Jun 2022: Remaining nimble in deploying investment capital

Highlights:

#1

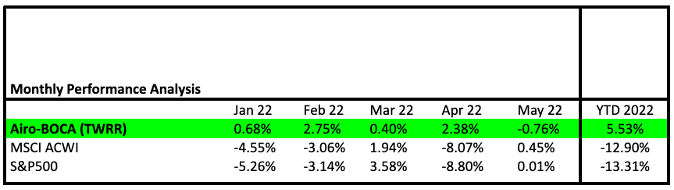

Airo-BOCA composite closed the month of May with -0.76% versus MSCI All Country World Index and S&P500 Index at +0.45% and -0.01% respectively. Towards the end of May, Airo-BOCA re-established tactical hedging positions and this contributed to the negative return as markets staged a relief rebound. However, on a year-to-date basis as of May 2022, Airo-BOCA recorded a positive return of +5.53% versus MSCI All Country World Index and S&P500 Index at -12.90% & -13.31% respectively.

#2

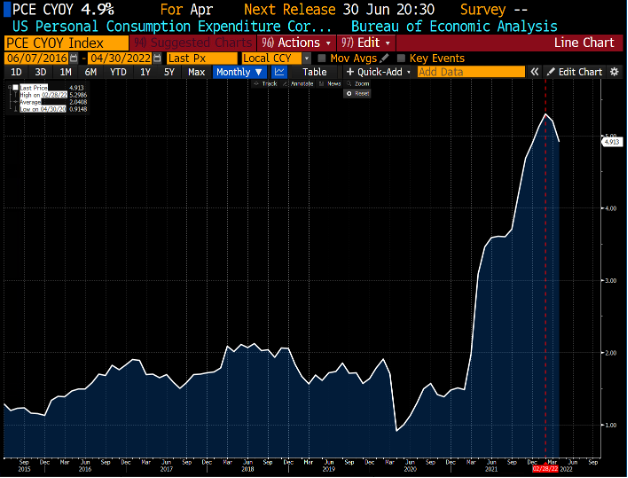

The U.S. macro growth remains a key concern where (i) job growth as proxied by ISM Manufacturing Employment Index has dipped into contraction territory for the first time in May 2022. This means job openings for the manufacturing sector are effectively in a declining trend. In addition, since peaking in February 2022, (ii) Personal Consumption Expenditure (PCE)’s growth has declined steadily over the past months. PCE growth is an important macro’s gauge for the overall consumption growth.

#3

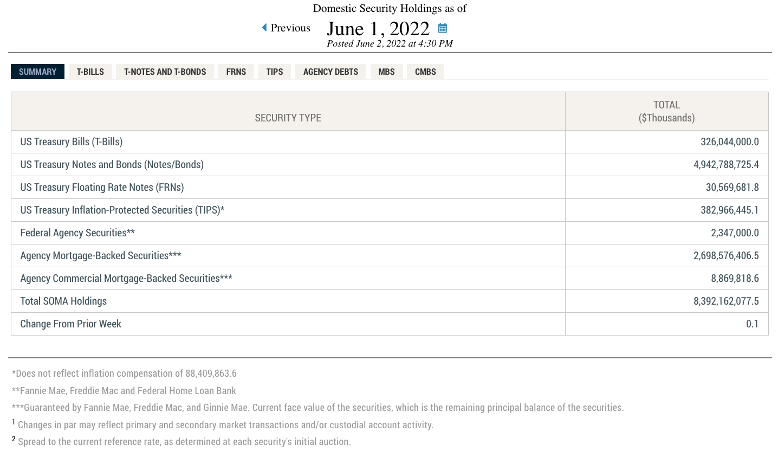

The U.S’ Quantitative Tightening (QT) is starting in June 2022. This means that the U.S Federal Reserve (The Fed.) will let its treasury & related holdings to expire by USD47.5 billion per month in June 2022 to USD95 billion per month from September 2022 onwards in order to reduce its balance sheet. QT, however, has an immediate negative potential to heighten the global equity markets’ volatility as can be seen during the January 2018 – August 2019 QT period.

#4

Given the still uncertain inflationary pressure, macro growth concerns & the potential negative side-effect associated with QT, we remain nimble in deploying investment capital cautiously. High levels of cash & tactical hedging will remain as our primary tools in the current investment environment.

Dear Valued Investors,

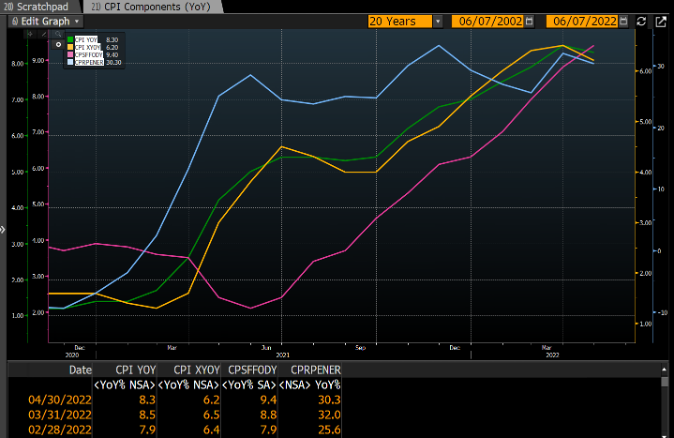

Global markets managed to stage a relief rebound in May largely due to a softening April inflationary data that was released in May. Headline Consumer Price Index (CPI) softened to 8.3% from 8.5% while Core CPI dropped to 6.2% from 6.5%. Albeit the magnitude of the easing in inflationary pressure appeared marginal for now, markets nevertheless took this positively from a possible less hawkish interest rate hikes angle.

Given the relief rebound, MSCI All Country World Index and S&P500 Index returned +0.45% and -0.01% respectively in May but Airo-BOCA composite returned -0.76% as we re-established tactical hedging position towards the end of May.

On year-to-date basis as of May 2022, Airo-BOCA recorded a positive return of +5.53% versus MSCI All Country World Index and S&P500 Index at -12.90% & -13.31% respectively.

Chart 1: Consumer Price Indices Showed Marginal Signs of Easing In April 2022

Source: Bloomberg, Airo Malaysia

Table 1: Airo-BOCA YTD Performance

Source: InteractiveBrokers, Bloomberg, Airo Malaysia

The U.S. macro growth remains a key concern where job growth as proxied by ISM Manufacturing Employment Index has dipped into contraction territory for the first time in May 2022. This index dropped from 56.3 in March to 50.9 in April before going into contraction mode at 49.6 in May. This means job openings are effectively in a declining trend. In addition, since peaking in February 2022, Personal Consumption Expenditure (PCE)’s growth has declined steadily over the past months from the peak of 5.3% in February to 4.9% in April. PCE growth is an important macro’s gauge for the overall consumption growth.

Chart 2: ISM Manufacturing Employment Index – Dipped Into Contraction Mode i.e. below 50 in May 2022

Source: Bloomberg, Airo Malaysia

Chart 3: Personal Consumption Expenditure Growth – Dropping Steadily Since Peaking In February 2022

Source: Bloomberg, Airo Malaysia

In an attempt to further combat the inflationary pressure, U.S Federal Reserve has committed its Quantitative Tightening (QT) measure starting in June 2022. This means that The Fed. will let its treasury & related holdings to expire by USD47.5 billion per month from June to August 2022 without a rollover; with the pace increased to USD95 billion per month from September 2022 onwards to reduce its balance sheet that is currently sitting at USD8.3 trillion. The reduction in The Fed.’s balance sheet will effectively translate to a reduction of liquidity available to the U.S & global financial markets. While QT’s impact to inflationary pressure may not be a direct one, however, QT has an immediate negative potential to heighten the global equity markets’ volatility as can be seen during the January 2018 – August 2019 QT period.

Table 2: U.S Federal Reserve Balance Sheet’s Holding of Treasury & Related Securities

Source: Federal Reserve Bank of New York

In conclusion, given the still uncertain inflationary pressure, macro growth concerns & the potential negative side-effect associated with QT, we remain nimble in deploying investment capital cautiously. High levels of cash & tactical hedging will remain as our primary tools in the current investment environment to ensure that Airo can continue to deliver overall good returns for the coming quarters.

Jun 7th, 2022

William Yii

CIO, Airo Malaysia