CIO Letter – Aug 2024: Heightened Volatility Incoming

Highlights:

#1

Following the Bank of Japan’s unexpected interest rate hike on 31st July, a massive wave of Yen (JPY) short covering has triggered heightened volatility across global currency, bond, and equity markets over the past few weeks.

#2

Given that the Yen has been heavily borrowed for investments outside Japan (i.e. a practice known as ‘carry trade’), this has partly fueled the stellar rally in the U.S technology stocks. Looking ahead, the Yen’s forward trajectory could continue to impact global volatility, as Yen carry trades may still have further room to unwind.

#3

Airo-BOCA posted a composite return +0.64% in July, with positive contributors from fixed income, gold, and Yen exposures. In comparison, the S&P500 and MSCI ACWI Index gained +1.13% and +1.54%, respectively, during the same period.

#4

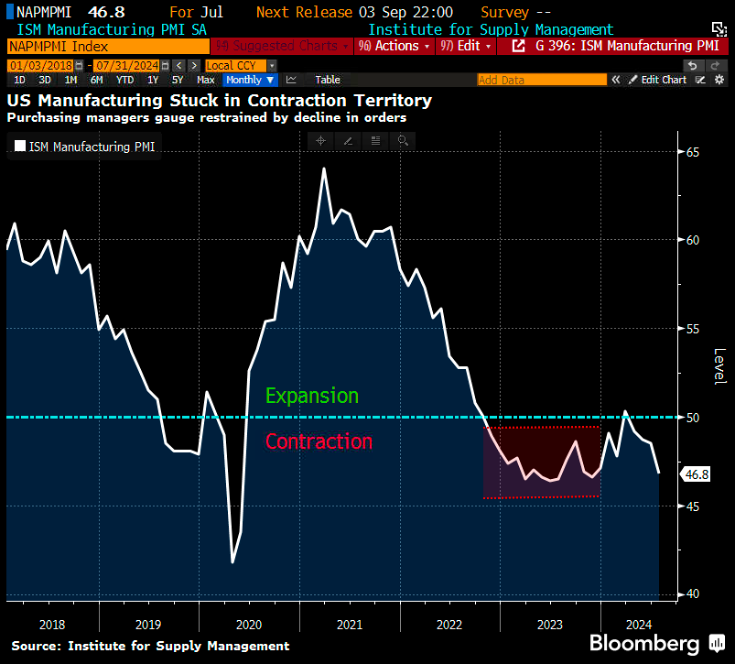

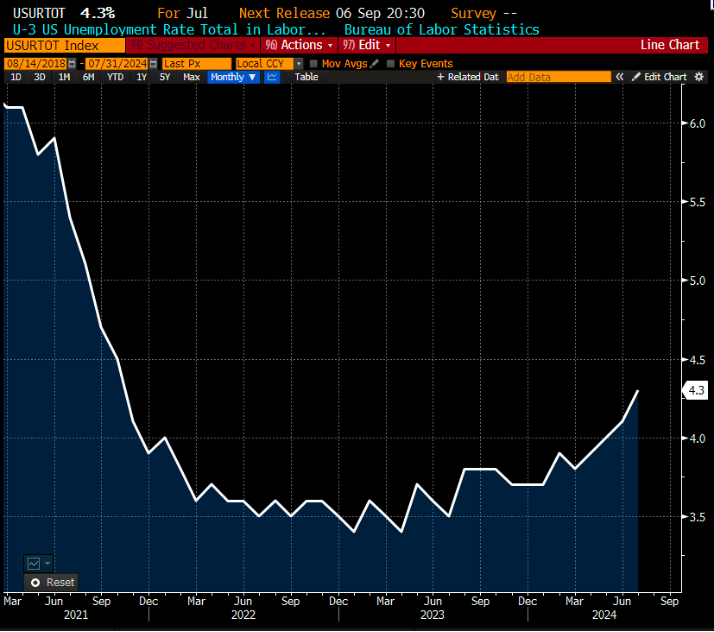

On the macroeconomic front, the ISM Manufacturing PMI recorded its fourth consecutive month of contraction in July, signaling that the U.S manufacturing growth has returned to a contractionary path. This aligns with the downward trend reflected in U.S nominal yields, real yields, and copper. Additionally, the labour market showed signs of weakness, with the unemployment rate spiking to 4.3% in July.

#5

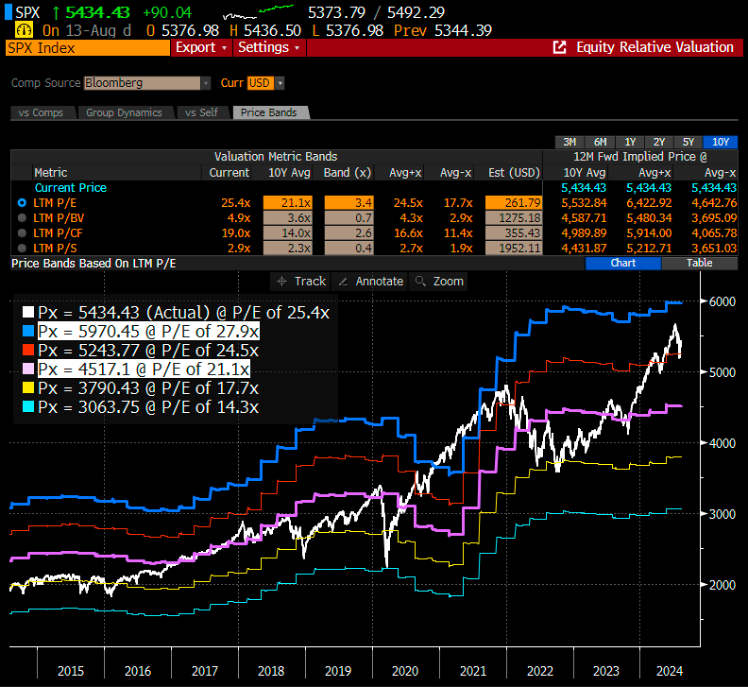

Overall, the U.S big technology companies reported a mixed revenue growth for Q2 2024. Microsoft, Amazon, Alphabet, and Meta led the pack with double-digit revenue growth, while Apple and Tesla posted more modest single-digit growth. On the other hand, equity valuation remains pricey although the S&P500 has started to correct from its 2-standard deviation 10-Year PE band above the mean.

#6

Amid increasing volatility driven by macroeconomic growth deterioration, Airo remains agile with its overall equity exposure and continues to diligently implement tactical hedging strategies.

– – –

Dear Valued Investors,

Following the Bank of Japan’s (BOJ) unexpected interest rate hike on 31st July, a massive wave of Yen (JPY) short covering has triggered heightened volatility across global currency, bond, and equity markets over the past few weeks. The Yen was shorted at historic levels by the hedge fund community just a few weeks ago. However, the BOJ’s unexpected interest rate hike and shift to a more hawkish stance quickly triggered a sharp appreciation of the Yen against other global currencies, resulting in an unprecedented wave of JPY short covering.

Chart 1: Massive Yen (JPY) short-covering trades ~ over the past weeks

Consequently, JPY appreciated by +7.2% against the USD in just five trading sessions. This event also triggered short covering in other heavily shorted currencies, such as the MYR, which appreciated by +4.8% against the USD. Simultaneously, a massive selloff occurred in global equities, with the Nikkei225, S&P500 and MSCI ACWI correcting by -20%, -7%, and -8%, respectively. In response to this risk-off environment, U.S. Treasuries rallied across the entire yield curve.

Given that the Yen has been heavily borrowed for investments outside Japan i.e. a practice known as ‘carry trade’, this has partly fueled the stellar rally in the U.S technology stocks on a year-to-date (YTD) basis. However, since the actual amount of Yen carry trades is largely unknown, moving ahead, the Yen’s forward trajectory may continue to impact global volatility, as Yen carry trades may still have further room to unwind.

Chart 2: Yen short covering ~ triggered a wipe-out of Nikkei225’s YTD positive performance.

In July, Airo-BOCA posted a composite return of +0.64% with positive contributors from fixed income, gold, and Yen exposures. In comparison, the S&P500 and MSCI ACWI Index gained +1.13% and +1.54%, respectively, during the same period.

Table 1: Airo-BOCA July 2024 Performance (in USD)

On the macroeconomic front, the ISM Manufacturing PMI recorded its fourth consecutive month of contraction in July, signaling that the U.S manufacturing growth has returned to a contractionary path. This aligns with the broken uptrend as seen in U.S nominal yields, real yields, and copper. In a nutshell and from a big picture perspective, a broken uptrend of yields and copper signifies a reversal in the global macro growth trajectory. Lastly, the labour market weakness also confirmed the negative manufacturing outlook as the unemployment rate spiked again to 4.3% in July.

Chart 3: U.S ISM Manufacturing PMI ~ fourth consecutive month of contraction.

Chart 4: U.S 10-Year Benchmark Yield ~ 2023’s uptrend decisively broken in July 2024

Chart 5: U.S Unemployment Rate ~ continued to spike to 4.3% in July.

Overall, the U.S big technology companies reported a mixed revenue growth for Q2 2024. Microsoft, Amazon, Alphabet, and Meta led the pack with double-digit revenue growth of +15%, +10%, and 14%, respectively, while Apple and Tesla posted more modest single-digit growth of +5% and +2%, respectively. On the other hand, very importantly, equity valuation remains pricey although S&P500 has started to correct from its +2-standard deviation 10-Year PE band above the mean.

Chart 6: S&P500 remains pricey ~ only just started to correct from its 2-sigma above the mean

Amid the increasing volatility driven by of macroeconomic growth deterioration, Airo remains agile with its overall equity exposure and continues to diligently implement tactical hedging strategies.

August 14th, 2024

William Yii

CIO, CP Global Fintech Solutions

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.