Jan 2023: 📈 Airo-BOCA +1.68% vs ACWI -5.34% and SPX -5.90% for the month of December

Highlights:

#1

Airo-BOCA composite closed December with +1.68% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) with -5.34% and -5.90% respectively. Airo’s positive performance for the month was due to the realized profits from our hedging positions. On an annual basis as of December 2022, Airo-BOCA composite returned -1.81%, outperforming ACWI & SPX at -19.74% & -19.44% respectively.

#2

As anticipated, December clocked a huge correction that completely unwound the S&P500’s positive return in November! The negative catalyst was none other than the macro growth trajectory that has turned even more negative on various growth proxies, namely, Dallas Fed. Manufacturing Index, Kansas City Fed. Manufacturing Index, S&P U.S Global Composite PMI and Durable Goods New Orders.

#3

Looking ahead from January onwards, we continue to expect the lack of growth narrative to dominate and drive the interim direction across various asset classes. However, given the softening year-on-year inflationary data since peaking in June 2022, the environment is increasingly constructive for fixed income assets as well as the precious metals sector. In fact, these will be some of the key focuses for Airo portfolios in the coming quarters!

#4

Macro aside, the 4Q2022 corporate earnings reporting will prove to be another important driver for January’s equity return. A vital question to ponder now is how much of the would-be negative earnings has already been duly priced-in given December’s correction? Our sense is that the bias could remain on the downside for now.

#5

Given the persistent negative growth catalysts lurking on the horizon, Airo will maintain tactical hedging allocations while gradually increasing strategic allocations that aims to benefit from the negative growth and disinflationary environment.

– – –

Dear Valued Investors,

Airo-BOCA composite closed December with +1.68% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) with -5.34% and -5.90% respectively. Airo’s positive performance for the month was due to the realized profits from our hedging positions. On an annual basis as of December 2022, Airo-BOCA composite returned -1.81%, outperforming ACWI & SPX at -19.74% & -19.44% respectively.

Table 1: Airo-BOCA YTD Performance – As of December 2022

Source: Interactive Brokers, Airo Malaysia

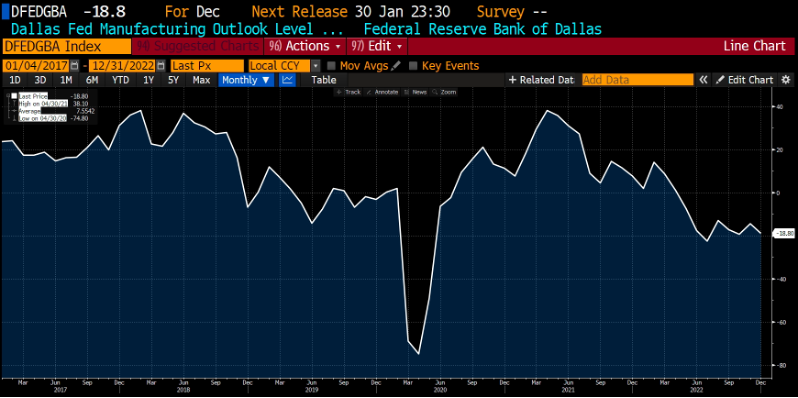

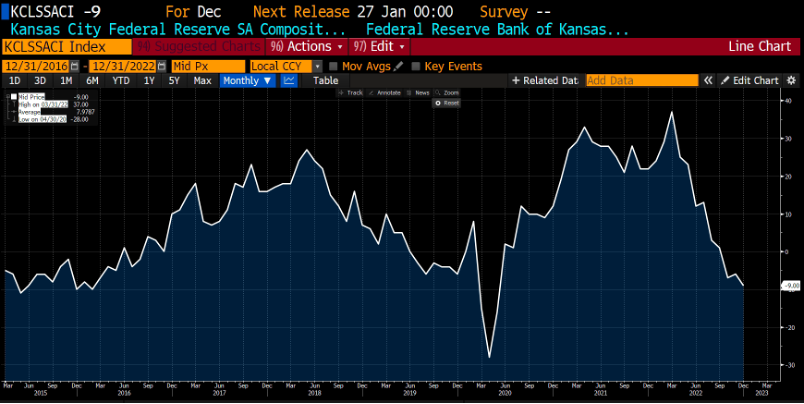

As anticipated, December clocked a huge correction that completely unwound the S&P500’s positive return in November! The negative catalyst was none other than the macro growth trajectory that has turned even more negative on various growth proxies, namely, Dallas Fed. Manufacturing Index, Kansas City Fed. Manufacturing Index, S&P U.S Global Composite PMI and Durable Goods New Orders. On this note, we continue to expect the lack of macro growth to play a dominant role on risky assets’ direction as we start the new year.

Chart 1: Dallas Fed. Manufacturing Outlook ~ Turning more negative at -18.8 vs. -14.4 previously

Source: Bloomberg, Airo Malaysia

Chart 2: Kansas City Fed. Manufacturing Index ~ Plunged to -9 from -6 previously

Source: Bloomberg, Airo Malaysia

Chart 3: S&P U.S Global Composite PMI ~ Contracted to 44.6 from 46.4

Source: Bloomberg, Airo Malaysia

Looking ahead from January onwards, we continue to expect the lack of growth narrative to dominate and drive the interim direction across various asset classes. Indeed, using the U.S. 30Year Treasury Yield as a long-term growth proxy to overlay the above-mentioned macro hard data, it implied that the long-term growth most likely had peaked in the recent months. Given the softening inflationary data since June 2022, the environment is increasingly constructive for fixed income assets as well as the precious metals sector. In fact, these will be some of the key focuses for Airo portfolios in the coming months!

Chart 4: US30Y Yield is implying that long-term growth has peaked!

Source: Bloomberg, Airo Malaysia

At a micro level, the 4Q2022 corporate earnings reporting will prove to be another important driver for January’s equity return. A vital question to ponder now is how much of the would-be negative earnings has already been duly priced-in given December’s correction? Looking at where the S&P500 is now, we expect the bias to remain on the downside over the short-term.

Chart 5: S&P500 ~ Given the potential negative earnings trajectory, the bias is remained to the downside for now

Source: Bloomberg, Airo Malaysia

Finally, given the persistent negative growth catalysts lurking on the horizon, Airo will maintain the tactical hedging allocations while gradually increasing strategic allocations that aims to benefit from the negative growth and disinflationary environment.

Jan 4th, 2023

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.