CIO Letter – Dec 2024: U.S. Equity’s Optimism Continues Cautiously

Highlights:

#1

U.S. equities posted their strongest performance in November 2024, fueled by sustained optimism surrounding Trump’s election victory. The S&P 500 and MSCI ACWI indices surged by +5.73% and +4.03%, respectively, reflecting broad market confidence.

#2

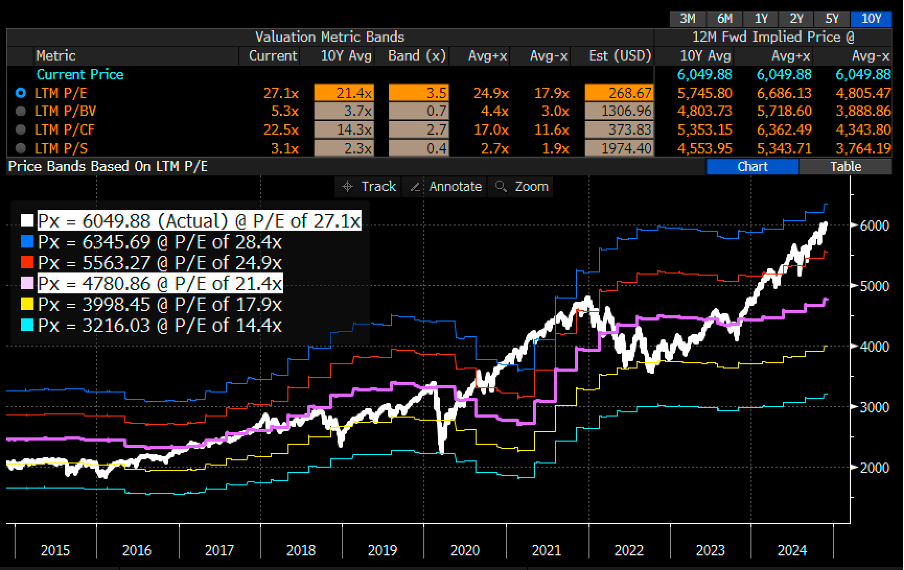

As highlighted previously, Trump’s proposed policies, including tax cuts, deregulation, and tariff adjustments, have been key drivers fueling the relentless rally in U.S. equities. However, on the downside, the S&P 500 is now trading at nearly twice its 10Y historical average P/E range, signaling that valuations are significantly stretched and the market appears expensive.

#3

In-line with the positive outlook for the U.S. market, Airo-BOCA portfolios increased allocation to U.S. equities during the November rebalancing.

#4

We believe the ongoing U.S. interest rate cut cycle should continue to provide a favourable tailwind for the U.S. equity market. However, given the elevated valuations mentioned earlier, we decided to maintain a diversified exposure, including exposure to emerging markets, which experienced significant corrections in the past month.

#5

Looking ahead, the direction of the global equity market will largely depend on the implementation of Trump’s policies, the continuation of global interest rate cut cycles, and stimulus measures from emerging markets, particularly China.

– – –

Dear Valued Investors,

U.S. equities posted their strongest performance in November 2024, fueled by sustained optimism surrounding Trump’s election victory. For the month, the S&P 500 and MSCI ACWI indices surged by +5.73% and +4.03%, respectively, reflecting broad market confidence. Airo-BOCA, by comparison, was dragged down by copper and emerging markets’ exposure and returned negatively at -0.84%.

Table 1: Airo-BOCA Composite Return (Nov 2024)

As highlighted previously, Trump’s proposed policies, including tax cuts, deregulation, and tariff adjustments, have been key drivers fueling the relentless rally in U.S. equities. However, on the downside, the S&P 500 is now trading at nearly twice its 10-year historical average P/E range, signaling that valuations are significantly stretched and the market appears expensive. We are mindful that the U.S. market may have front-loaded the bulk of the equity performance at the current juncture despite the view that we are positive on the U.S. market.

Chart 1: S&P500 is trading at 1.9x above its 10Y historical average PE band, i.e. expensive.

In-lined with the positive view on the U.S. market, Airo-BOCA portfolios increased their allocation to U.S. equities during the November rebalancing. However, we are cautious against going all in U.S. equity given the pricey valuation as mentioned.

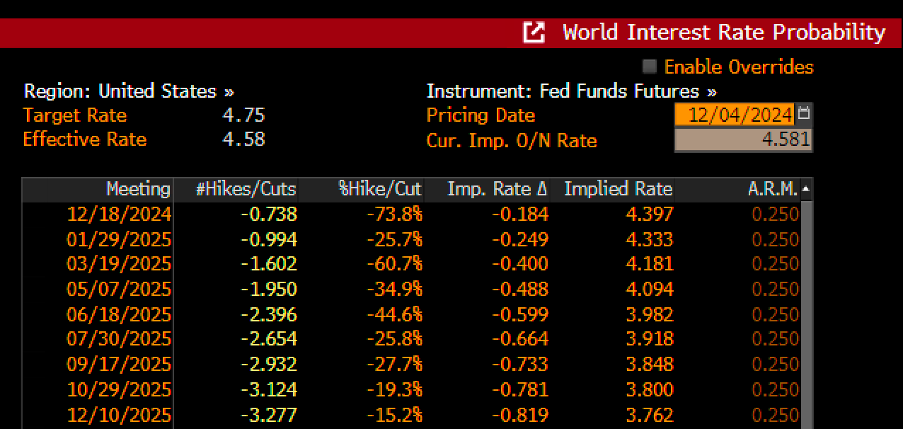

We believe the ongoing U.S. interest rate cut cycle should continue to provide a favourable tailwind for the U.S. equity market. At current juncture, the U.S. interest rate futures’ market is pricing in 2 to 3 more interest rate cuts until the end of 2025. The pace of interest rate cuts’ expectation may have slowed, nevertheless, this should continue to be supportive of the U.S. equity market.

Table 2: U.S interest rate futures’ market is pricing in between 2 to 3 cuts until the end of 2025.

As mentioned, given the pricey valuation as mentioned, we decided to maintain a diversified exposure into the emerging markets that had corrected sizably in the past month. From a valuation perspective, the MSCI Emerging Market is trading at 0.2x below its 10-year historical average P/E band, i.e. it is not expensive.

Chart 2: MSCI Emerging Market is trading at 0.2x below its 10Y historical average PE band

Looking ahead, the direction of the global equity market will largely depend on the implementation of Trump’s policies, the continuation of global interest rate cut cycles, and stimulus measures from emerging markets, particularly China. Specifically, China’s leaders are set to start their annual Central Economic Work Conference next week to set the pace of GDP growth target as well as any further stimulus consideration next week. This anticipated event could provide further insights into the mind of Chinese leaders.

December 6th, 2024

William Yii

CIO, CP Global Fintech Solutions.

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.