CIO Letter – Jun 2024: Expected rate cuts’ driven rally continued

Highlights:

#1

Given May’s FOMC meeting that remained overall dovish, global equities rebounded strongly in May as it continued to take cue of lower interest rates in regard to the incoming U.S rate cuts’ expectation by year end.

#2

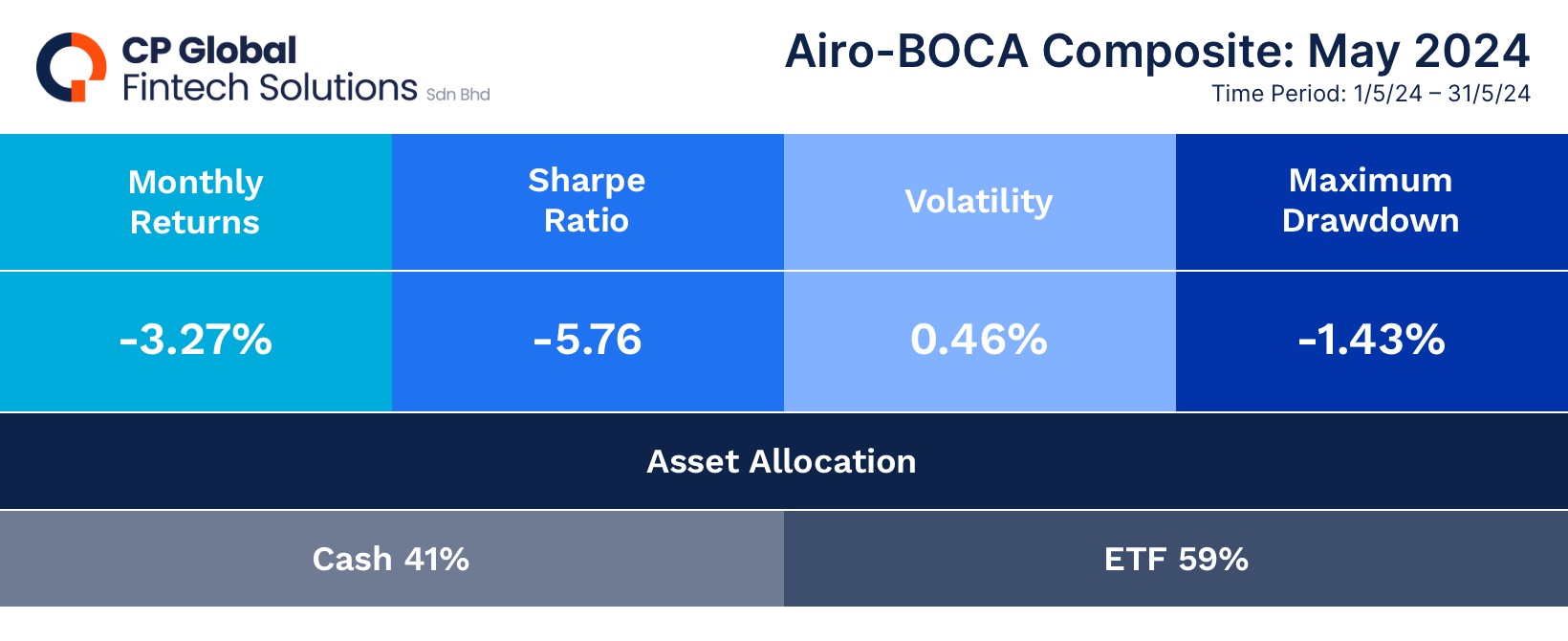

Furthermore, alongside the correction in the gold sector and China equities, Airo-BOCA was negatively impacted by the volatile fluctuations within the cannabis sector. As such, the Airo-BOCA Composite returned -3.27% in May.

#3

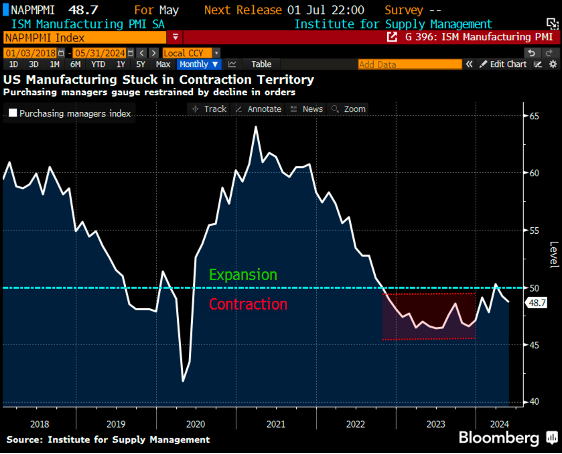

Looking ahead from a macro perspective, the U.S ISM Manufacturing PMI growth contracted for the second consecutive month in May after a brief expansion in March. This trend underscores the patchy nature of macroeconomic growth in the U.S. for now.

#4

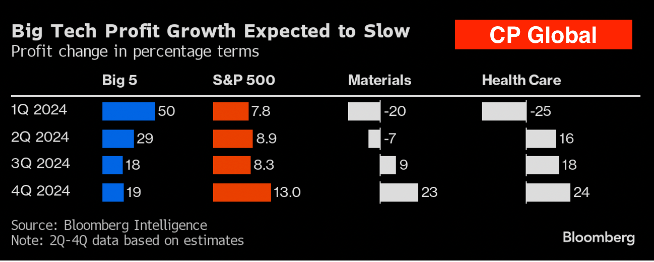

U.S corporations are due to report their 2Q earnings result in July. As it stands, the consensus currently expects the top big five technology stocks to report much lower earnings’ growth at 29% yoy (2Q), 18% yoy (3Q) and 19% yoy (4Q) respectively as compared to their growth of 50% yoy in the 1Q.

#5

Airo remains committed to its active rebalancing strategy and maintaining nimble risk-taking positions to navigate the current market landscape effectively.

– – –

Dear Valued Investors,

As the Federal Reserve Meeting Committee (FOMC) maintained its three rate cuts’ dot-plot during May’s meeting, global equity markets interpreted this as an overall dovish stance despite a continuous sticky inflation. Consequently, MSCI ACWI Index & S&P500 rallied 4.58% and 4.62% respectively in May. Airo-BOCA, on the other hand, was negatively impacted by the volatile fluctuations within its cannabis sector holding. China and the gold sectors also corrected in May and hence adding to the negative return for the month at -3.27%.

Table 1: AIRO-BOCA Composite ~ Performance Matrix (May 2024)

Looking ahead, from a macro perspective, U.S macro growth remained a mixed bag where the ISM Manufacturing PMI saw a second consecutive month of contraction in May (< 50) after just a brief expansion in March (> 50). In contrast, the ISM Services PMI managed to grow (> 50) after a contraction in April. These showed that the U.S macro growth remains patchy for now. To be outright bullish on the U.S economy, we need to see several months of a sustainable growth expansion.

Chart 1: U.S ISM Manufacturing PMI ~ second consecutive month of contraction.

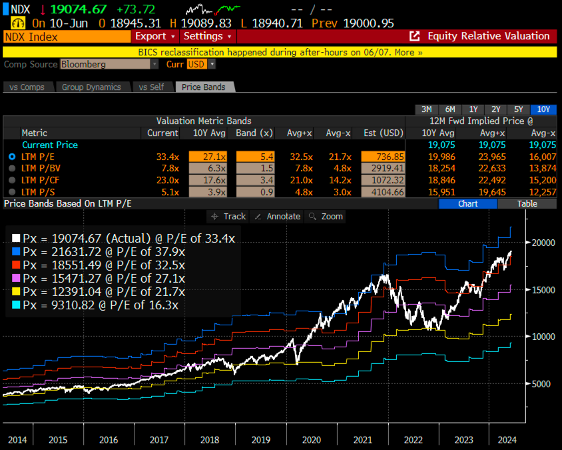

From a micro perspective, the U.S corporations will start to report their second quarter earnings in July. As it stands right now, the consensus is currently expecting the top big five technology stocks to report a much lower earnings’ growth at 29% year-on-year (yoy) for 2Q, 18% yoy for 3Q and 19% yoy for 4Q respectively. Given the new high valuation for Nasdaq100 index, this effectively means that the technology driven market rally could be at risk with a slowing growth expectation going forward. Put this in another way, unless the other sectors could pick up the paces in earnings’ growth, the broader market’s rally is likewise to be at risk.

Chart 2: Nasdaq100’s Valuation at new high.

Chart 3: Consensus’ earnings growth forecast

In short, given the uncertain macro-outlook while the U.S’ corporate earnings growth is expected to slow, Airo remains committed to its active rebalancing strategy and maintaining nimble risk-taking positions to navigate the current market landscape effectively.

June 11th, 2024

William Yii

CIO, CP Global Fintech Solutions

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.