CIO Letter – Feb 2024: Equity Exuberance Driven by Tech Continues 🤖

Highlights:

#1

January 2024 was marked by another exuberance in the U.S technology stocks that drove S&P500 Index +1.59% up. MSCI ACWI Index was flat at +0.28%. In contrast, China equity market suffered new lost as SHSZ300 A-Share index saw a substantial decline of -7.17%.

#2

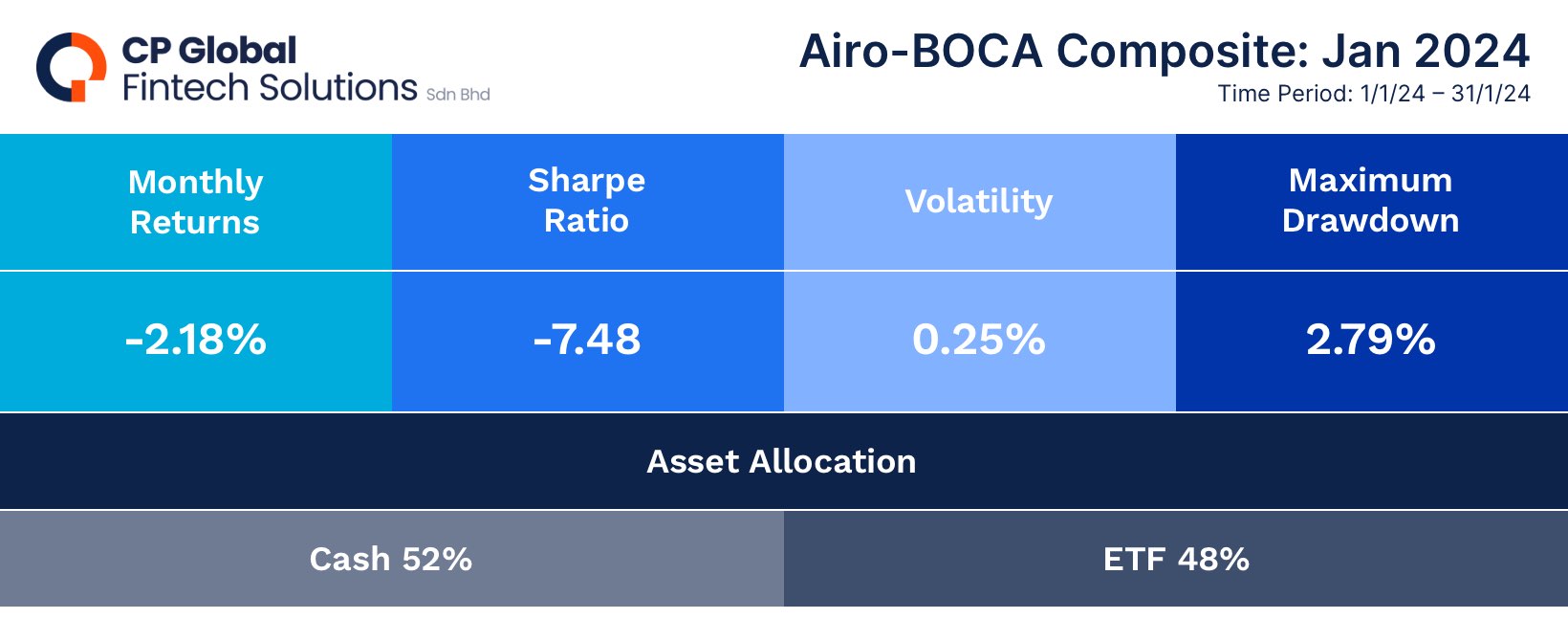

The Airo-BOCA composite saw a decline of -2.18%, largely due to its exposure to China-related commodities in rare earth as well as gold and silver-related sectors. Additionally, hedging positions in the technology sector contributed to the downturn. On the flip side, however, we paced into China as it was deemed an attractive level given the steep correction coupled with various liquidity stimulus measures by the People’s Bank of China (PBOC).

#3

Looking ahead, U.S macro growth continues treading water while Core CPI saw a renewed inflationary pressure in January 2024. The lacklustre macro conditions are being marred by the overall good 4QCY2023 earnings reported by the ‘Magnificent 7’ technology companies.

#4

At Airo, as we usher in the Lunar New Year 2024, we maintain our cautiously optimistic stance. We remain committed to steering the BOCA portfolios towards investment assets that are supported by improving macro fundamentals.

– – –

Dear Valued Investors,

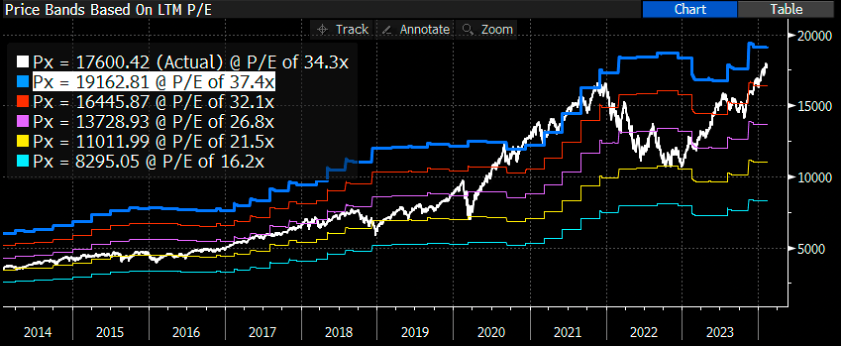

January 2024 was marked by another rally in the U.S technology stocks that drove S&P500 Index +1.59% up. On Artificial Intelligence’s frenzy again, stocks like Super Micro Computer Inc. and NVIDIA Corp. rallied +86% and +24% respectively in January alone. The relentless rallies since November 2023 have duly elevated the valuation exuberance of Nasdaq100 Index to another level.

For context, the Nasdaq100 Index is currently trading and approaching the top-end of its 10-year PE valuation band. The only other time that it traded at the top of its valuation band was during the Covid19’s QE-to-infinity’s period. This means the U.S equity market is very pricey as we speak.

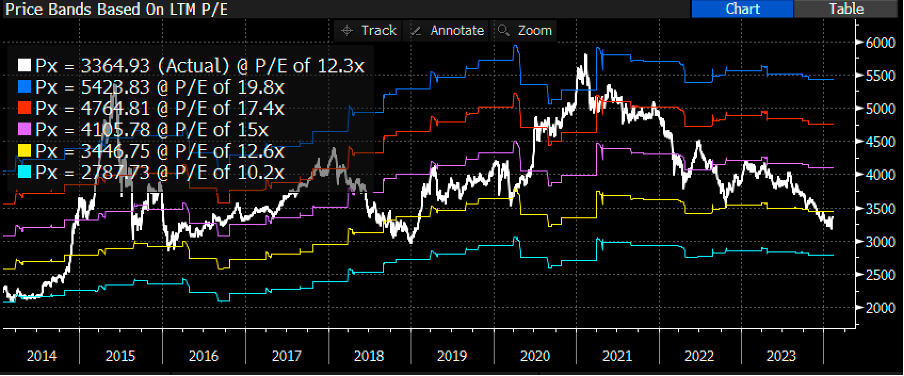

From a broader market perspective, MSCI ACWI Index returned flat for January at +0.28%. And, in contrast to the U.S equity market, China A-share (SHSZ300 Index) suffered a whopping -7.17% lost in January due predominantly to its macro deflationary regime.

Chart 1: Nasdaq100 Index ~ Valuation exuberance continues.

The Airo-BOCA composite experienced a decline of -2.18%, largely due to its exposure to China-related commodities in rare earth as well as gold and silver-related sectors. Additionally, hedging positions in the technology sector contributed to the downturn. With the plummeting China equity market to new lows i.e. approaching its 10-Year trough’s valuation, we see real value emerging.

As the People’s Bank of China (PBOC) recently cut its reserve requirement ratio by 0.50%, this is set to release RMB1 trillion into the banking system. In addition, a RMB2 trillion stabilization fund is planned to be deployed to support the China domestic equity market. Airo-BOCA has thus paced into China equity in the last portfolio rebalancing exercise.

Table 1: AIRO-BOCA Composite Return ~ January 2024

Chart 2: China A-Share SHSZ300 Index ~ Valuation approaching 10-Year’s Low

From a macro perspective, various U.S soft economic data remain in the growth contraction zone for January 2024. These includes the likes of ISM Manufacturing PMI (49.1), Empire Manufacturing Index (-43.7), Dallas Fed. Manufacturing (-27.4), Richmond Fed. Manufacturing (-15) and Philadelphia Fed. Business Outlook (-10.6). While ISM Services PMI (53.4) saw a slight increase in growth expansion, the ISM Prices Paid (64.0) saw a huge concurrent jump. In short, the U.S macro growth continue to tread water while producer price inflation seems to be getting worse.

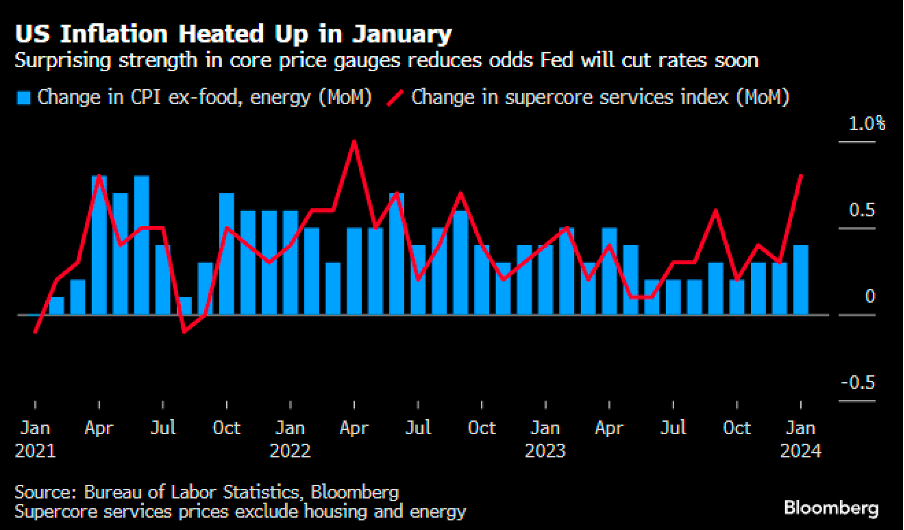

In fact, the U.S Core CPI was unexpectedly sticky and unchanged at +3.9% year-on-year (YoY) in January 2024. This was driven by its month-on-month (MoM) Core CPI of +0.4% in January vs. +0.3% in December 2023. More glaringly, the Supercore Services Index (ex-housing) jumped +0.85% MoM in January from +0.35% MoM in December. As a result, the Supercore Services Index increased +4.29% YoY from +3.91% YoY in December. This goes to show that the road to achieving a +2% YoY Core CPI target could be rather bumpy still.

Chart 3: Supercore Services Index (ex-housing) ~ saw a renewed inflationary pressure in January 2024

The top U.S technology companies reported an overall good 4QCY2023 earnings & management’s forward guidance. Amazon, Alphabet, Meta, and Microsoft are among the best ones with a double-digit revenue growth while Tesla and Apple reported a low single digit revenue growth. These overall good earnings results have marred the uncertain macro-outlook for now.

At Airo, we maintain our cautiously optimistic stance as we usher in the Lunar New Year 2024. We remain committed to steering the BOCA portfolios towards investment assets that are supported by improving macro fundamentals.

Feb 14th, 2024

William Yii

CIO, CP Global Fintech Solutions

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.