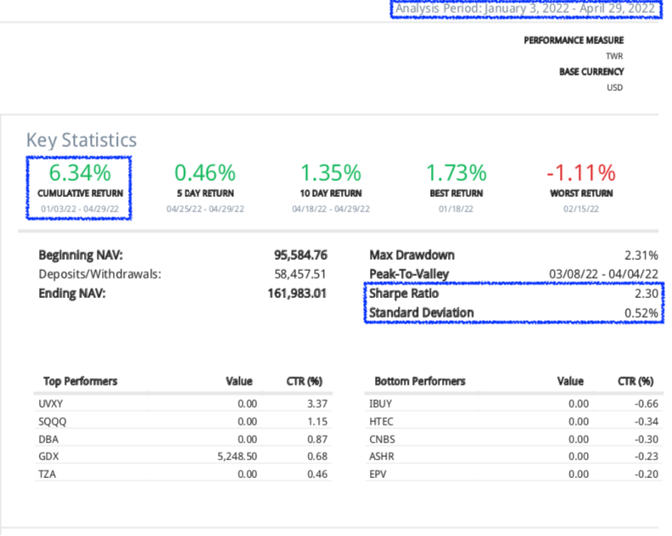

May 2022: Airo-BOCA returned +6.34% YTD (as of Apr 2022)

Highlights:

#1

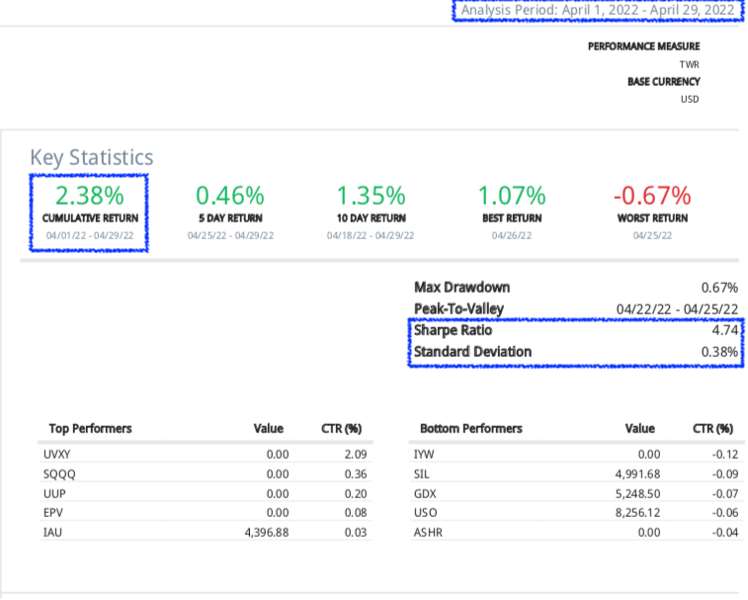

Airo-BOCA composite closed the month of April with +2.38% versus MSCI All Country World Index and S&P500 Index at -8.07% and -8.80% respectively. Again, the positive alpha was mainly attributed to our active hedging positions and the core long position in the USD. On year-to-date basis as of April 2022, Airo-BOCA returned +6.34% versus MSCI All Country World Index and S&P500 Index at -13.28% & -13.30% respectively.

#2

Global inflationary pressure shall continue to be a central theme of risk for the coming months. On one hand, pricing pressures implicate consumers’ purchasing power negatively which could further implicate macro growth. On the other hand, major global central banks have only just started the monetary tightening cycle in a bid to curb inflations. The latter has the unintended consequences of compressing financial market’s valuation from a liquidity perspective.

#3

As highlighted in my previous letters, corporate earnings growth trajectory was the only pillar standing that would have the chance to counter the market correction from a micro perspective. Unfortunately, corporate earnings’ growth has likewise been faltering in the previous months. As a proxy, New York Exchange Composite EPS has contracted -2% while Nasdaq Composite EPS has declined -7% from their peaks in December 2021.

#4

Given that both the macro & micro environment remains unconducive for outright long positionings, Airo shall continue to maintain a strict assets’ risk exposure & risk management regime, an approach that we believe many of our investors could appreciate especially during such volatile times. This means both cash & tactical hedging positionings will remain an important tool while the strategy of initiating core long positionings will be managed in a nimble manner.

Dear Valued Investors,

From a seasonality perspective, April 2022 is officially the worst month of April for the past three decades. The key negative driving forces for the continuous selloff were: (i) macro growth slowing continued (ii) inflationary pressure hit new high (iii) corporate earnings growth profile started to weaken.

Through Airo’s active management strategy, we capitalized on these negatives and turned them into positive returns through our tactical hedging positionings.

For the month of April 2022, Airo-BOCA composite returned +2.38% versus MSCI All Country World Index and S&P500 Index at -8.07% and -8.80% respectively. On year-to-date basis as of April 2022, Airo-BOCA returned +6.34% versus MSCI All Country World Index and S&P500 Index at -13.28% & -13.30% respectively.

What is also worth mentioning is that these returns of Airo-BOCA were achieved with commendable Sharpe ratio & low volatility throughout the period.

Chart 1: ISM Manufacturing PMI – Slowing Growth Expansion Continued in April 2022

Source: Airo Malaysia, Bloomberg

Figure 1: Airo-BOCA April 2022 Monthly Performance Attribution

Source: Airo Malaysia, InteractiveBrokers

Figure 2: Airo-BOCA Year-To-Date as of April 2022 Performance Attribution

Source: Airo Malaysia, InteractiveBrokers

Global inflationary pressure shall continue to be a central theme of risk for the coming months as inflation hit new highs for consecutive months’ since the Covid’s lows in 2020. On one hand, pricing pressures tend to implicate consumers’ purchasing power negatively which could further implicate the global-macro growth cycle that has already peaked.

On the other hand, major global central banks have only just started the monetary tightening cycle in a bid to curb inflations. The latter has the unintended consequences of compressing financial market’s valuation from a liquidity perspective.

In short, quantitative tightening (QT) is the reverse of quantitative easing and this means that liquidity in the financial markets will be significantly reduced for the coming months as the QT is officially starting in June 2022.

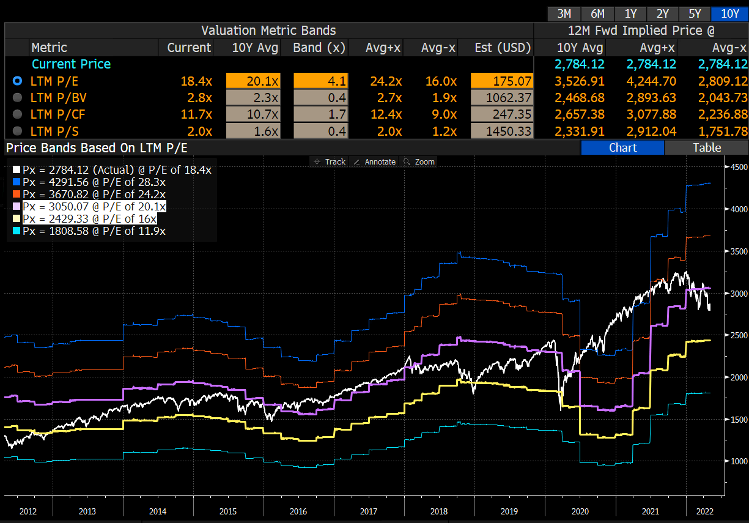

Using MSCI World Equity Index as a proxy for global equity markets, the 10Y PE valuation bands depicted that during the previous severe corrections, such as that in 2018 & 2020, the incoming correction may hit 16x PE versus where it currently stands at 20x PE.

Chart 2: Global Inflation (U.S, Germany, UK, Japan) Hitting New Highs Since Covid’s Low

Source: Airo Malaysia, Bloomberg

Chart 3: MSCI World Equity Index 10-Year PE Valuation Bands

Source: Airo Malaysia, Bloomberg

As highlighted in my previous letters, corporate earnings growth trajectory would have been the last pillar standing that could stand a chance to counter the market correction from a micro perspective. Unfortunately, corporate earnings’ growth has likewise been faltering since the previous months.

As a proxy, New York Exchange Composite EPS has contracted -2% while Nasdaq Composite EPS has declined -7% from their respective peaks in December 2021. What this means is that both macro & micro are churning the growth reversal in addition to global liquidity tightening measures.

Given that both the macro & micro environment remains unconducive for an outright heavy long positionings, Airo shall continue to maintain a strict assets’ risk exposure & risk management regime. This means both cash & tactical hedging positionings will remain an important tool while the strategy of initiating core long positionings will be managed in a nimble manner.

May 6th, 2022

William Yii

CIO, Airo Malaysia