CIO Letter – May 2024: Airo-BOCA +2.87% – Resiliency amid markets’ downturn!

Highlights:

#1

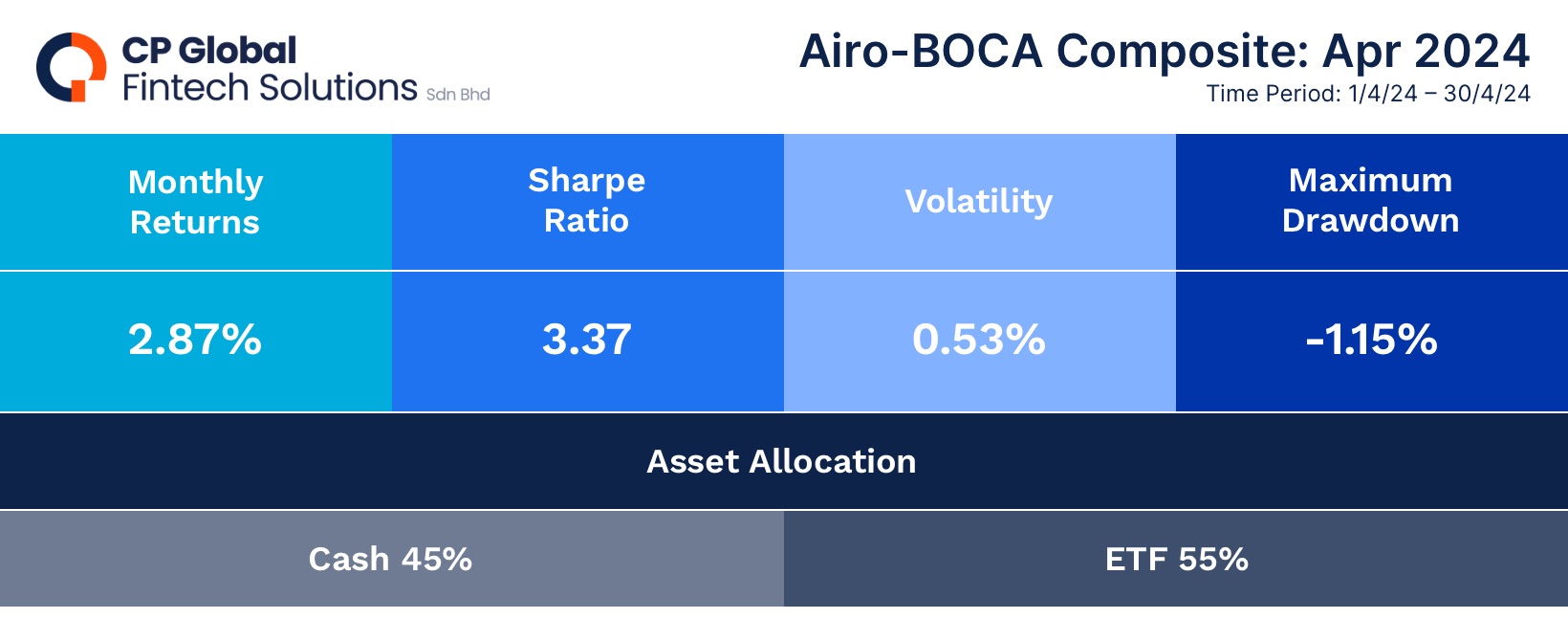

Global equity correction was the theme for April with MSCI ACWI Index and S&P500 Index declining by -3.55% and -4.16% respectively. In contrast, Airo-BOCA portfolios’ composite demonstrated remarkable resilience, registering a positive return of +2.87% in USD terms for the month.

#2

Amid the turbulent market conditions in April, Airo-BOCA thrived due to its strategic hedging positions and core long positions in gold, cannabis, and China. Looking ahead, Airo remains committed to its proactive approach, maintaining a nimble stance in adjusting both hedging and long positions through active rebalancing strategies.

#3

The persistent U.S’ inflationary pressure continues to be a significant concern, as evidenced by the stubbornness reflected in March’s CPI, PPI & PCE data. Furthermore, April’s ISM Manufacturing Prices Paid surged to a level not seen since 2022, further emphasizing the enduring nature of inflationary pressures.

#4

On the macroeconomic growth front, the unexpected contraction in the U.S manufacturing growth during April marked a notable deviation from the upward trajectory observed in March. This inconsistency underscores the patchy nature of macro growth in the U.S., exemplified by the ISM Manufacturing PMI fluctuating between periods of expansion and contraction in recent months.

#5

On the microeconomic front, the first-quarter earnings reports from major technology companies revealed a consistent trend: while results met expectations, the market anticipated stronger forward guidance for the second quarter and beyond. This suggests that the bar for earnings expectation going forward is set high, especially considering the significant year-to-date rally of technology firms.

– – –

Dear Valued Investors,

Global equities saw massive volatility throughout April and ended the month with the MSCI ACWI Index and S&P500 Index declining by -3.55% and -4.16% respectively. In contrast, Airo-BOCA portfolios’ composite demonstrated remarkable resilience, registering a positive return of +2.87% in USD terms for the month.

Table 1: AIRO-BOCA Composite ~ Performance Matrix (April 2024)

Amid the turbulent market conditions in April, Airo-BOCA thrived due to its strategic hedging positions in technology and small cap. sectors as well as the positive return of its core long positions in gold, cannabis, and China. Given the macro headwinds as lamented in the following paragraphs, in the interim, Airo shall continue its active rebalancing strategy with a nimble positioning in both hedging and long positions. At the current juncture, equity allocation is slightly higher at 55% from 52% while the rests remain in cash.

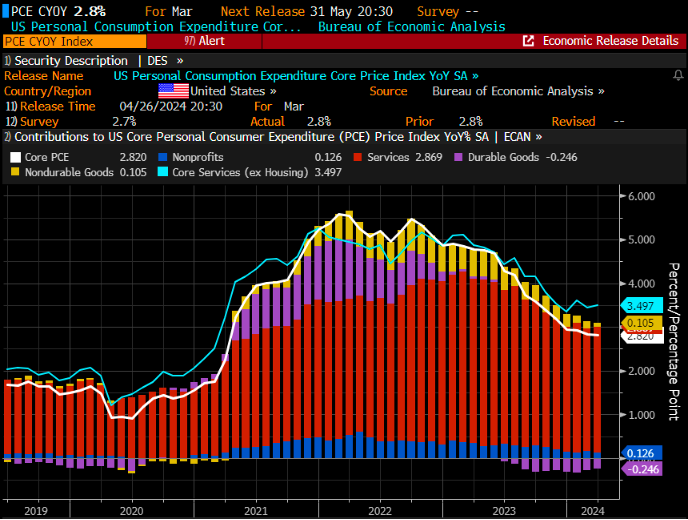

The persistent U.S’ inflationary pressure remains a significant concern, as evidenced by the stubbornness reflected in March’s CPI, PPI & PCE data. Furthermore, April’s ISM Manufacturing Prices Paid hit a new high since 2022 and this underpinned that inflationary pressures remain broadly intact from both consumers and manufacturing perspective.

Chart 1: Core PCE Deflator (YoY) ~ remained sticky at +2.8% with Supercore PCE at +3.5%

Chart 2: ISM Manufacturing Prices Paid ~ consistently higher & hit new high since 2022

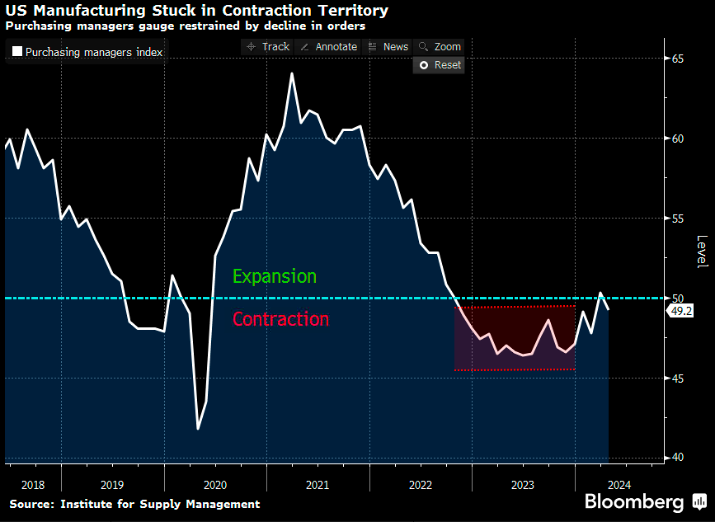

On the macroeconomic growth front, the U.S manufacturing growth as proxied by the ISM Manufacturing PMI cratered in contraction unexpectedly in April as it failed to maintain its growth trajectory as seen in March. As such, U.S macro growth remains patchy given that its ISM Manufacturing PMI churned back into contraction again after only one month into growth in March.

Chart 3: ISM Manufacturing PMI ~ back into negative growth for April 2024

On the microeconomic front, most of the technology companies (except Nvidia) reported the 1Q earnings result as summarized below. In a nutshell, the post result price action can be interpreted as the market setting a higher bar of expectation going into 2Q given the already stellar share price performance on a year-to-date basis.

- ASML Holding ~ bad 1Q revenue -20% yoy and EPS -37% yoy as its most advanced chip making machines fell short of its sales’ expectation. Forward guidance on its growth recovering hinged on a potentially better outlook in 2025 only. Its share price tumbled -7% post result.

- Netflix ~ good earnings but forward guidance hinted a slowing growth by stopping ARPU & new subscribers’ statistics going forward. Its share price tumbled -9% post result.

- Tesla ~ missed on both 1Q revenue -9% yoy and EPS -34% but rallied +12% post result on something else unrelated to earnings & guidance, i.e. on the preliminary approval for its full self-driving system in China with a flare of meme returning to the stock.

- Meta ~ good 1Q result as revenue +28 yoy but the market was spooked by its unexpected huge capex. plan that is going to eat into the forward earnings’ potential in the interim as warned by Zuckerberg. Its share price tumbled -11% post result.

- Google ~ good 1Q rev +16% and EPS +62% while beating expectations & it rallied +10% post result.

- Microsoft ~ good 1Q revenue +17% yoy and EPS +20% yoy while beating expectation and guided +10% to +13% yoy revenue growth for 2Q. Its share price +2% only post result.

- Amazon ~ good 1Q revenue +12% yoy and EPS +227% yoy but the 2Q revenue forward guidance was below the range of the existing expectation of $150 billion at $144b – $149 billion range. Its share price +3% only post result.

- SMCI ~ good 1Q revenue +160% yoy and EPS +308% yoy and forward guidance for 2Q was good at $5.3b versus existing expectation of $4.9b; however, stock fell -14% post result as the market was expecting an even higher guidance given that the stock had rallied +350% on a year-to-date basis.

- Apple ~ bad 1Q revenue -4% yoy and EPS was flat; however, stock rose +6% as the negative result was better-than-expected!

May 4th, 2024

William Yii

CIO, CP Global Fintech Solutions

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.