CIO Letter – Jun 2025: More Volatility Anticipated Ahead

Highlights:

#1

U.S equities staged a strong rally in May, with the S&P 500 rising +6.15% and outperforming most of the other markets. In comparison, the MSCI ACWI gained +5.69%, while China’s H-Share Index and A-Share Index returned +3.27% and +2.87% respectively.

#2

Despite the broader market rally, the Airo-BOCA Composite declined by -1.77%, primarily due to an existing hedging position in place. On the other hand, the Airo-Shariah Composite rose by +4.6%, driven mainly by exposure to U.S. equity ETFs and technology stocks.

#3

Following the strong global equity performance in May, markets may be approaching a moment of reckoning amid persistent uncertainty over tariff negotiations, the risk of escalating tensions with Iran, and the ‘big, beautiful fiscal bill’ that is due to be passed in the U.S. Senate.

#4

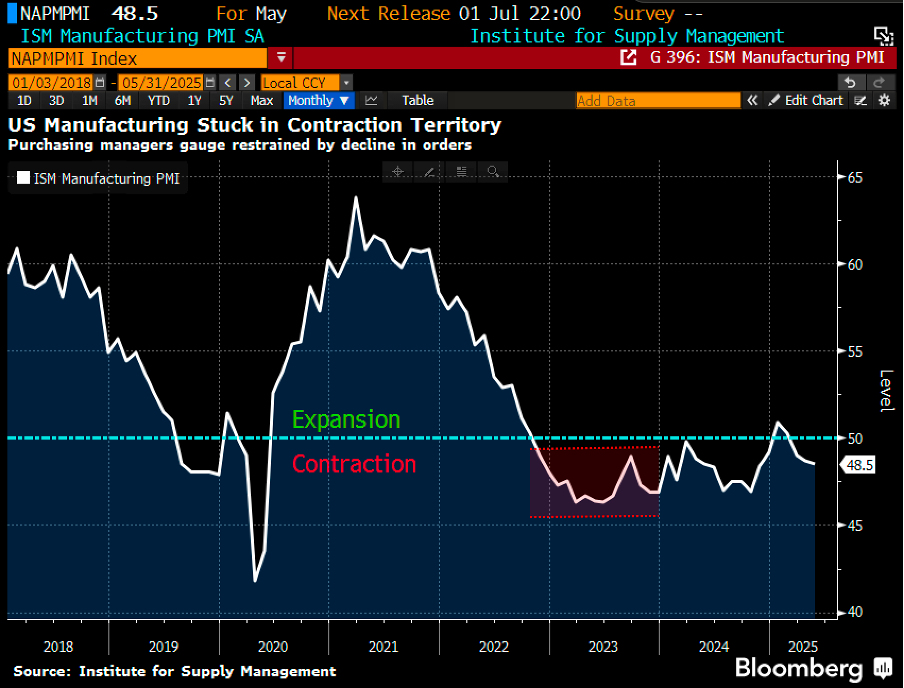

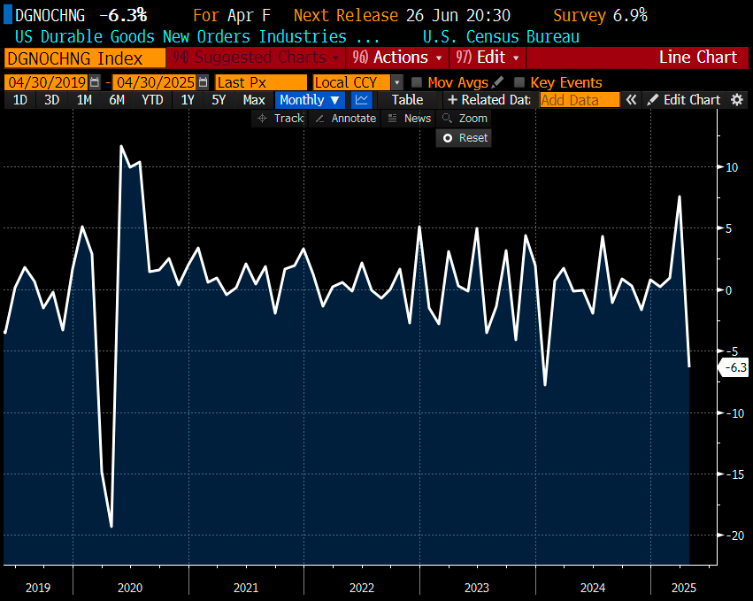

On the macro front, U.S. growth continued to show signs of slowing, with contractions observed across both soft and hard data indicators, including ISM Manufacturing and Services PMI, Durable Goods Orders, Industrial Production, and Retail Sales.

#5

Airo continues to see a disconnect between equity valuations and the array of macro risks that have yet to fully materialise. As such, we will maintain a nimble and adaptive positioning strategy.

– – –

Dear Valued Investors,

Global equities rallied strongly in May, led by U.S. markets, with the S&P 500 gaining +6.15% and outperforming most of the other markets. In comparison, the MSCI ACWI returned +5.69%, while China’s H-Share Index and A-Share Index returned +3.27% and +2.87%, respectively. The rally was largely driven by an interim de-escalation in trade tensions between the U.S. and China, as both sides moved to ease certain export restrictions.

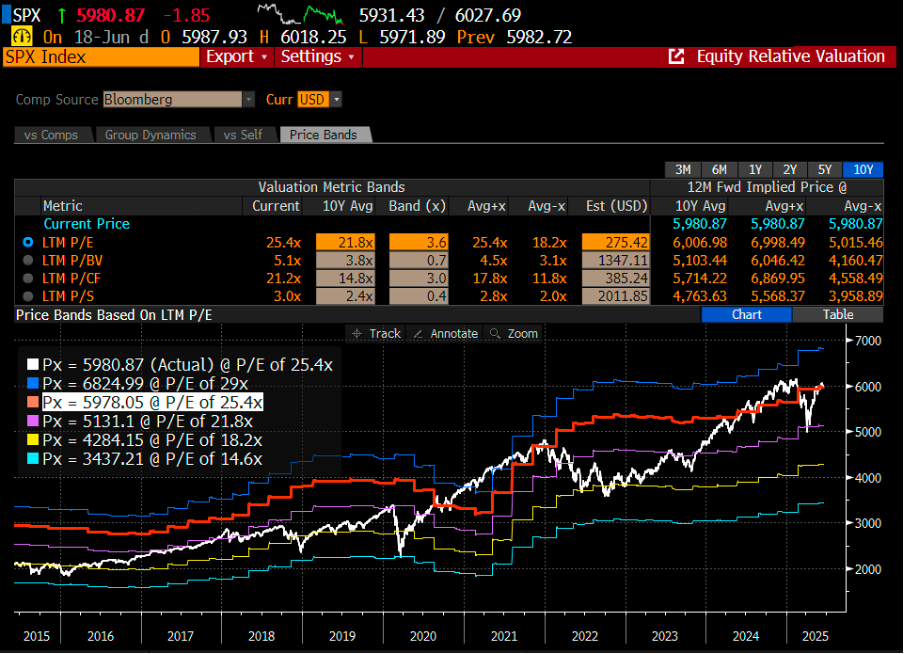

Chart 1: S&P500 is trading at +1x-sigma above its 10Y historical PE bands

Due to an existing hedging position against technology stocks, the Airo-BOCA Composite declined by -1.77% despite the broader market rally. On the other hand, the Airo-Shariah Composite gained +4.6%, largely supported by exposure to U.S. equity ETFs and technology stocks.

Table 1: Airo-BOCA Composite Performance (May 2025)

Table 2: Airo-Shariah Composite Performance (May 2025)

Following the stellar global equity performance in May, markets may be approaching a moment of reckoning amid ongoing uncertainty surrounding: (i) tariff negotiations, (ii) a potential Iran war escalation, and (iii) the ‘big, beautiful fiscal bill’ that is due to be passed in the U.S. Senate.

The interim tariff de-escalation between the U.S. and China was intended to pave the way for further negotiations aimed at reaching an eventual trade agreement between the two nations. Meantime, the global market is also closely watching the U.S. as it seeks to finalise trade deals with other countries before the 90-day tariff pause expires on July 9.

Trump recently signaled that a decision on whether the U.S. will directly engage in the conflict with Iran could be made within the next two weeks. This escalating geopolitical risk looms large and is expected to fuel increased volatility across asset classes in the near term.

The ‘big, beautiful fiscal bill’ is set to be passed by the U.S. Senate by July 4. In our view, U.S. equities have largely priced-in the optimism surrounding its potential approval. As such, any deviation from this expectation could trigger a wave of profit-taking and act as a near-term selling catalyst for the U.S. equity market. Additionally, if the bill is passed, it may unsettle the bond market due to concerns over rising budget deficits in the years ahead.

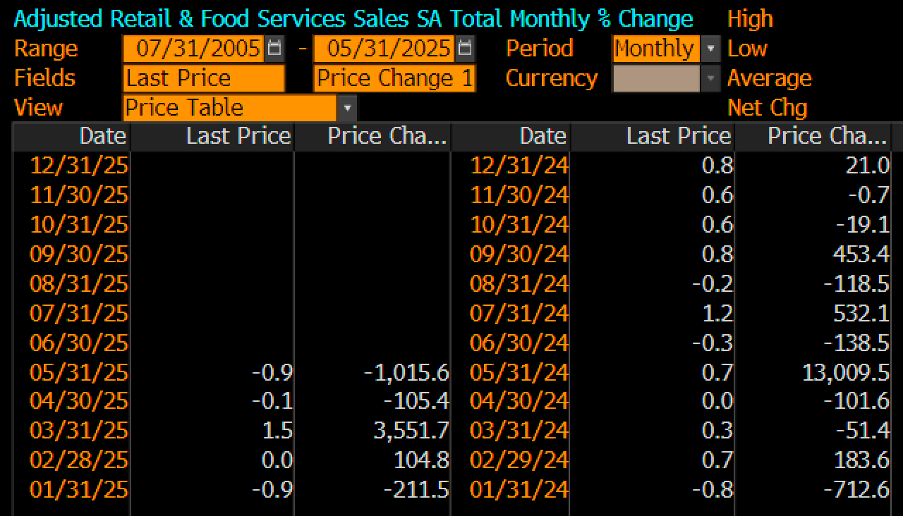

On the macro front, U.S. growth data continue to show signs of slowing, with contractions seen across both soft and hard data indicators. ISM Manufacturing has remained in contractionary territory for three consecutive months since March, while ISM Services PMI slipped into contraction for the first time in May. Durable goods orders plunged -6.3% month-on-month (MoM) in April, partly driven by heightened tariff rhetoric from Trump. Industrial production also cooled, recording just +0.60% year-on-year (YoY) growth. Meanwhile, retail sales declined again in May, falling -0.9% MoM.

Chart 2: ISM Manufacturing PMI contracted for the third consecutive month

Chart 3: ISM Services PMI just slipped into a contraction in May

Chart 4: Durable goods orders saw a big plunge in April at -6.3% MoM

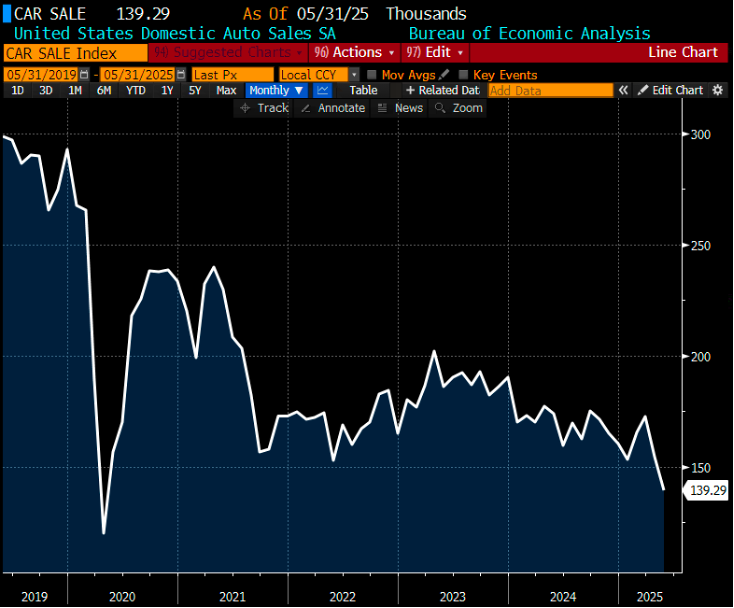

Chart 5: Car sales’ drop is a big contributor in the durable goods orders

Chart 6: Industrial production growth turned cooler at only +0.6% YoY

Chart 7: Retail sales saw a second consecutive month of contraction at -0.9% MoM

Airo continues to see a disconnect between equity valuations and the array of macro risks that have yet to fully materialise. As such, we will maintain a nimble and adaptive positioning strategy.

June 20th, 2025

William Yii

CIO, CP Global Fintech Solutions.

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realised by you.