CIO Letter – May 2025: Fast & Furious, But, What Now?

Highlights:

#1

April’s sharp correction was swiftly followed by a striking rebound, with U.S. equities seemingly brushing off Trump’s tariff rhetoric as if nothing happened! As a result, the S&P 500 ended the month with only a modest decline of -0.76%, while the MSCI ACWI posted a gain of +0.52%.

#2

In comparison, the Airo-BOCA Composite declined by -2.7%, weighed down primarily by its hedging positions. The Airo-Shariah Composite also fell by -1.84%, driven largely by weakness in consumer and pharmaceutical stocks.

#3

The pressing question remains: what has fundamentally changed over the past month? The short answer–not much. Although the U.S. and China have resumed dialogue, the current de-escalated tariff rate on Chinese goods still stands at 30%, which is expected to weigh on U.S. GDP growth in the near term.

#4

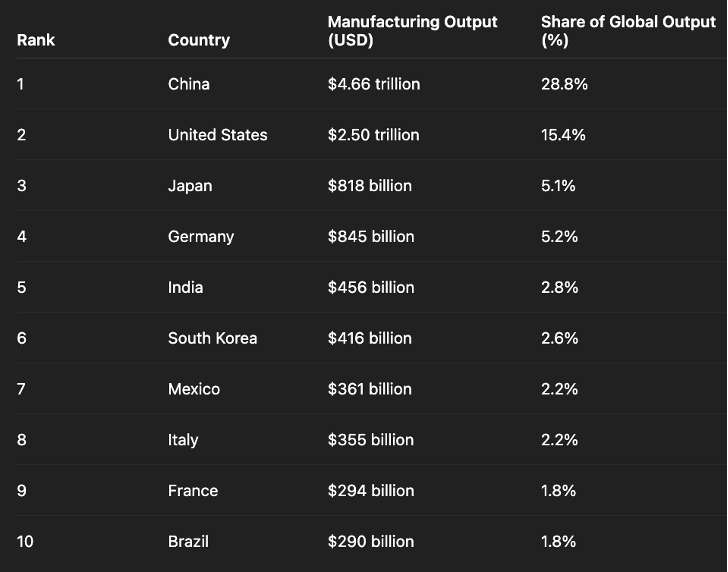

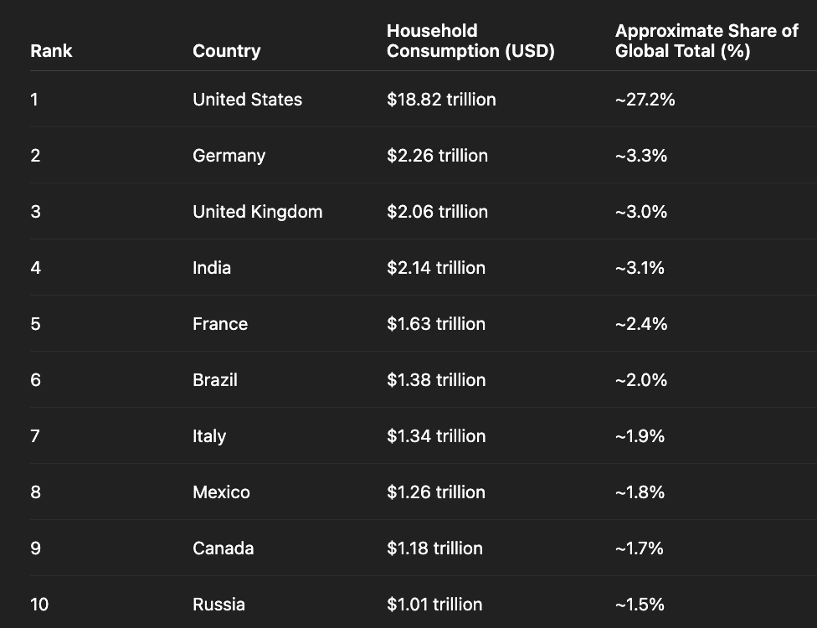

From China’s perspective, exports to the U.S. amount to approximately $0.5 trillion. To put this into context, China is responsible for manufacturing one-third of global goods, while U.S. households consume about one-third of global output. In other words, the livelihood of millions of Chinese factory workers is directly tied to this trade relationship.

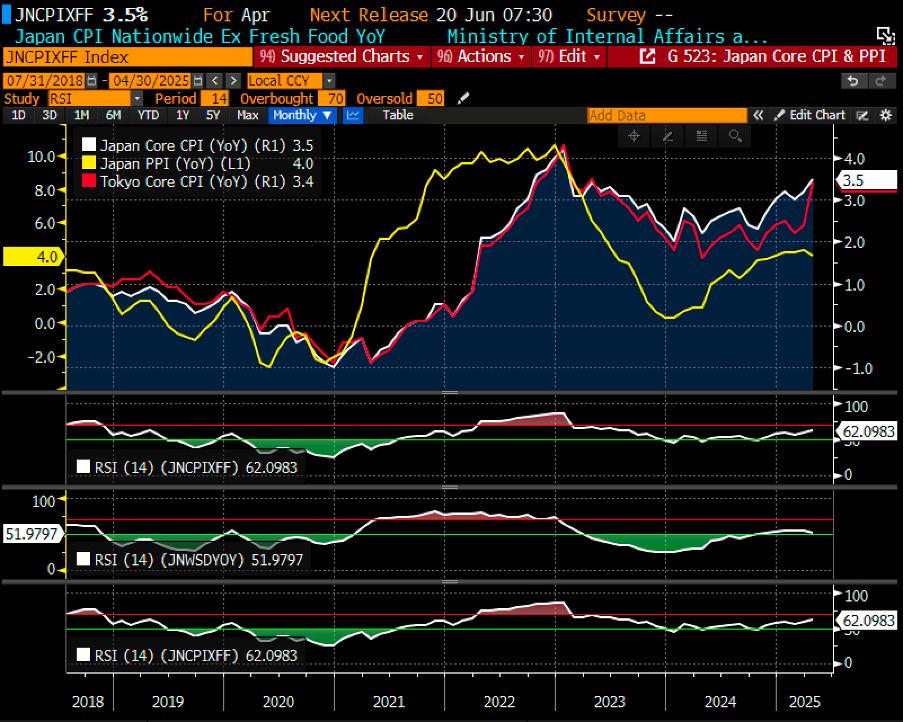

#5

Japan continues to grapple with persistent inflationary pressures, as core inflation stays firmly above 3.0% year-on-year. This has placed mounting pressure on the Bank of Japan (BOJ), particularly in light of its decision to leave interest rates unchanged at the May policy meeting.

– – –

Dear Valued Investors,

The sharp correction in April was followed by an equally dramatic rebound, as U.S. equities appeared to shrug off Trump’s tariff rhetoric entirely. Despite an initial drawdown of around -15% following Trump’s ‘Liberation Day’ announcement, the S&P 500 managed to rally +16% from its April low, ultimately ending the month with a modest decline of just -0.76%. April 2025 will be remembered as one of the most volatile months in global equity market history.

Chart 1: S&P500 whipsaw +15% in both direction and closed down -0.75% in April 2025

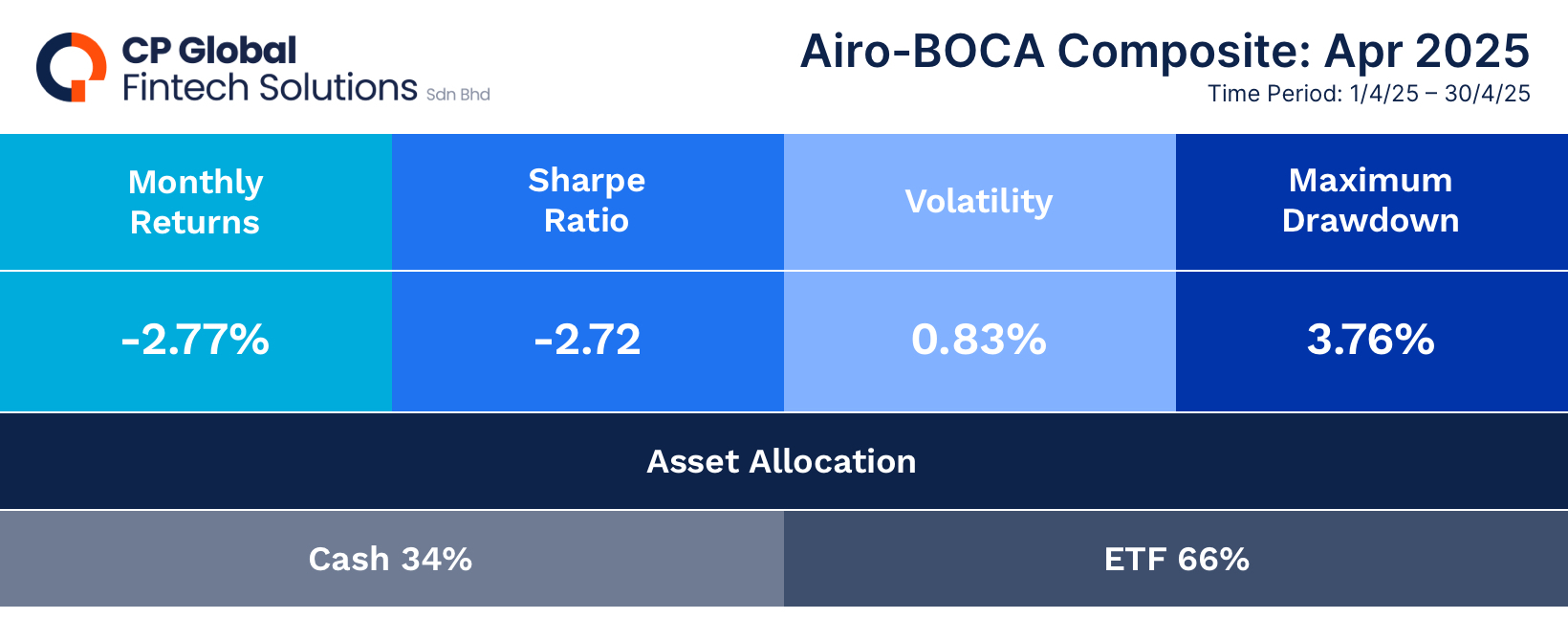

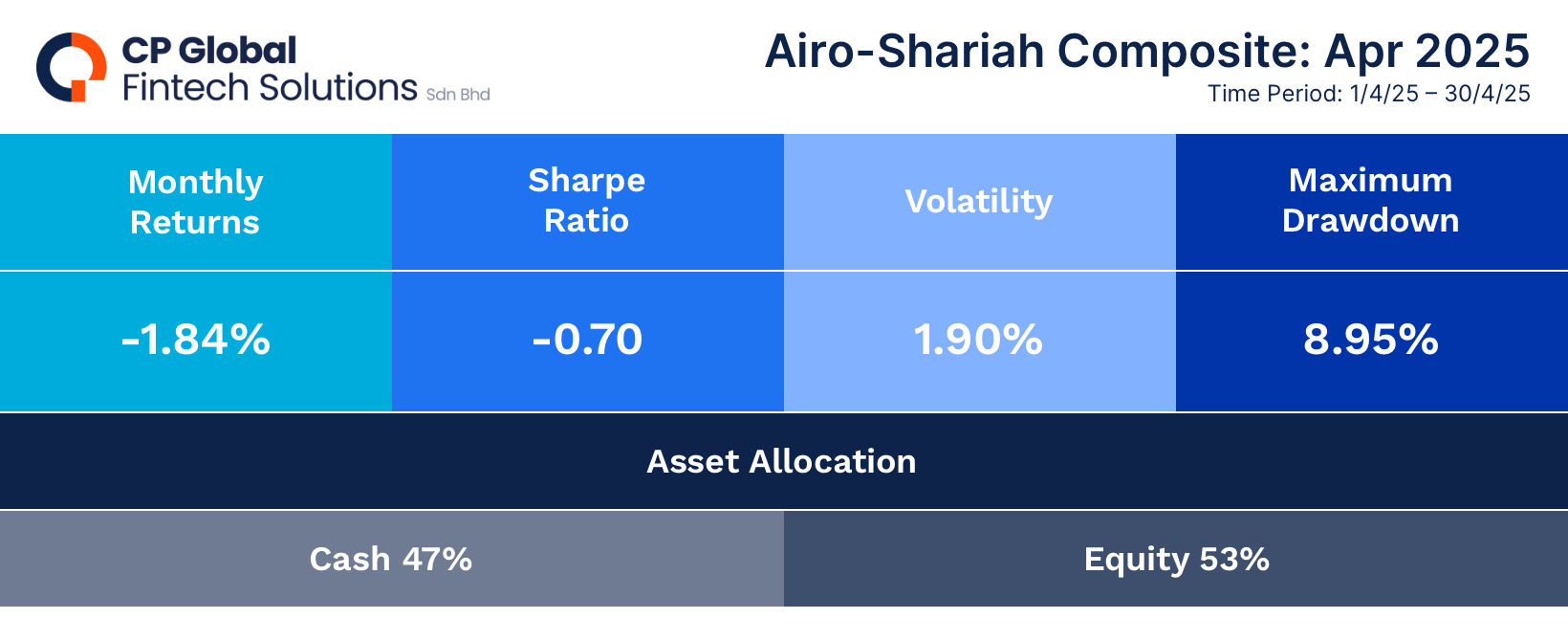

In comparison, the Airo-BOCA Composite was down -2.7% as it was negatively impacted by the hedging positions. Meanwhile, the Airo-Shariah Composite also declined by -1.84% largely attributed to underperformance in consumer and pharmaceutical stocks.

Table 1: Airo-BOCA Composite Performance (April 2025)

Table 2: Airo-Shariah Composite Performance (April 2025)

The pressing question is: what has fundamentally changed over the past month? The short answer–not much. Although the U.S. and China have resumed dialogue, the de-escalated tariff on Chinese goods remains at 30%. Since tariffs on Chinese imports effectively act as a tax on U.S. consumers, this is expected to weigh on U.S. GDP growth in the near term.

From China’s perspective, exports to the U.S. total approximately $0.5 trillion. For context, China manufactures one-third of global goods, while U.S. households consume about one-third of global output. This interdependence underscores the stakes: the livelihoods of China’s 120 million factory workers–out of a total labor force of 740 million–are closely tied to the strength of this trade relationship.

Table 3: China manufactures 1/3 of total global output

Table 4: U.S household consumes 1/3 of total global consumption

Japan continues to face persistent inflationary pressure, with core inflation remaining firmly above 3.0% year-on-year. As a result, the Bank of Japan (BOJ) is under mounting pressure, particularly following its decision to hold rates steady at the May policy meeting. Assuming inflation shows no signs of easing in the coming months, we expect the BOJ to resume its path of interest rate hikes.

Chart 2: Japan’s Core CPI is at 3.5% as of April 2025, i.e. 150 basis points above the 2% target!

May 23rd, 2025

William Yii

CIO, CP Global Fintech Solutions.

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.