Dec 2022: Maintaining our strategic positions to capitalise opportunities on the horizon

Highlights:

#1

Airo-BOCA composite closed November with -0.59% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) with +8.34% and +5.38% respectively. Airo’s negative return in November was again due to the hedging positioning. On a YTD basis as of November 2022, Airo-BOCA composite returned -3.44% but outperformed ACWI & SPX at -15.21% & -14.39% respectively.

#2

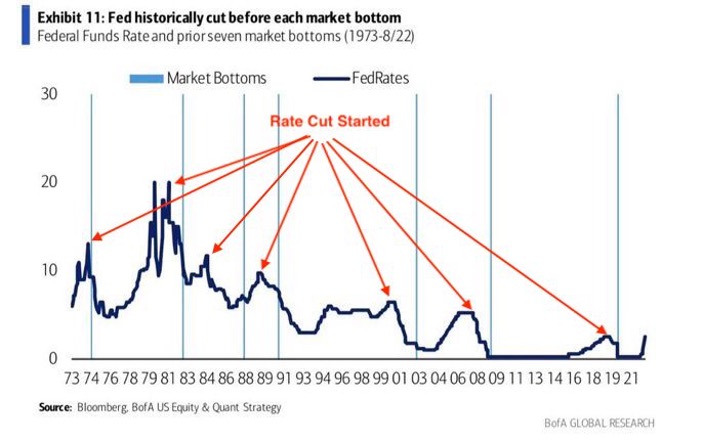

November saw equity markets rallying on the expectation of the Fed. to pivot on interest rate hikes. The rationale for this expectation was based on a relatively softening CPI as reported in the 2nd week of November. However, we maintain that the strong rally in October & November remains a bear-market-rally as equity markets never bottomed until after the Fed. had started to cut interest rates for a period of time!

#3

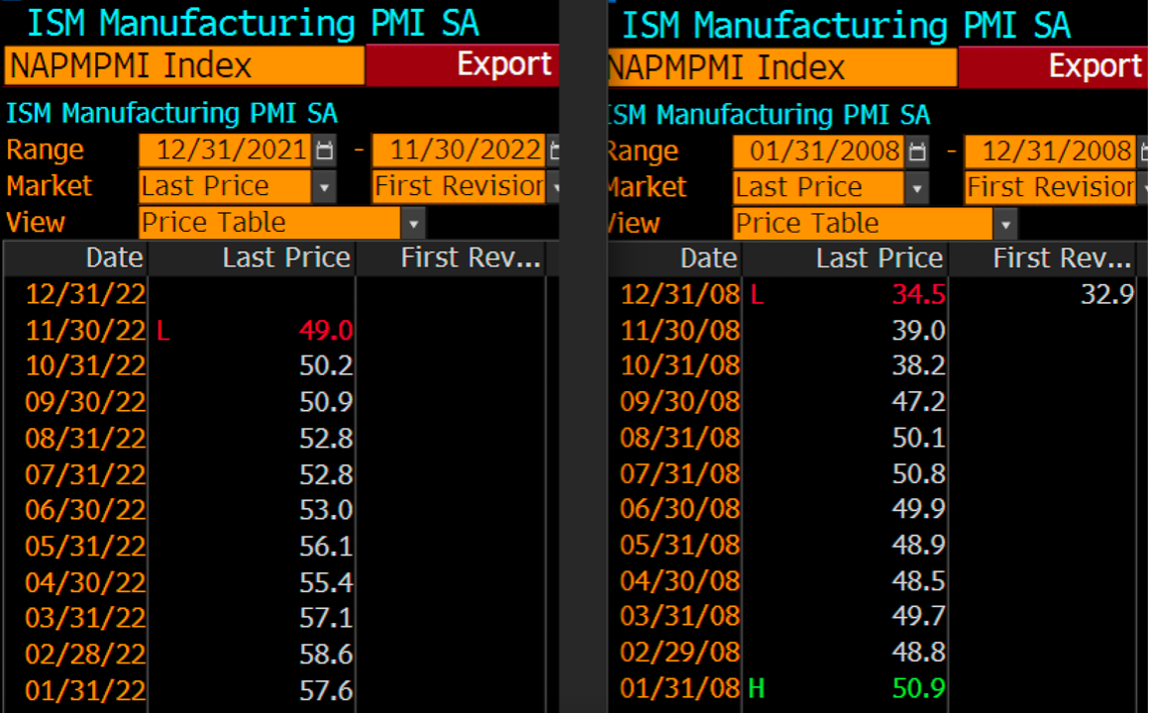

More importantly, on the macro growth front, ISM Manufacturing PMI dipped into contraction mode i.e. a negative growth for the first time since March 2020. Given that the Fed. remains on the rate hike tightening cycle well into the 1H 2023, macro growth contraction is expected to continue.

#4

Under the current no rate-cuts scenario using 2008 as an example, ISM Manufacturing PMI first dipped into contraction mode in February 2008 and did not bottom until December 2008. During that period, S&P500 corrected another -40% before bottoming in November 2008, i.e. one month ahead of ISM Manufacturing bottoming.

#5

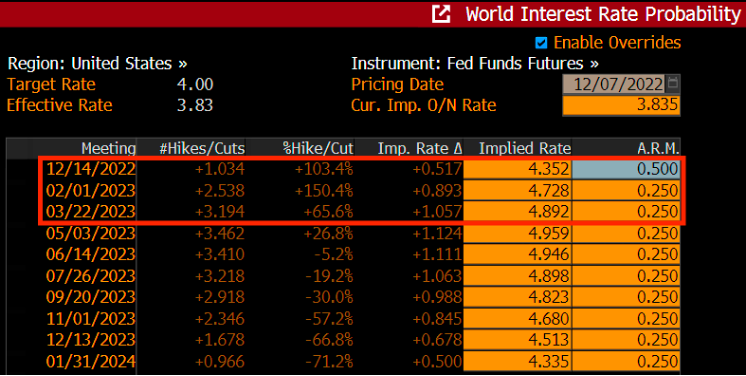

Next week’s FOMC will be a tricky one as Powell sounded dovish during his 30th November’s speech on a tamer CPI & PCE. However, given the recently released strong Non-Farm Payroll & strong employment still, Powell needs to decide his narrative carefully!

#6

Given a potentially less interest rate hike expectation, however, Airo continues to maintain the tactical hedging allocation in view of a wavering macro growth condition that we believe will become the center of the market’s narrative sooner rather than later.

– – –

Dear Valued Investors,

Airo-BOCA composite closed November with -0.59% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) with +8.34% and +5.38% respectively. The negative return in November was again solely due to the hedging positioning. On a YTD basis as of November 2022, Airo-BOCA composite returned -3.44% but outperformed ACWI & SPX at -15.21% & -14.39% respectively.

Table 1: Airo-BOCA YTD Performance – As of November 2022

Source: Interactive Brokers, Airo Malaysia.

November saw equity markets rallying on the expectation for the Fed. to pivot on interest rate hikes. The reason for this expectation was based on a relatively softening CPI as reported in the 2nd week of November. However, we maintain that the strong rally in October & November remains a bear-market-rally. Why? From a historical interest rate hike cycle’s perspective, equity markets had never bottomed until after the Fed. started to cut interest rates for a period of time! And, on average since 1970s, U.S equity only bottomed 11 months after the first rate cut! The rationale behind this dynamic is such that the Fed. would tend to cut interest rates when the economy plunges into a deflationary regime. A deflationary regime means low inflation with a confirmed negative macro growth. A period of rate cuts could then work by reflating the economy where equity markets would price-in its bottom accordingly.

Chart 1: U.S equity market consistently bottomed only after rate cut cycle started for a period of time

Source: Bloomberg, BofA Global Research, Airo Malaysia

Chart 2: S&P500 rallied to another lower high within its bear market downtrend

Source: Bloomberg, Airo Malaysia

Very importantly, on the macro growth front, ISM Manufacturing PMI dipped into contraction mode i.e. a negative growth for the first time since March 2020. Given that the Fed. remains on the rate hike tightening cycle well into the 1H 2023, macro growth contraction is expected to continue. Under the current no rate-cuts scenario using 2008 as an example, ISM Manufacturing PMI first dipped into contraction mode in February 2008 and did not bottom until December 2008. During that period, S&P500 corrected another -40% before bottoming in November 2008, i.e. one month ahead of ISM Manufacturing bottoming.

Table 2: ISM Manufacturing PMI bottomed after 11 months’ of contraction in 2008

Source: Bloomberg, Airo Malaysia

The upcoming December’s FOMC will be a tricky one for the Fed. as Powell sounded dovish during his 30th November’s speech on a tamer CPI & PCE data. However, given the recently release of strong Non-Farm Payroll & strong employment data, Powell needs to decide his narrative carefully! Interest rate futures is currently pricing in a 0.50% hike in December followed by another two rate cuts to bring the Fed. fund rate to around 4.90% by March 2023. Market also expects the interest rate to remain constant until the subsequent 1st rate cut in November 2023.

Table 3: Interest rate futures is pricing in another 3 hikes to bring the Fed. fund rate to 4.90% before pausing with the subsequent 1st rate cut expected in November 2023

Source: Bloomberg, Airo Malaysia

Given a potentially less interest rate hike expectation, however, Airo continues to maintain the tactical hedging allocation in view of a wavering macro growth condition that we believe will become the center of the market’s narrative sooner rather than later. Rest assured that Airo’s portfolios remain strategically positioned to capitalize what is yet to come.

Dec 7th, 2022

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.