CIO Letter – Mar 2025: Tariff Uncertainty Continues

Highlights:

#1

February witnessed a notable correction in U.S. equities, with the S&P 500 declining by 1.42%. The technology sector was once again a major drag on performance, as the Nasdaq 100 fell by 2.76%. Smaller-cap stocks also faced significant pressure, with the Russell 2000 dropping by 5.45%.

#2

In comparison, the Airo-BOCA Composite outperformed the S&P 500, recording a smaller decline of just 0.72%. The relative outperformance was primarily driven by gains in long U.S. Treasuries and long Japanese Yen ETFs. On the other hand, the Airo-Shariah Composite fell by 1.82%, weighed down by its exposure to U.S. technology stocks.

#3

While market pundits remain focused on the uncertainty surrounding Trump’s proposed tariffs, we continue to monitor the broader macroeconomic backdrop–particularly the evolving trajectories of growth and inflation. Although U.S. inflation has continued to ease, it has come at the cost of a weakening macro growth outlook.

#4

On the micro front, Nvidia reported its Q4 2024 results with forward guidance that fell short of consensus’ expectations. More concerning for the broader U.S. technology sector is that the ‘Magnificent 7’ continue to pour billions into AI-related cloud and data centre driven capital expenditures–seemingly with little regard for the potential return on investment.

#5

On the emerging markets front, China appears to have bottomed, as evidenced by its strong recent rally–despite the broader correction in developed equity markets. For context, this upward trend began as early as April 2024, and we expect China to continue its relative outperformance over the medium term.

– – –

Dear Valued Investor,

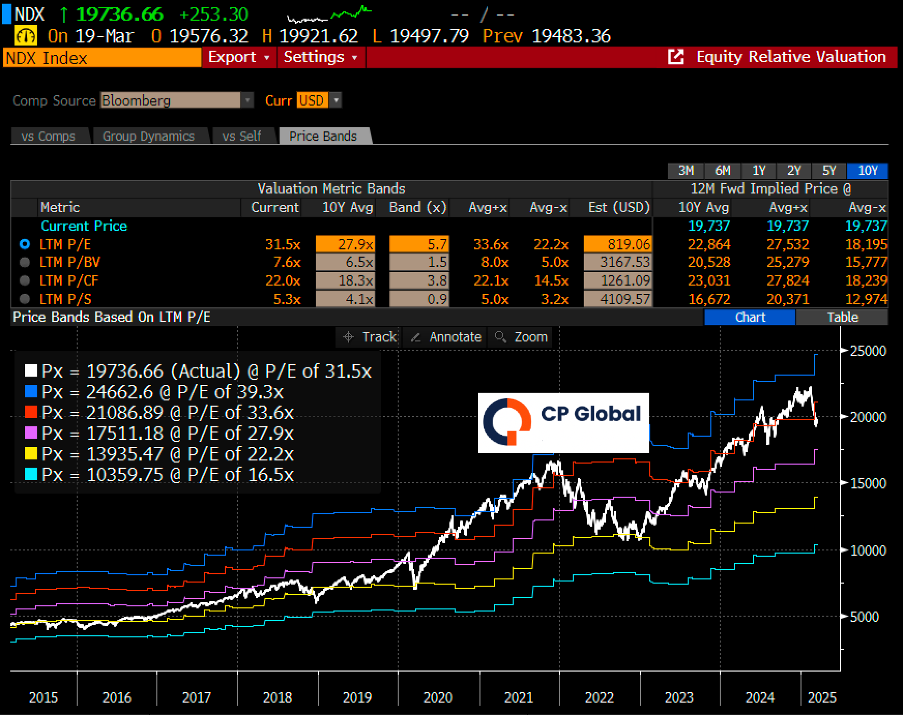

Global equities experienced a notable correction in February, led by the U.S. market. The S&P 500 declined by 1.42% while the Nasdaq 100 and small-cap Russell 2000 fell by 2.76% and 5.45%, respectively. While market pundits were quick to attribute the pullback to tariff-related uncertainty under Trump, the reality is that valuations had become stretched following the strong rally that began in 2023. Even after the recent correction, the Nasdaq 100 remains more than one standard deviation above its 10-year average PE valuation band. A more reasonable near-term fair value would place it closer to its historical average.

Chart 1: Nasdaq100 barely corrected down to its +1-standard deviation band

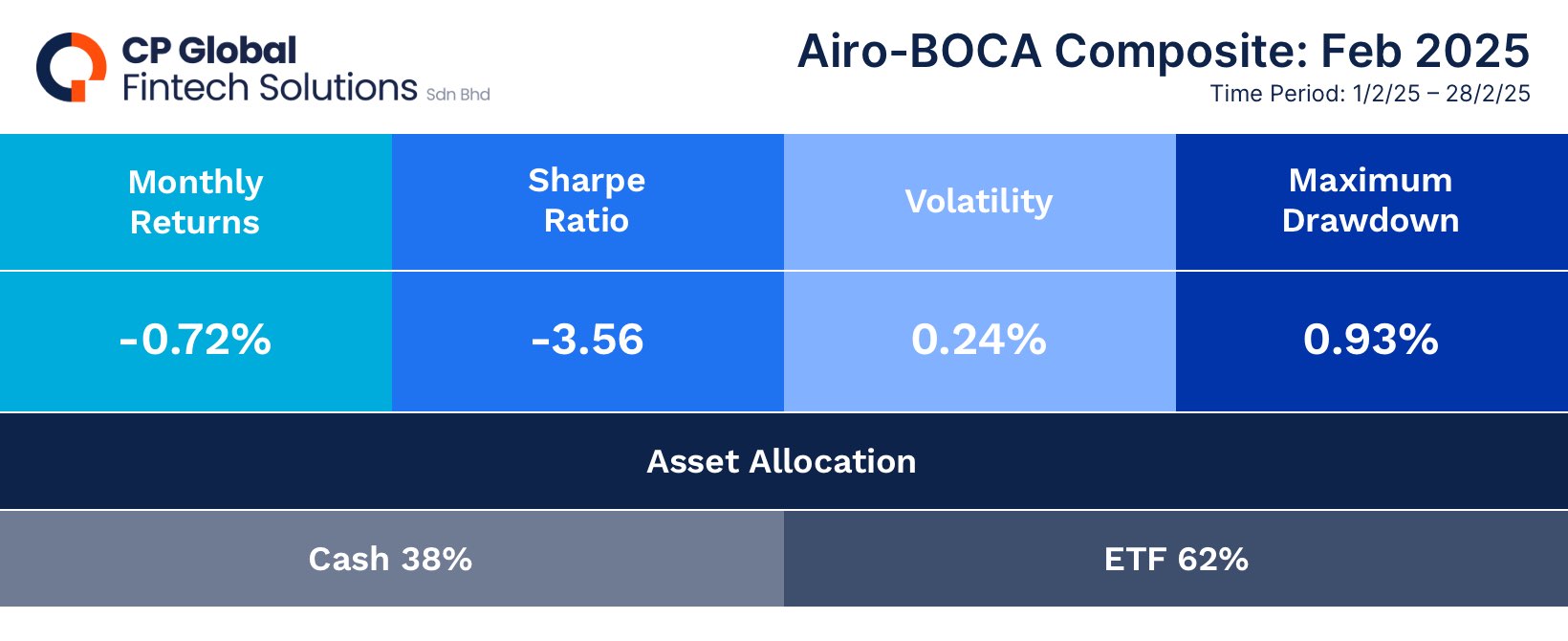

In contrast, the Airo-BOCA Composite outperformed the S&P 500 in February, posting a smaller decline of just 0.72%. This relative resilience was primarily driven by gains in long U.S Treasuries and long Japanese Yen ETFs. Meanwhile, the Airo-Shariah Composite declined by 1.82%, largely due to its exposure to U.S. technology stocks, which weighed on performance.

Table 1: Airo-BOCA & Airo-Shariah Performance As Of February 2025

While market pundits remain fixated on the uncertainty surrounding Trump’s proposed tariffs, we continue to focus on the broader macroeconomic backdrop–particularly the evolving trajectories of growth and inflation. In recent months, U.S. inflation has continued to cool, as reflected in both Headline and Core CPI figures. On its own, moderating inflation is a good thing for the main street, offering some relief to the masses.

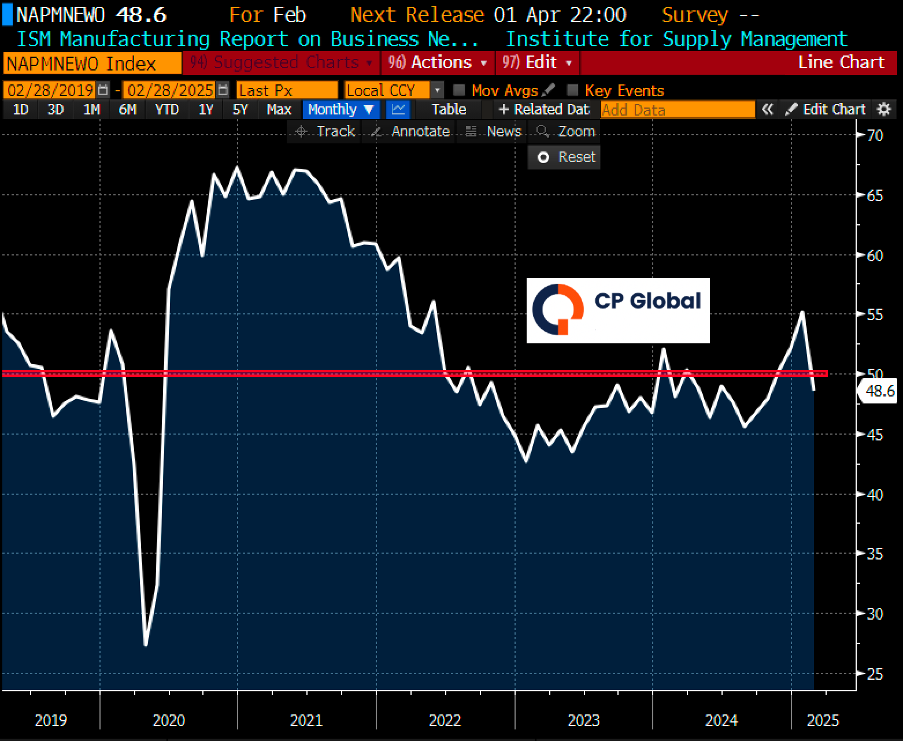

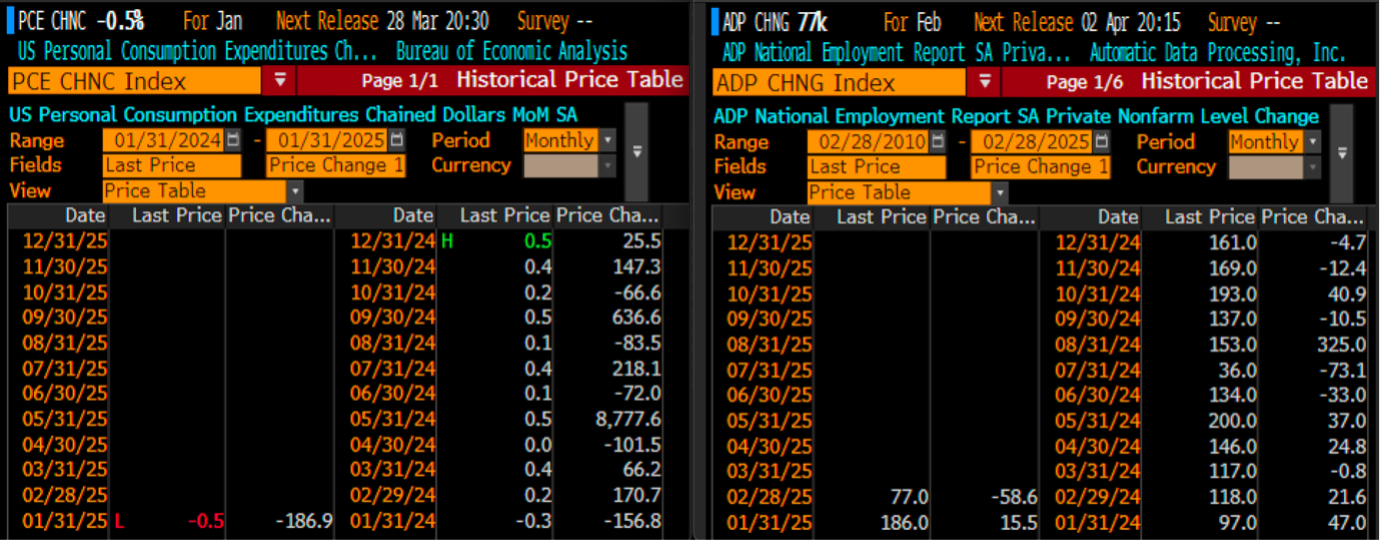

However, there are growing anecdotal signs that the recent cooling in inflation may have come at the expense of weakening economic growth. First, ISM Manufacturing New Orders plunged sharply into contraction territory, indicating negative growth concurrently as manufacturing costs surged. Second, real personal spending unexpectedly contracted for the first time since 2024. Third, private sector job openings–as measured by ADP–declined significantly in February. In short, the softer inflation figures appear to be a byproduct of a deteriorating macro growth trajectory, which is not a reassuring signal for the broader U.S. equity market.

Chart 2: ISM Manufacturing New Orders Plunged Sharply Into Contraction

Table 2: Real Personal Spending vs. Private Payrolls ADP.

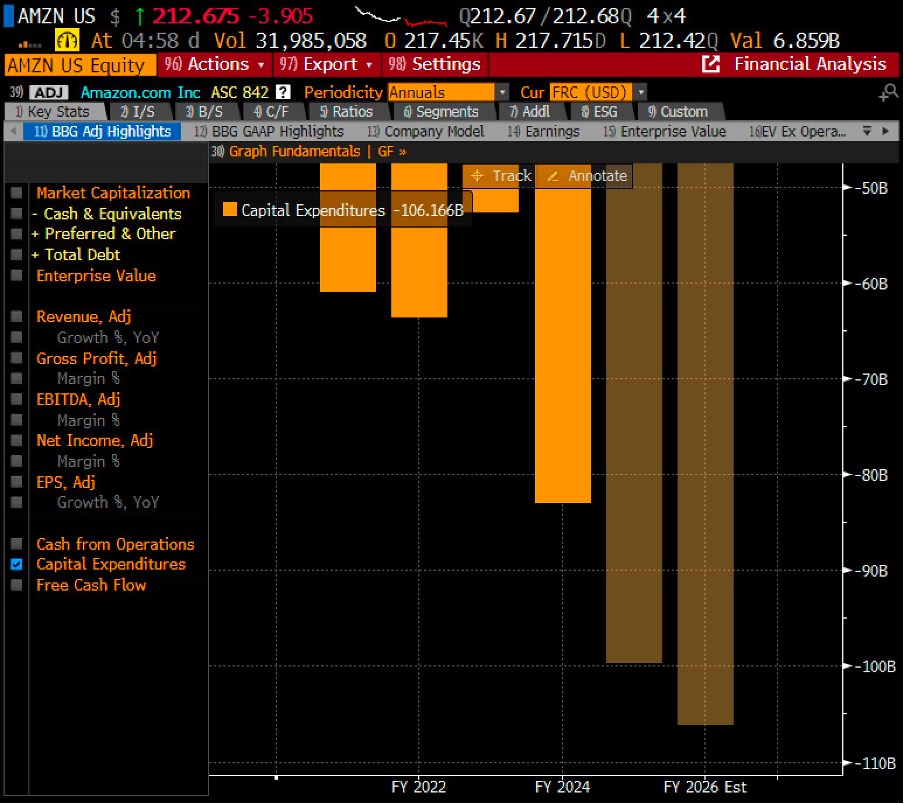

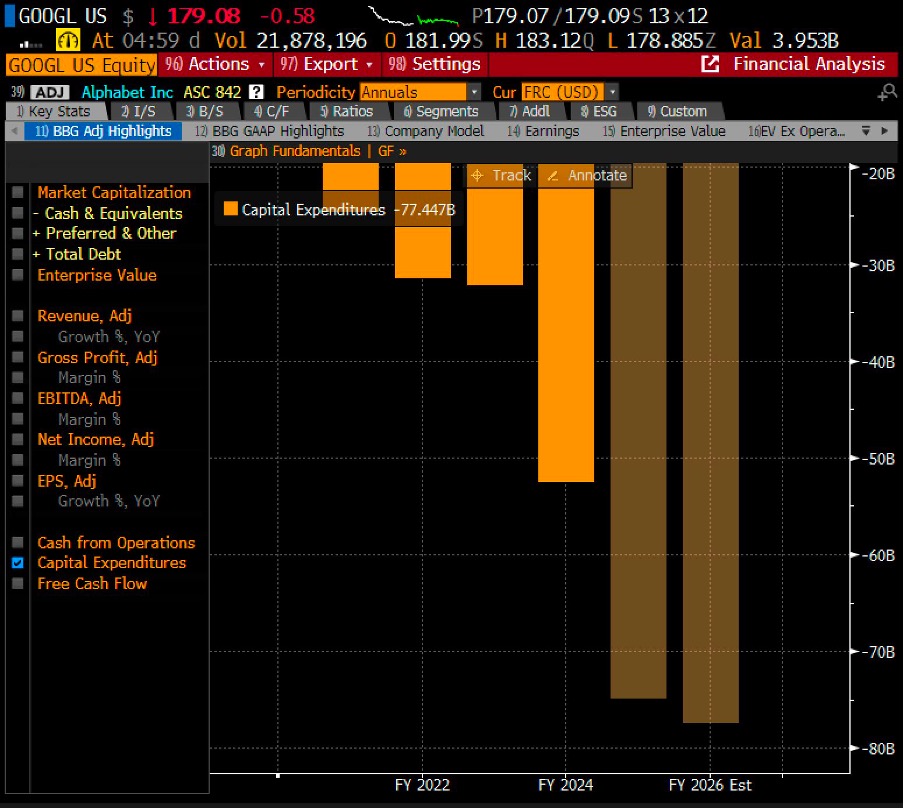

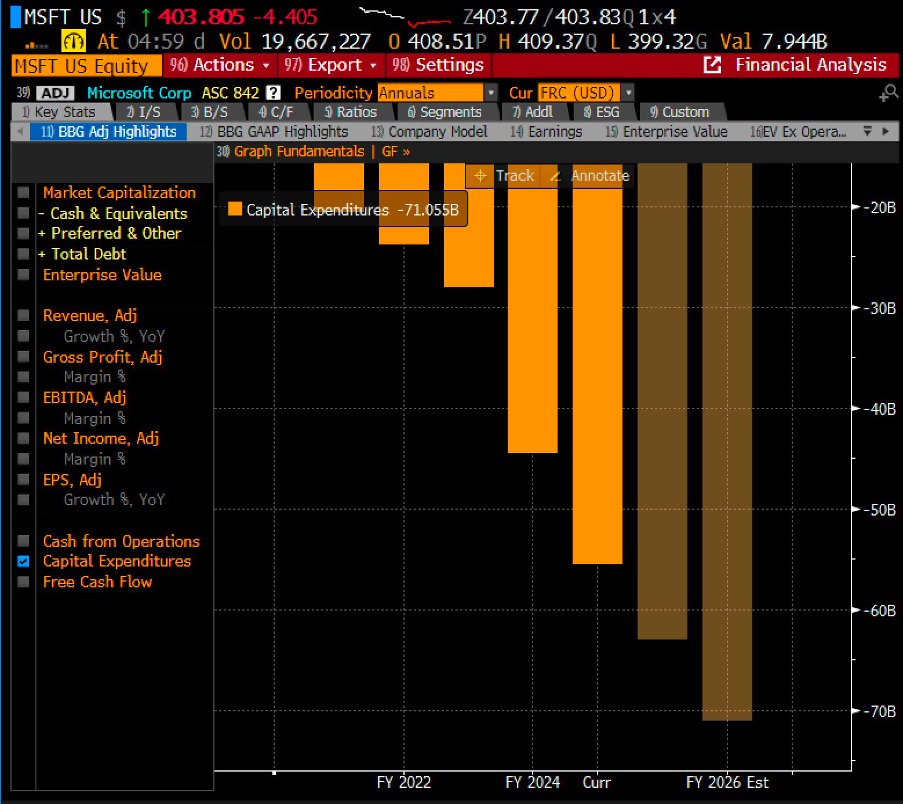

On the micro front, Nvidia reported its Q4 2024 results with forward guidance that fell short of consensus expectations. Specifically, its Q1 2025 revenue guidance came in at the lower end of the range around $43 billion versus the consensus’ estimate of $48 billion at the time. More concerning for the broader U.S. technology sector is the continued aggressive capital expenditure by the ‘Magnificent 7’ on AI-related cloud infrastructure and data centres, seemingly with limited consideration for near-term return on investment.

Chart 3: Amazon’s Capex Intentions

Chart 4: Alphabet’s Capex Intentions

Chart 5: Microsoft’s Capex Intentions

On the emerging markets front, China appears to have found a bottom, as evidenced by its recent strong rally–despite the broader correction in developed equity markets. For context, this upward momentum began as early as April 2024. Looking ahead, we expect China to continue its relative outperformance over the medium term.

Chart 6: China Had Actually Bottomed In April 2024

March 21st, 2025

William Yii

CIO, CP Global Fintech Solutions.

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.