CIO Letter – Jan 2024: Another Imminent Yen Carry-Trade Unwinding Risk?

Highlights:

#1

December set the stage for the new year with heightened volatility across various asset classes. Global equities experienced a downturn, with the MSCI ACWI and the U.S. S&P 500 indices declining by -3.51% and -2.50%, respectively. This was largely driven by the FOMC’s unexpected hawkish stance on interest rate cuts.

#2

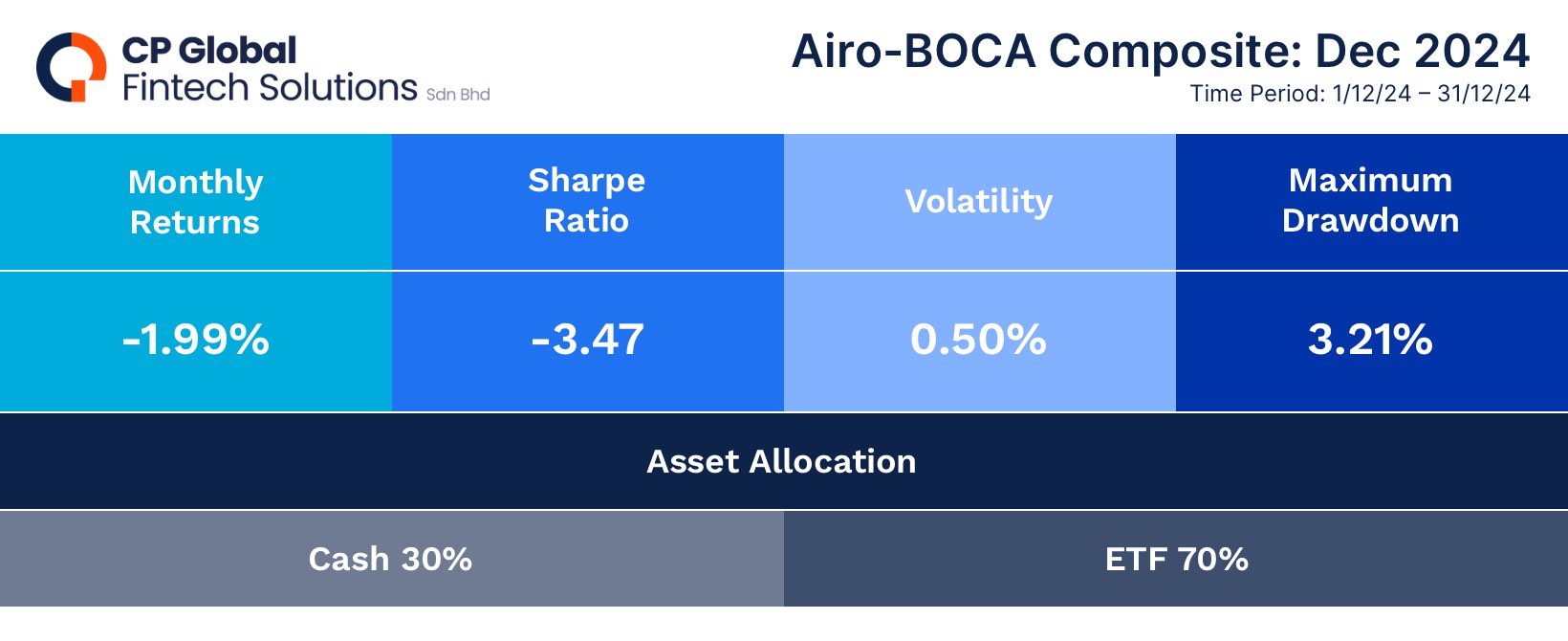

In comparison, the Airo-BOCA composite outperformed both indices, with our portfolios declining by only -1.99%. While China and U.S. technology sectors contributed positively, the overall performance was weighed down primarily by commodities and value sectors.

#3

Looking ahead from a macro perspective, global financial markets face the potential unwinding of Yen carry trades once again. With Japan’s macroeconomic conditions showing sustained improvements in both growth and inflation, the Bank of Japan has compelling reasons to resume its interest rate hike normalization regime.

#4

While an interest rate hike would be bullish for JPY, it could have a bearish impact on Japan equities and other investments that have been leveraging a weak Yen to fund their positions. An increase in Japan’s interest rates would raise borrowing costs, potentially triggering the unwinding of Yen carry trades.

#5

The potential unwinding of Yen carry trades poses a significant risk, and we anticipate increased downside volatility in the coming weeks. In response, Airo-BOCA has recently implemented hedging strategies to mitigate investment exposure.

– – –

Dear Valued Investors,

Global financial markets greeted 2025 with heightened volatility across various asset classes in December. Persistent U.S. inflation pressures led to a bond market selloff, which subsequently triggered intensified declines in the equity market, exacerbated by the U.S. Fed.’s hawkish stance on rate cuts. As a result, the MSCI ACWI global equity index and the U.S. S&P 500 index fell by -3.51% and -2.50%, respectively, in December.

Chart 1: MSCI ACWI ~ peaked in earlier December 2024

In comparison, the Airo-BOCA composite outperformed both indices, with our portfolios declining by only -1.99%. Positive contributions from China and U.S. technology sectors helped mitigate losses; however, the overall performance was weighed down primarily by the commodities and value sectors.

Table 1: Airo-BOCA Composite Return (December 2024)

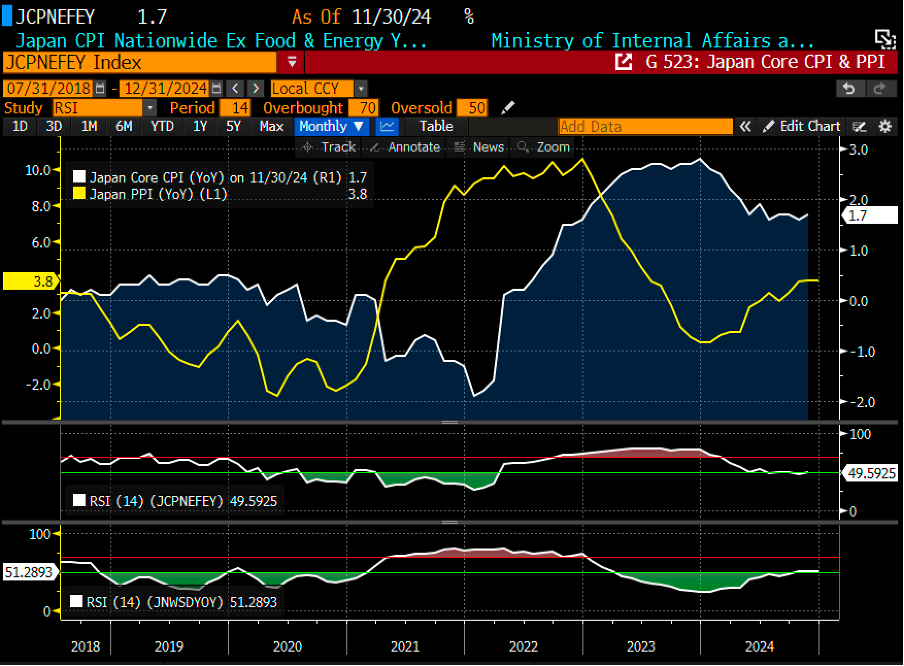

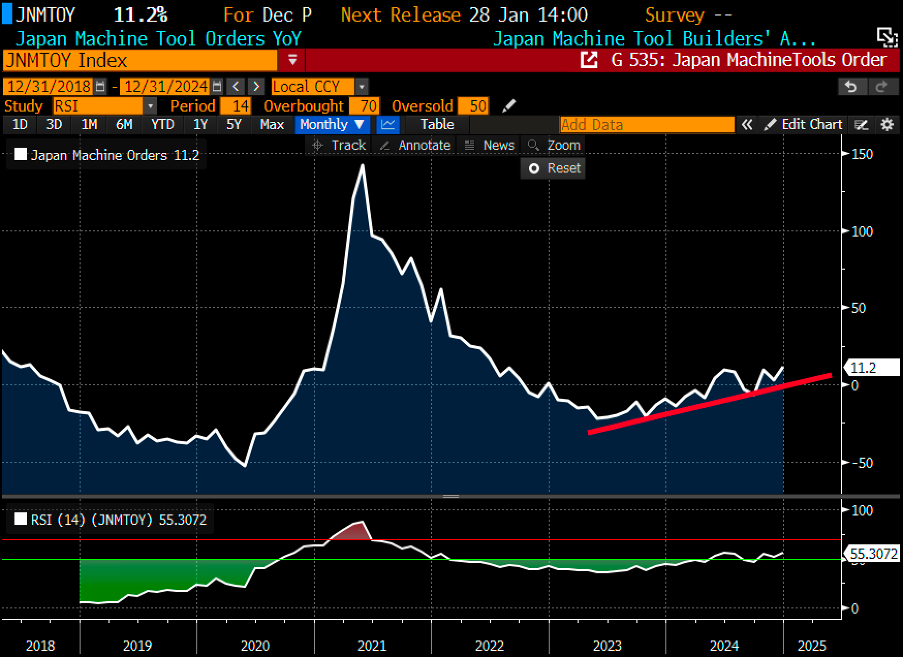

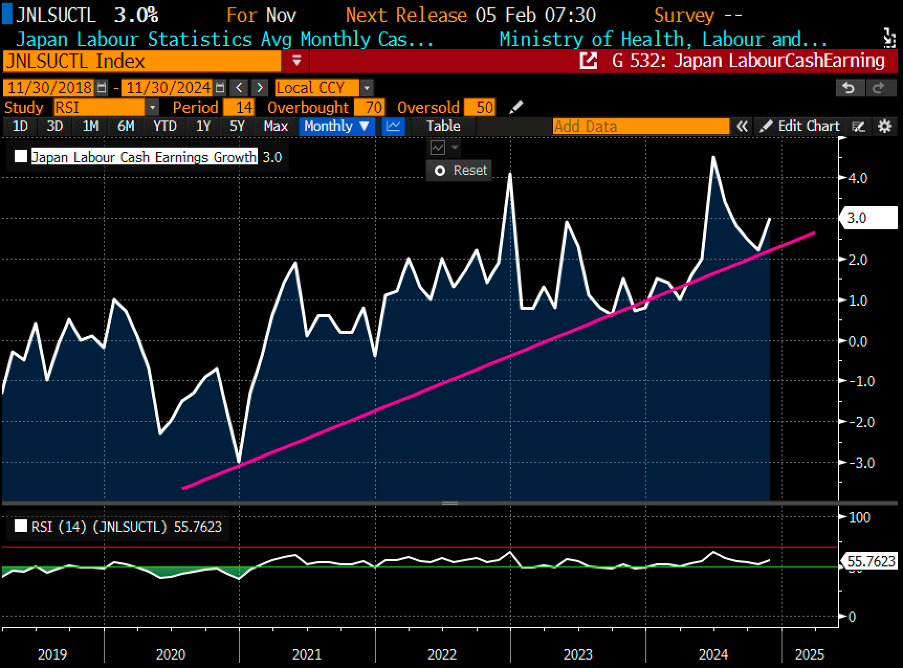

Looking ahead from a macro perspective, global financial markets are once again facing the potential unwinding of Yen carry trades. With Japan’s macroeconomic conditions showing steady improvements in both growth and inflation, the Bank of Japan has compelling reasons to resume its interest rate hike normalization regime sooner rather than later. On the inflation front, Japan’s Producer Price Index (PPI) has been rising consistently throughout 2024, although core Consumer Price Index (CPI) growth remains relatively subdued. On the growth front, a surge in machine tools orders has skyrocketed.

Chart 2: Japan PPI on a strong trajectory relative to its Core CPI

Chart 3: Japan machine tools continues to grow steadily

Chart 4: Japan labour’s cash earnings growth also looking up nicely!

While an interest rate hike would be bullish for JPY, it could have a bearish impact on Japan equities and other investments that have been leveraging a weak Yen to fund their positions. An rise in Japan’s interest rates would increase borrowing costs, potentially triggering another unwinding of Yen carry trades. However, the potential selloff implications extend beyond Japan equities, as Yen carry trades are deeply embedded in global equity and bond markets, especially in the U.S markets.

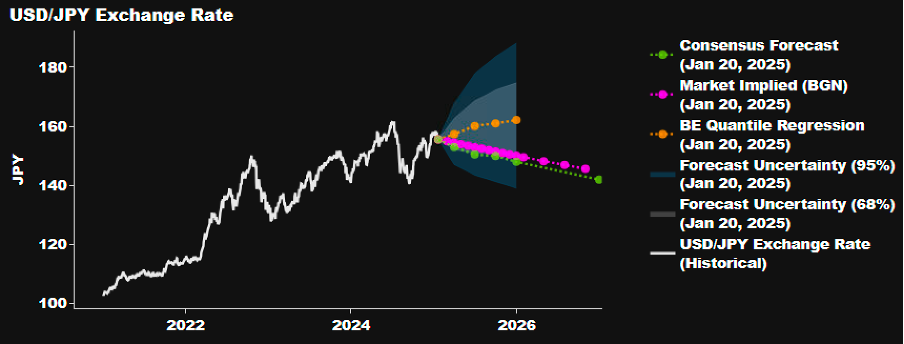

Chart 5: Market consensus is expecting JPY to continue strengthening throughout 2025

Chart 6: Nikkei225 is at risk of another protracted selloff

Given the potential for near-term downside volatility, Airo-BOCA has recently implemented hedging strategies to safeguard its investment exposure and mitigate the impact of any unfavourable market movements.

January 20th, 2025

William Yii

CIO, CP Global Fintech Solutions

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.