CIO Letter – Dec 2023: 🛟 Remaining Cautious Amidst Global Equity Rallies

Highlights:

#1

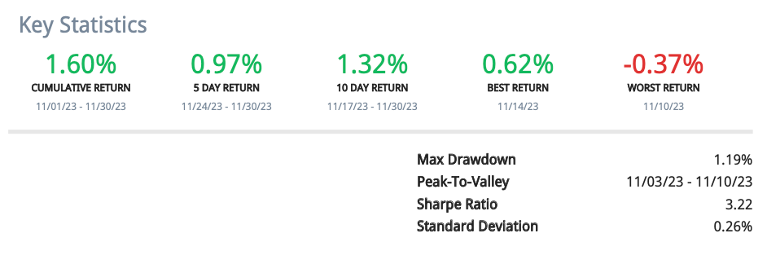

Airo-BOCA composite gained +1.60% in November 2023. This performance seems modest as compared to the MSCI All Country World Index (ACWI) and S&P500 Index (SPX), which returned +8.89% and +3.20% respectively. Airo’s lower return was due to the high cash holding and the hedging position initiated recently.

#2

Global equity markets rallied strongly in November due to the bond and interest markets pricing-in a substantial likelihood of interest rate cuts starting in June 2024. However, we maintain a cautious stance that the equity market may have overdone in its rally pertaining to the expectation of incoming rate cuts.

#3

Interest rate cuts generally appear favorable for equity valuations. However, earnings growth remains the single most important factor for equity prices. In the face of a slowing macro growth, forward equity earnings’ growth trajectory could likewise be challenged.

#4

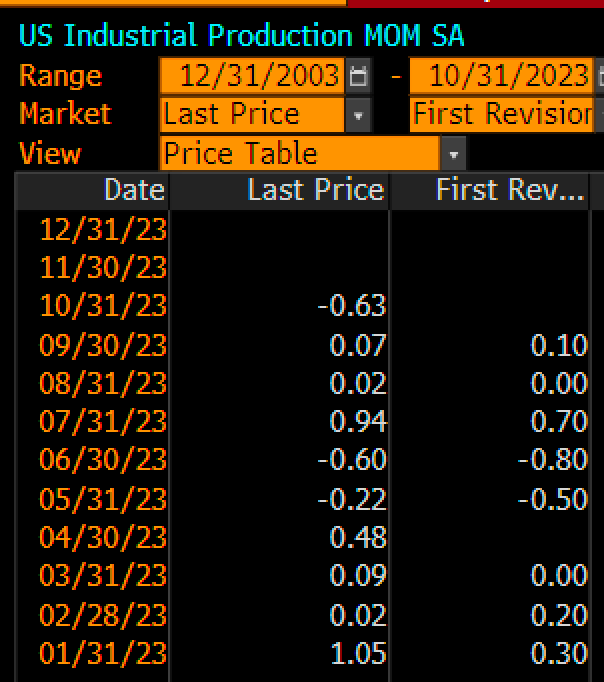

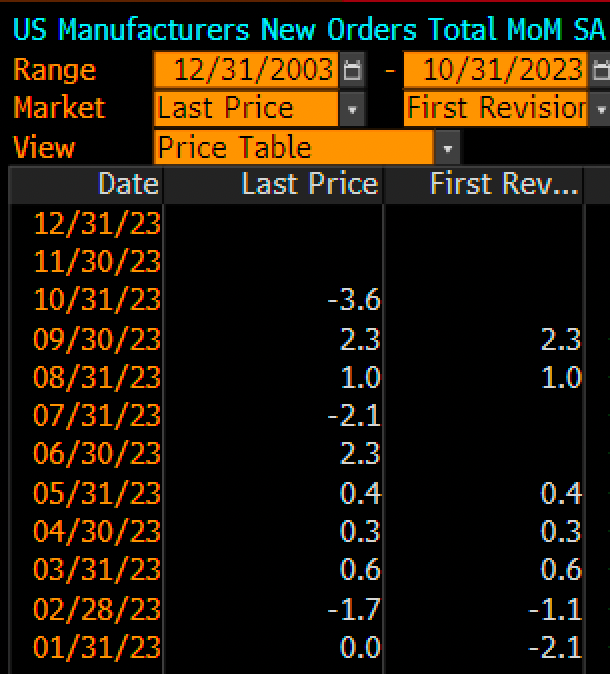

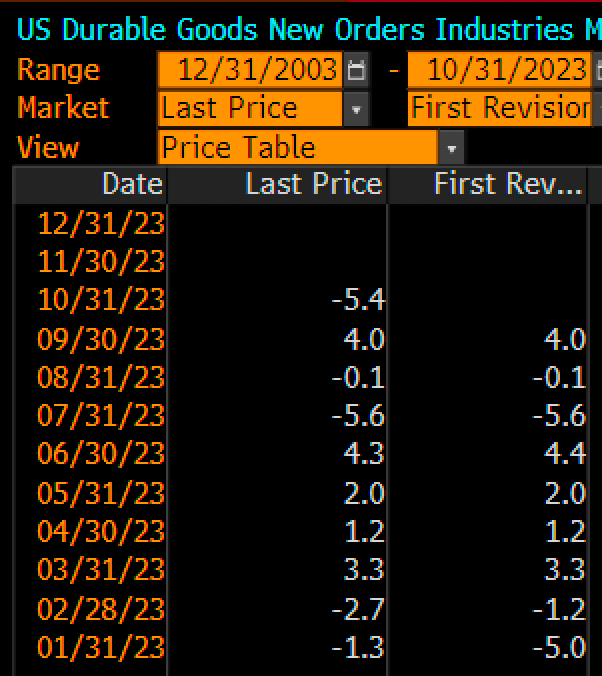

Indeed, U.S’ key macro growth data turned for the worse in October. Industrial Production saw another contraction since June. Factory Orders unexpectedly dropped into contraction mode while Durable Goods Orders resumed its contraction with a big plunge. Airo is mindful of the worsening macro conditions that could translate into negative repercussions for equity earnings growth trajectory going forward.

#5

At Airo, our primary objective extends beyond merely outperforming benchmarks on a relative basis. More importantly, we endeavor to achieve sustainable, long-term positive absolute returns for our investors. In short, our strategic and tactical asset allocations are carefully tailored and managed with this specific objective in mind.

Dear Valued Investors,

For the month of November 2023, Airo-BOCA composite gained +1.60%. This was a modest performance as compared to the MSCI All Country World Index (ACWI) and S&P500 Index (SPX) that returned +8.89% & +3.20% respectively. Airo’s lower return was due to the high cash holding and the hedging position initiated recently. The main positive contributors for the month were the investments in the U.S Treasuries, U.S technology sector and gold while the main detractor was the hedging position against the U.S technology sector.

Table 1: AIRO-BOCA Composite Return ~ November 2023

Global equity markets rallied strongly in November due to the bond and interest markets pricing-in a substantial likelihood of interest rate cuts starting in June 2024. Specifically, the U.S 10Y treasury yield plunged to 4.3% by the end of November from 4.9% at the end of October. This drastic move in yield signified a significant re-pricing of rate cut expectation in November. Despite this, we maintain a cautious stance that the equity market may have overdone in its rally pertaining to the expectation of incoming rate cuts for now.

Chart 1: U.S Treasury 10 Year Yield ~ plunged from 4.9% to 4.3% by the end of November

Any sort of interest rate cut by itself generally appears to be positive for equity valuations and hence the recent equity rally in anticipation of any incoming rate cuts. However, as we lamented previously, earnings growth remains the single most important factor for equity prices. Although the lower the interest rate, the higher the equity valuation should be, if the earnings growth is not positive then the assumption of a sustained higher equity valuation would be challenged in due course. As such, ceteris paribus, interest rate cuts may not necessarily be positive for the equity markets assuming a negative earnings growth scenario.

Indeed, U.S key macroeconomic data turned for the worse in October. Industrial Production dropped -0.6% MoM from +0.3% in September. Factory Orders unexpectedly dropped -3.6% MoM from +2.8% in September while Durable Goods Orders resumed its negative growth with a big plunged to -5.4% MoM. Airo is mindful of these worsening macroeconomic data that could potentially translate into a broader corporate earnings’ negative growth trajectory moving forward.

Table 2: U.S Industrial Production ~ saw a new contraction since June 2023

Table 3: U.S Factory New Orders ~ saw a new contraction since July 2023

Table 4: U.S Durable Goods Orders ~ resuming its contraction with a big plunge!

At Airo, our primary objective extends beyond merely outperforming benchmarks on a relative basis. More importantly, we endeavor to achieve sustainable, long-term positive absolute returns for our investors. In short, our strategic and tactical asset allocations are designed & managed so that the investment portfolios could serve the very purpose of wealth preservation & capital appreciation.

Dec 11th, 2023

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.