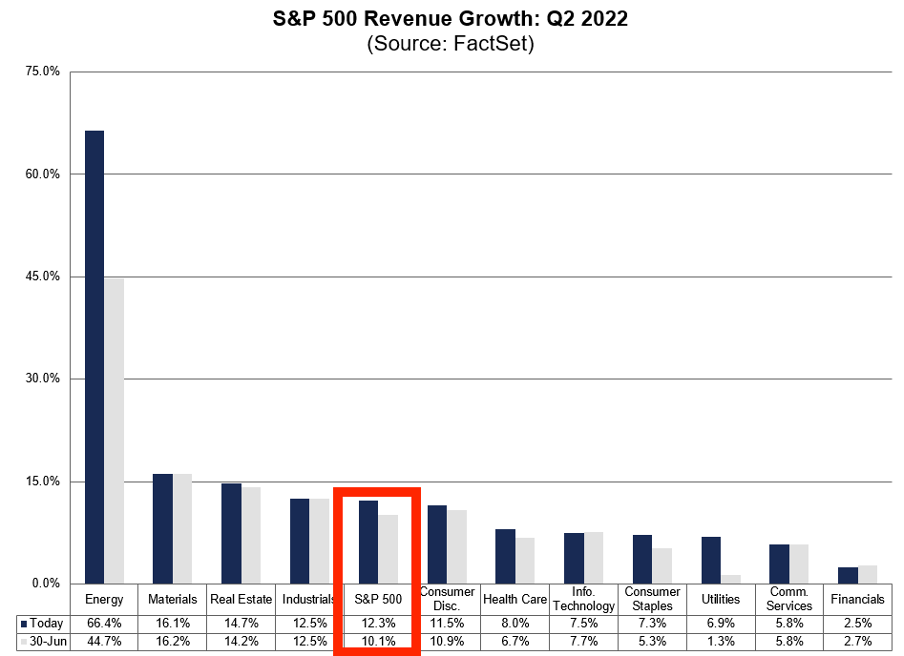

The strong “bear market rally” was initially due to a lower inflationary expectation priced into by the market as the U.S Federal Reserve continued front-loading its rate hike. Subsequently, the rally continued as S&P500 managed to report a year-on-year revenue growth of 12.3% for 2Q2022.

#3

The bond market is currently pricing in the likelihood of inflation pressure falling faster in the coming months. If this turns out to be correct, it will likely cause the U.S Federal Reserve to slow down on the interest rate hike path.

#4

On the growth trajectory, concerns remain as various macro indicators are still pointing to lower incoming growth. Importantly, S&P Global U.S Composite PMI has plunged into contraction mode at 47 while Philadelphia Fed.’s Business Outlook worsened to -12.3 from -3.3. Lastly, Dallas Fed. Manufacturing activities also deteriorated further to -22.6 from -17.7.

#5

As we maintain that macro growth will remain non-conducive, Airo shall keep the current high level of cash for capital preservation and to be deployed at the right time as mentioned previously. Tactical hedging shall also continue as an overall strategy to secure potential positive alpha for the portfolios.

Dear Valued Investors,

During a protracted bear market period, major markets tend to stage strong counter rallies. July 2022 was one of those periods where Airo-BOCA composite closed the month at -3.35% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) at +7.07% and +9.11% respectively. However, on a YTD basis as of July, Airo-BOCA composite maintained its positive return at +0.75% versus ACWI & SPX at -15.09% & -13.34% respectively.

Table 1: Airo-BOCA YTD Performance As Of July 2022

The strong “bear market rally” was initially due to a lower inflationary expectation priced by the market as the U.S Federal Reserve continued front-loading its rate hike effort. Subsequently, the rally continued as S&P500 managed to report a year-on-year revenue growth of 12.3% for 2Q2022.

Chart 1: The flattish inflation expectation in July 2022 had helped the rally

Source: Bloomberg, Airo Malaysia

Chart 2: S&P500 managed a 12.3% year-on-year revenue growth in Q2 2022

Source: Factset, Airo Malaysia

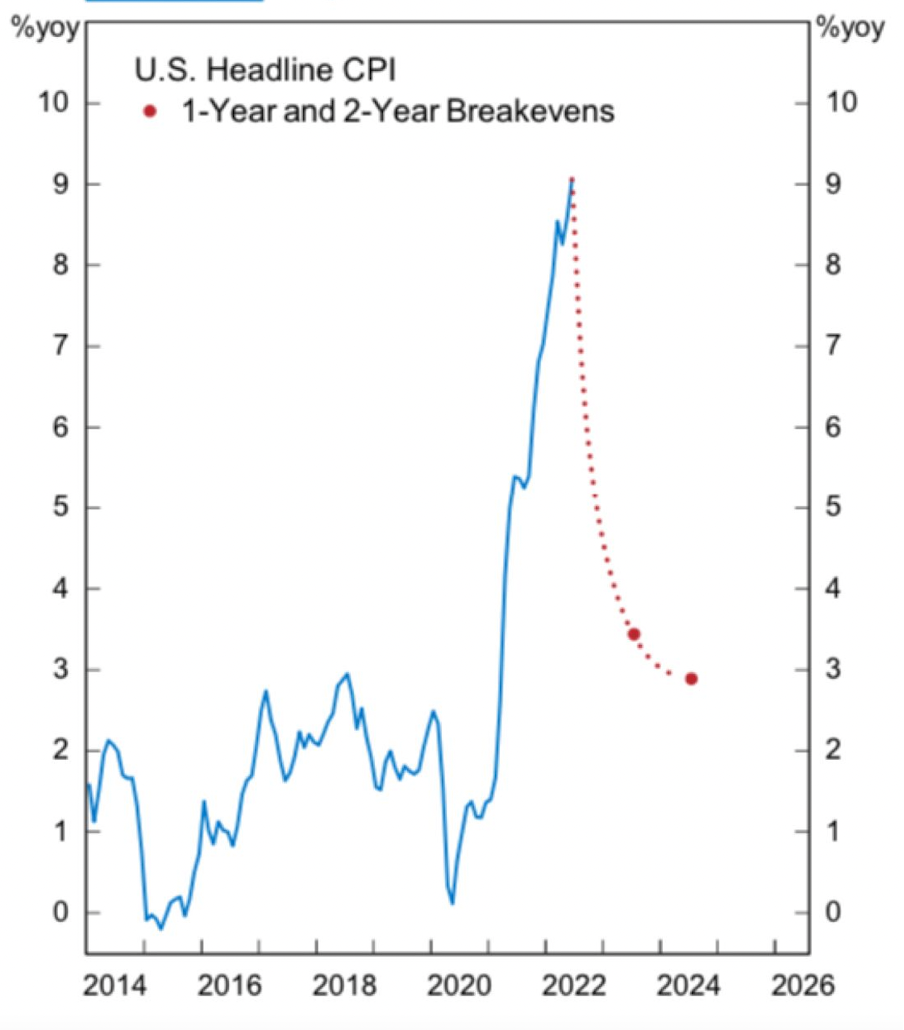

The bond market is currently pricing in the likelihood of inflation pressure falling faster in the coming months. If this turns out to be correct, it will likely cause the U.S Federal Reserve to slow down on the interest rate hike path. The following chart shows that the path of U.S inflation as projected by the bond market is implying that inflation may likely fall sharply sooner than later, rightly, or wrongly!

Chart 3: Projected path of U.S. CPI inflation currently expected by the bond market

Source: AlpineMacro, Airo Malaysia

On the growth trajectory, concerns remain as various macro indicators are still pointing to lower incoming growth. Importantly, S&P Global U.S Composite PMI has plunged into contraction mode at 47 while Philadelphia Fed.’s Business Outlook worsened to -12.3 from -3.3. Lastly, Dallas Fed. Manufacturing activities also deteriorated further to -22.6 from -17.7.

Chart 4: S&P Global U.S Composite PMI plunging into contraction mode at 47

Source: Bloomberg, Airo Malaysia

As we maintain that macro growth will remain non-conducive, Airo shall keep the current high level of cash for capital preservation and to be deployed at the right time as mentioned previously. Tactical hedging shall also continue as an overall strategy to secure potential positive alpha for the portfolios.

Aug 3rd, 2022

William Yii

CIO, Airo Malaysia

{kind=link}