CIO Letter – Mar 2024: Equity Shined Despite Macro’s Sluggishness

Highlights:

#1

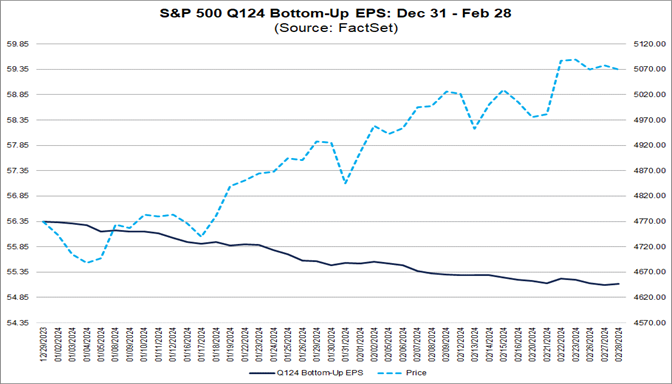

Nvidia’s stellar 4Q’s earnings & guidance prompted a broad market rally with S&P500 & MSCI ACWI closing the month up +5.17% & +4.51% respectively. This was despite the fact that the consensus has been revising down S&P500’s earnings forecast on a year-to-date basis. In other words, the broader market’s rally was driven by something else in addition to technology’s earnings.

#2

The other key driver for the relentless rally is because of a lose financial condition. In fact, the U.S financial condition has been easing alongside the rallies of Nasdaq100 & Bitcoin where Bitcoin is often seen as the higher beta version of Nasdaq100.

#3

The danger of a liquidity and an extreme sentiment driven rally is that the rally itself could be setting up a potential “sentiment crash” event. An example to note is Super Micro Computer Inc’s share price that has gone parabolic while trading at over 50x PE with a ZScore of 4 above its mean.

#4

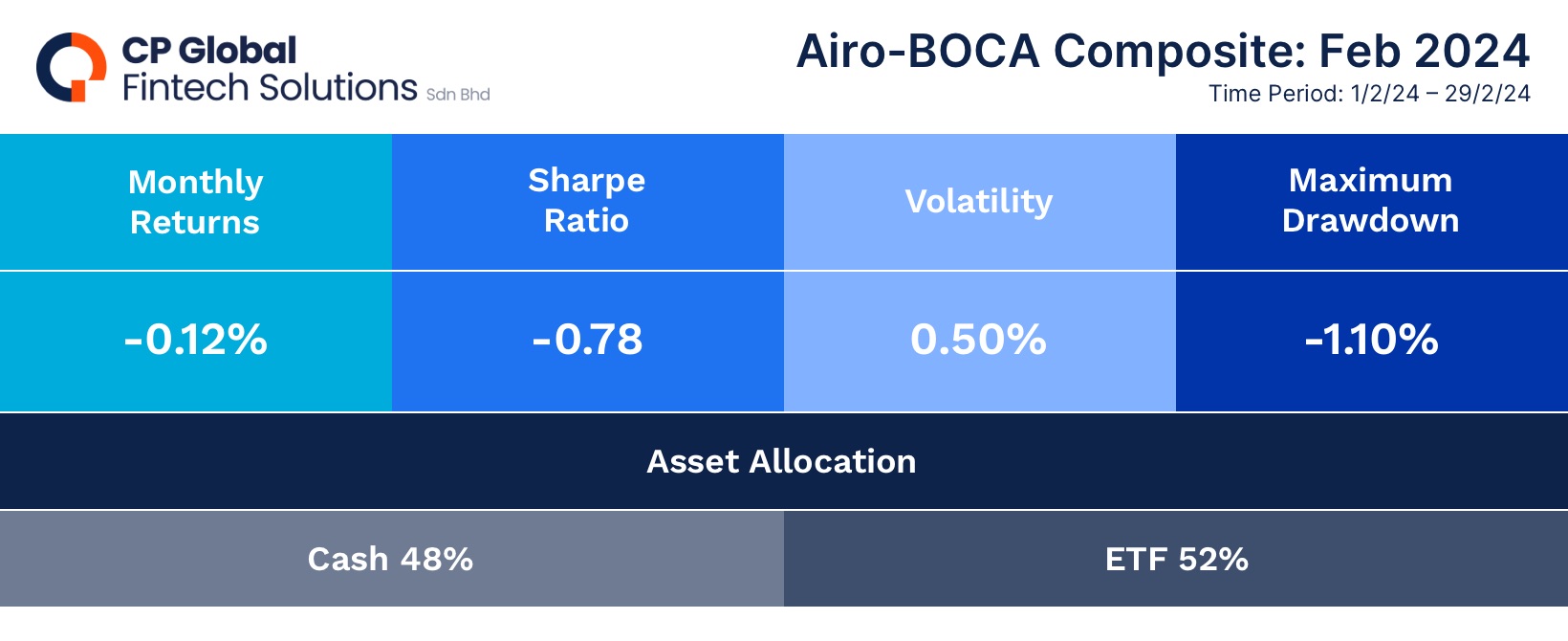

As Airo-BOCA is fundamentally driven, the composite return was flat in February at -0.12% due to the active hedging position. Given the extreme exuberance in the U.S equity prices, the hedging position will be intact for now. On the other hand, both China & gold related positions contributed positively.

#5

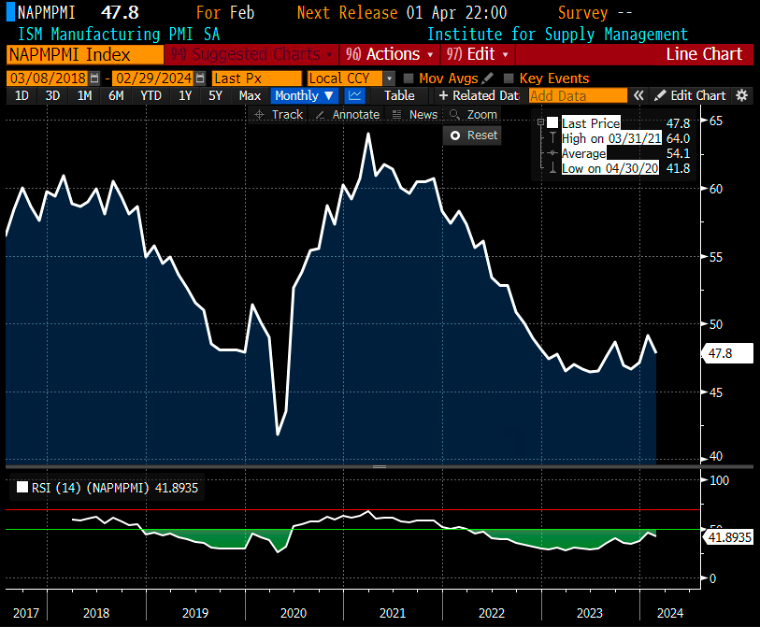

From a macro perspective, macro growth data turned south again, and this shows another disconnection between the equity prices with regards to the overall macro growth condition.

#6

Airo’s strategy remains nimble with regards to cash deployment while maintaining a relatively active rebalancing stance for the coming months.

– – –

Dear Valued Investors,

Nvidia’s stellar 4Q’s earnings & guidance prompted a broad market rally with S&P500 & MSCI ACWI closing the month up +5.17% & +4.51% respectively. This was despite the fact that the consensus has been revising down S&P500’s earnings forecast on a year-to-date basis. In other words, the broader market’s rally was driven by something else in addition to technology’s earnings.

Chart 1: S&P500 ~ Year-to-date EPS downward revision vs. index’s rally

Chart 2: Nvidia ~ Valuation exuberance continues with PE at 77x.

When looking at the U.S equity rally from a liquidity perspective, the relentless rally is also due to a lose financial condition. As a matter of fact, the U.S financial condition has been easing alongside the rallies of Nasdaq100 & Bitcoin where Bitcoin is often seen as the higher beta version of Nasdaq100. In other words, an abundant liquidity lifted all boats regardless of the fundamental reasonings.

Chart 3: U.S Financial Condition ~ tracking in lockstep with Nasdaq100 & Bitcoin prices

The danger of a liquidity and an extreme sentiment driven rally is that the rally itself could be setting up a potential “sentiment crash” event. A sentiment crash happens as and when the market believes that the extreme rally in share price can no longer be supported from its earnings’ fundamental. In addition to Nvidia in the artificial intelligence’s space, another example to note is Super Micro Computer Inc’s share price that has gone parabolic while trading at over 50x PE with a ZScore of 4 above its mean. Eventually, the market will need to come to term with the sustainability of this sort of unhealthy rally.

Chart 4: Super Micro Computer Inc ~ a parabolic rally with 4x standard deviation above the mean

As Airo-BOCA is fundamentally driven, the composite return was flat in February at -0.12% due to the active hedging position. Given the extreme exuberance in the U.S equity prices, the hedging position will be intact for now. On the other hand, both China & rare earth related positions contributed positively.

Table 1: AIRO-BOCA Composite Return ~ February 2024

From a macro perspective, macro growth data continued to worsen. Soft data for February i.e., ISM Manufacturing PMI & MNI Chicago worsened unexpectedly into further growth contraction while hard data, namely, durable goods orders, real personal spending, retail sales and industrial productions all turned negative for January. And, these showed another disconnection between the equity prices with regards to the overall macro growth trajectory.

Chart 5: ISM Manufacturing PMI ~ unexpectedly weakened in February

Airo continues to maintain a nimble strategy with regards to cash deployment while engaging an active rebalancing stance for the coming months.

Mar 8th, 2024

William Yii

CIO, CP Global Fintech Solutions.

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.