CIO Letter – Jul 2025: Bubbling Up Despite Macro Risks

Highlights:

#1

Despite persistent macro risks associated with Trump’s policy uncertainties, global equities continued bubbling up in June, with the S&P 500 and ACWI posting returns of 4.96% and 4.00%, respectively.

#2

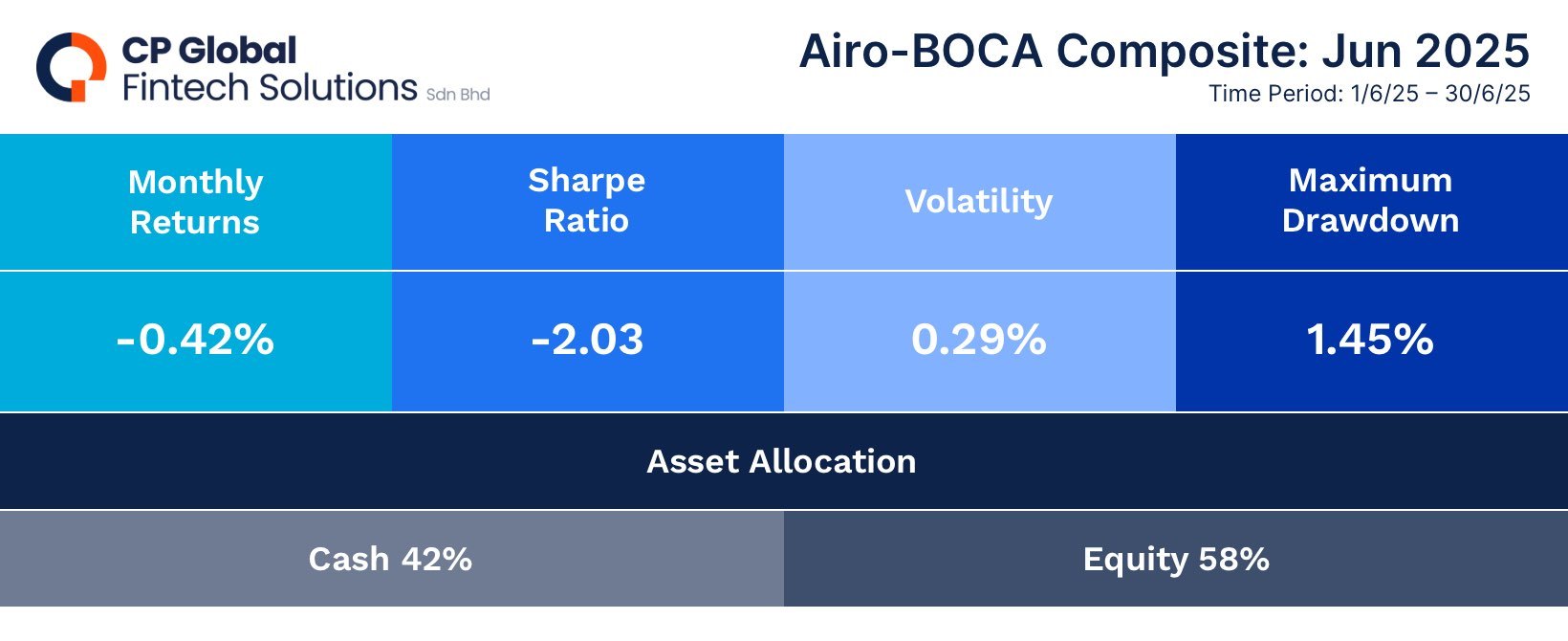

The Airo-BOCA Composite declined by -0.42%, primarily due to an existing hedging position. On the other hand, the Airo-Shariah Composite gained +4.33%, driven by sustained exposure to U.S. equity ETFs and technology stocks.

#3

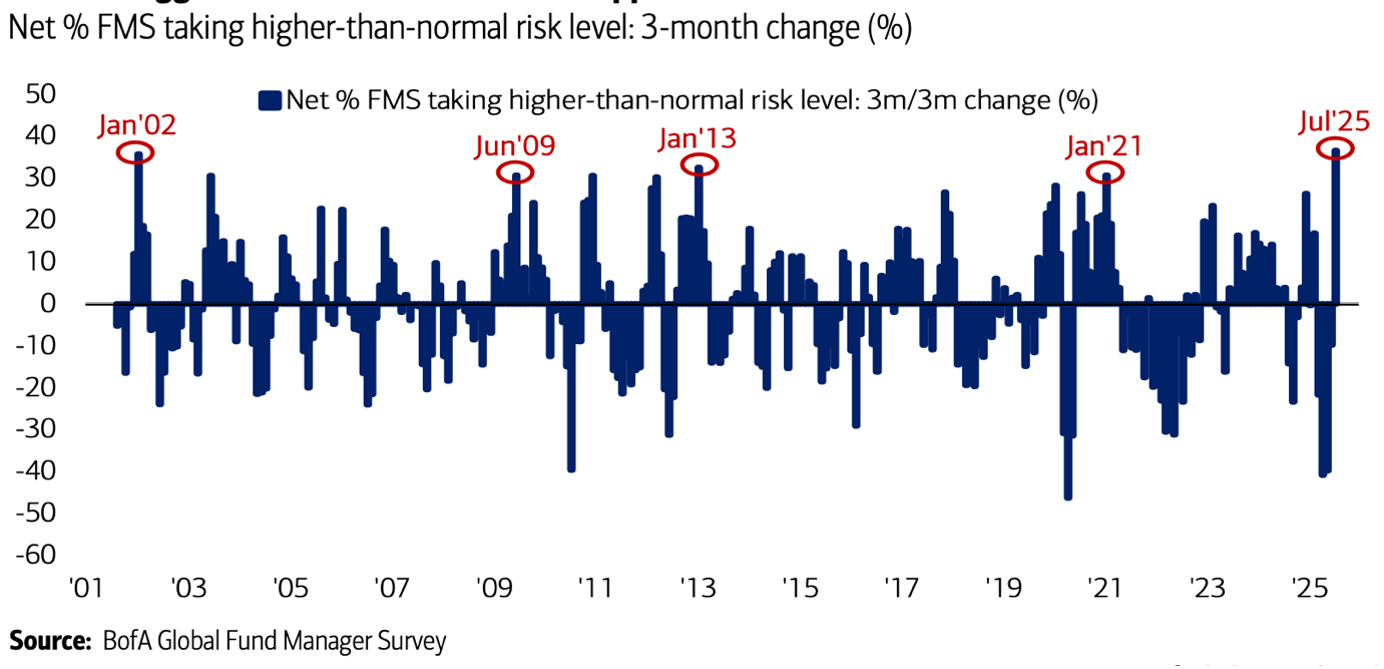

Global fund managers exhibited the highest level of risk-taking since 2002, largely explaining the recent surge in equity chasing.

#4

The Global Dow Index is currently trading near the upper end of its 10-year historical P/E range. Additionally, a broad-base negative divergence in price momentum signals a potential warning.

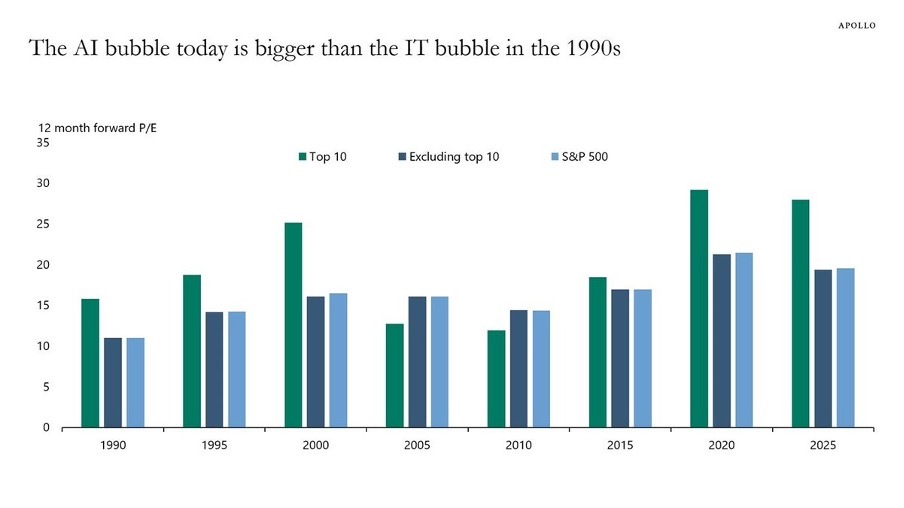

#5

The A.I. bubble, based on 12-month forward P/E ratios, is now trading at its highest levels since the 1990s.

#6

From a macro perspective, the USD remains at a critical juncture, where the long-term de-dollarisation thesis could spell trouble in the quarters ahead.

– – –

Dear Valued Investors,

Despite ongoing macro risks associated with Trump’s policy uncertainties, global equities continued bubbling up in June, with the S&P 500 and ACWI returning 4.96% and 4.00%, respectively. Currently, the S&P 500 is trading at approximately 1.8 standard deviations above its 10-year historical average P/E range.

Chart 1: S&P500 is trading at 1.8x above its historical 10-year average PE band.

The Airo-BOCA Composite declined by -0.42%, once again weighed down by an existing hedging position. On the other hand, the Airo-Shariah Composite gained +4.33%, supported by continued exposure to U.S. equity ETFs and technology stocks.

Table 1: Airo-BOCA Composite Performance (June 2025)

Table 2: Airo-Shariah Composite Performance (June 2025)

Global fund managers have exhibited the highest level of risk-taking since 2002, which largely explains the recent exuberance in equity chasing. Despite persistent tariff-related uncertainties, equity markets have largely shrugged off macro risks, driving global indices higher and seemingly pricing-in a blue-sky scenario for forward growth.

Chart 2: Global fund managers’ risk-taking at the highest level since 2002

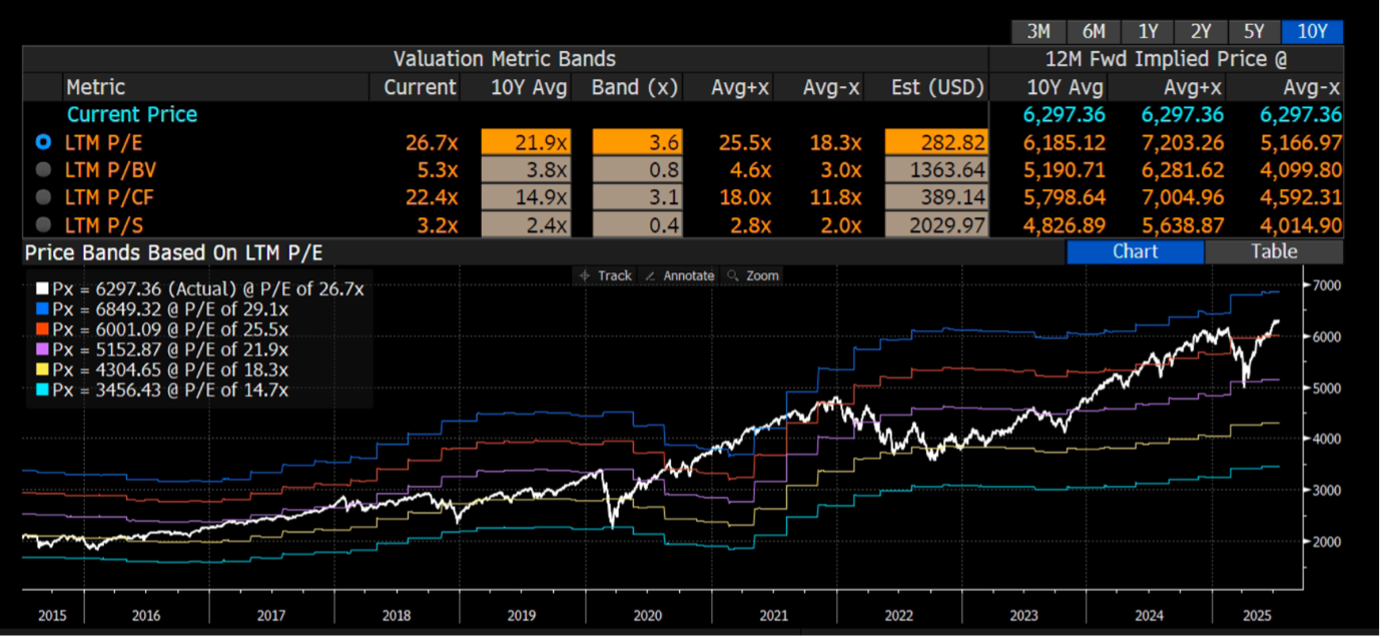

From a global equity valuation standpoint, the Global Dow Index is currently trading near the upper end of its 10-year historical P/E range. This reinforces the view that global equities are advancing in tandem with U.S. equities toward stretched valuation levels.

Chart 3: Global Dow is trading at its upper end of the 10-Year historical PE band

In addition, the Global Dow is exhibiting a broad-base negative divergence–a warning signal from a price momentum perspective. In other words, prices are climbing on weakening momentum, a pattern that often precedes a market correction.

Chart 4: Global Dow’s momentum divergence is sending a warning shot

Zooming into the technology sector, the so-called A.I. bubble is trading at historically high levels based on 12-month forward P/E ratios–the highest since the 1990s. Sustaining such elevated valuations would require equally robust forward earnings growth, which has yet to be seen.

Chart 5: A.I bubble is currently surpassing the level during the dot com’s bubble.

Lastly, the long-term de-dollarisation thesis appears increasingly relevant given the recent trajectory of the USD. While the DXY Index is currently testing its critical uptrend support established since 2010–which thus far remains intact–longer-term structural forces may weigh on the dollar. A shifting global trade rebalancing narrative, coupled with an A.I.-driven deflationary environment, could continue to put downward pressure on the USD. As a result, USD-based assets could be facing an imminent selling pressure in the long-term even if this may not be an apparent risk factor in the current market condition.

Chart 6: USD’s long-term disposition looks bearish despite a near-term rebound

While near-term equity exuberance may persist, Airo continues to maintain a cautious stance at the current juncture.

July 18th, 2025

William Yii

CIO, CP Global Fintech Solutions

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realised by you.