CIO Letter – May 2023: Being nimble in our strategic and tactical asset allocations

– – –

Highlights:

#1

In April 2023, Airo-BOCA composite gained +0.20% while MSCI All Country World Index (ACWI) and S&P500 Index (SPX) were up +1.57% and +1.46% respectively. Despite being range-bound for several weeks, U.S. equities were pushed up towards the end of the month on the better-than-expected headline earnings results from the big technology companies.

#2

On the surface, the 1Q2023 earnings for the big technology companies appeared to be good. Both Microsoft & Amazon reported positive earnings growth. In contrast, however, most companies, namely, Tesla, Netflix, Alphabet, Meta and Intel continued to report negative earnings growth on an absolute basis. From a valuation perspective, all these companies remain expensive, considering their single digit or negative earnings growth.

#3

The U.S regional banking crisis continued to drift even after the First Republic Bank was taken over by J.P. Morgan. PacWest Bancorp & Western Alliance Bancorp were heavily sold-off and down by -45% & -27% in the past few days. Indeed, it remains to be seen if more rescues will be necessary for these and other regional banks going forward.

#4

At the macro level, the U.S government is currently embroiled in another bipartisan standoff over the debt-ceiling. Politics aside, a lack of fiscal discipline and discretionary spending restraint from both parties may prove to be costly for its future generations. For now, the saga could remain just a headline noise.

#5

Post-May’s FOMC meeting, the bond market expects no further rate hikes while pricing-in rate cuts from November’s FOMC meeting onward. No further rate hike would be regarded as a positive factor from an equity valuation perspective. However, earnings’ growth needs to bottom and improve in order to sustain a turnaround in the broader equity market.

#6

Airo’s strategy remains unchanged by being nimble in both strategic & tactical asset allocations. Rest assured that Airo will continue to seek out and capitalize on potential market mispricing opportunities to generate positive alpha steadily for the BOCA portfolios.

– – –

Dear Valued Investors,

In April 2023, Airo-BOCA composite gained +0.20% while MSCI All Country World Index (ACWI) and S&P500 Index (SPX) were up +1.57% and +1.46% respectively. Despite being range-bound for several weeks, U.S. equities were pushed up towards the end of the month on the better-than-expected earnings results from the big technology companies.

Table 1: On a year-to-date basis, Airo-BOCA returned a steady 3.03% (As of April 2023)

Source: Interactive Brokers, Airo Malaysia, Bloomberg.

On the surface, the 1Q2023 earnings for the big technology companies appeared to be good . Both Microsoft & Amazon reported positive earnings growth. Microsoft reported 1Q EPS of +7% yoy while Amazon’s 1Q EPS jumped positively as it was loss-making in 1Q2022. In contrast, however, most companies, namely, Tesla (-21% yoy), Netflix (-18% yoy), Alphabet (-5% yoy), Meta (-19% yoy) and Intel (-105% yoy) continued to report negative EPS growth on an absolute basis. From a valuation perspective, all these companies remain expensive, considering their single digit or negative earnings growth, as reported for 1Q2023’s result.

Chart 1: Nasdaq100 Index ~ is pricey at 29x PE vs. FY23 EPS Growth Estimate of +3%

Source: Airo Malaysia, Bloomberg.

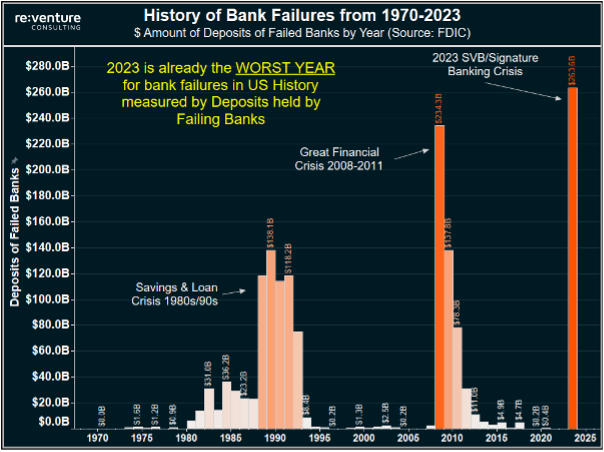

The U.S regional banking crisis continued to drift even after the First Republic Bank was taken over by J.P. Morgan. PacWest Bancorp & Western Alliance Bancorp were heavily sold-off and down by -45% & -27% in the past few days. In aggregate, we are, in fact, dealing with the worst bank failures in the U.S history from a perspective of total deposit size. Indeed, it remains to be seen if more rescues will be necessary for these and other regional banks going forward.

Chart 2: The Worst U.S Bank Failures ~ from the perspective of a total deposit size.

Source: Re:Venture Consulting

At the macro level, the U.S government is currently embroiled in another bipartisan standoff over the debt-ceiling. While the Democrats look for an unconditional lift-off for the debt-ceiling, the Republicans call for a $4 trillion reduction in deficit cuts’ commitment over a decade as a bargaining chip instead. Politics aside, a lack of historical fiscal discipline and discretionary spending restraint from both parties may prove to be costly for its future generations. For now, the saga could remain just a headline noise in terms of its implication to the U.S and global financial markets; but, nonetheless, an imminent tail-end risk to be watched over.

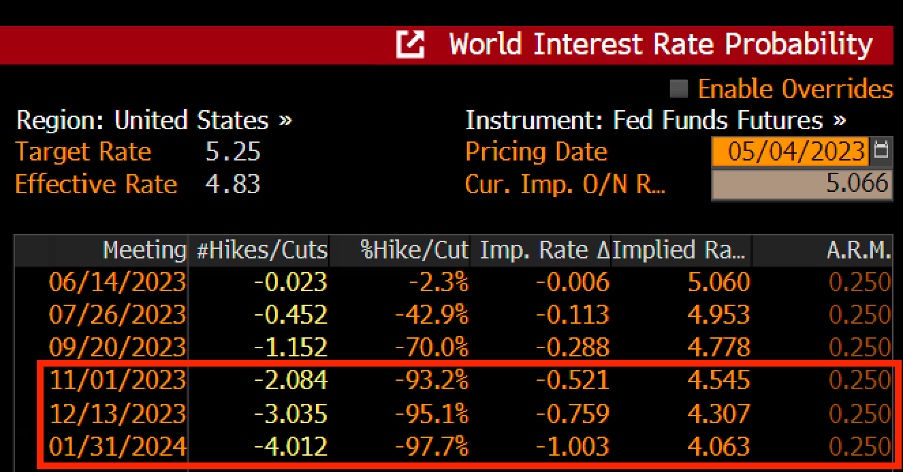

Post-May’s FOMC meeting, the bond market expects no further rate hikes while pricing-in rate cuts from November’s FOMC meeting onward. Assuming the bond market’s expectation is “correct”, no further rate hike would be regarded as a positive factor from an equity valuation perspective. However, earnings’ growth needs to bottom and continue to improve in order to sustain a turnaround in the broader equity market that remains pricey for now.

Table 2: Bond Market ~ expects no more rate hike for 2023 & priced-in rate cuts to ensue from November 2023 onwards.

Source: Airo Malaysia, Bloomberg.

Airo’s strategy remains unchanged by being nimble in both strategic & tactical asset allocations. Rest assured that Airo will continue to seek out and capitalize on potential market mispricing opportunities to generate positive alpha steadily for the BOCA portfolios.

May 5th, 2023

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.