CIO Letter – Aug 2023: Equity valuation remains lofty!

– – –

Highlights:

#1

For July 2023, Airo-BOCA composite was up +0.58% while MSCI All Country World Index (ACWI) and S&P500 Index (SPX) were up +3.60% & +3.11% respectively. Airo’s positive performance was mainly attributed to the rebound in China & gold sectors.

#2

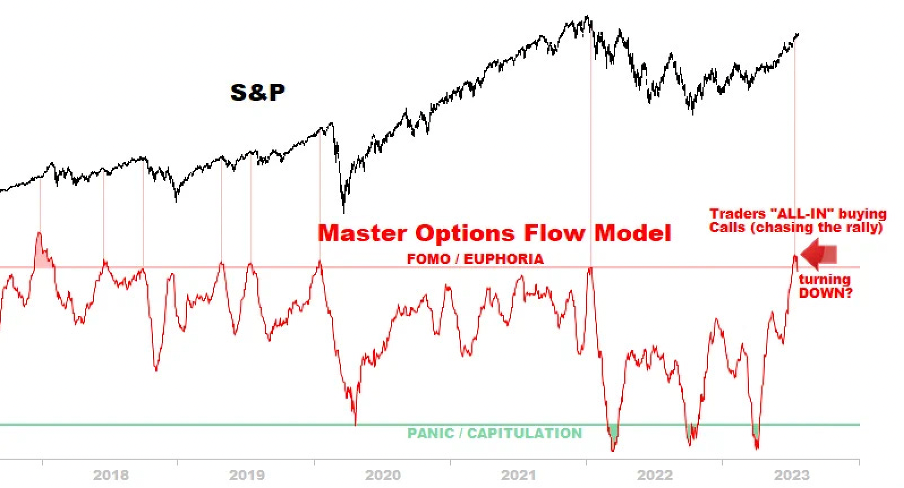

The valuation of U.S equity, particularly within the S&P 500, continues to appear elevated, given that: (i) S&P 500’s earnings yield vs. U.S Treasury 10-Year yield is at historical low since 2005, indicating a potential overvaluation; and (ii) S&P 500 call options positioning has reached a Euphoric level, suggesting a highly optimistic market sentiment that may not be grounded in fundamentals.

#3

For the second quarter (2Q) U.S reporting season thus far, approximately 80% of the companies within the S&P500 have reported earnings per share (EPS) that surpassed expectations, signaling a positive surprise. However, this optimism is tempered by the fact that the blended year-on-year revenue growth for these companies is around a mere +0.1%.

#4

Separately, Fitch downgraded the U.S sovereign credit rating one notch from AAA to AA+. The move was based on the recent tax cuts and new fiscal spending initiatives, which are anticipated to negatively impact U.S finances over the next three years.

#5

Airo is committed to maintaining agility in its overall asset allocation strategy to uphold the capital preservation of your investments. By constantly monitoring market conditions and adapting to changes, we aim to protect and sustain the value of your investments.

– – –

Dear Valued Investors,

For July 2023, Airo-BOCA composite was up +0.58% while MSCI All Country World Index (ACWI) and S&P500 Index (SPX) were up +3.60% & +3.11% respectively. Airo’s positive performance was mainly attributed to the rebound in China & gold sectors.

Table 1: On a year-to-date basis, Airo-BOCA returned -2.50% (As of July 2023)

Source: Interactive Brokers, Airo Malaysia, Bloomberg.

As it stands, the valuation of U.S equity remains elevated, given that the S&P500’s earnings yield vs. U.S Treasury 10-Year yield is at historical low since 2005. This means U.S equity valuation is expensive relative to the U.S government’s bond yield. Moreover, S&P500 call options’ positioning is at the Euphoric level with an outsized of call-options long positions. These matrixes imply that the forward expected return’s potential may not be as conducive as one might project.

Chart 1: S&P500’s earnings yield ~ at historical low vs. the U.S Treasury 10-Year yield since 2005

Source: The Daily Shot.

Chart 2: S&P500’s Call Options Positioning ~ at the Euphoric level

Source: The Macro Chart

For the second quarter (2Q) U.S reporting season thus far, approximately 80% of the companies within the S&P500 companies have reported earnings per share (EPS) surprises. However, the blended year-on-year revenue growth is only around a mere +0.1%. For U.S equities to rally further given the lofty valuation, absolute earnings improvement may be needed to underpin & justify the market’s valuation.

Separately, Fitch just downgraded the U.S sovereign credit rating one notch from AAA to AA+. The move was based on the recent tax cuts and new fiscal spending initiatives, which are anticipated to negatively impact U.S finances over the next three years. Although this may not have an immediate repercussion to the U.S equity market given its economic resiliency, it nonetheless highlighted how the U.S market is well-supported due to a plentiful fiscal stimulus’ driven liquidity that warranted Fitch’s downgrade.

Airo is committed to maintaining agility in its overall asset allocation strategy to uphold the capital preservation of your investments. By constantly monitoring market conditions and adapting to changes, we aim to protect and sustain the value of your investments.

August 4th, 2023

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.