Nov 2022: A challenging environment driven by unrelated macro fundamentals

Highlights:

#1

Airo-BOCA composite closed October with -3.91% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) with +6.35% and +7.99% respectively. The negative return in October was solely due to the hedging positioning. On a YTD basis as of October 2022, Airo-BOCA composite flipped back into negative territory at -2.86% but remained solidly outperforming ACWI & SPX at -21.74% & -18.76% respectively.

#2

Airo’s October performance underlies a very challenging environment driven by unrelated macro fundamentals. Specifically, S&P500 was largely flat until Oct 21st when Fed. Daly dovishly remarked on the need to start considering a slow-down in rate hikes followed swiftly by a Wall Street Journal’s article whispering that the Fed. might be pausing/pivoting on future rate hikes. Consequently, S&P500 engineered another bear market rally of +7%.

#3

Fundamentally speaking, however, the rally made no sense as macro data had in fact worsened with the hawkish September headline of CPI at +0.4% MoM and 8.2% YoY while Core CPI was at +0.6% MoM and 6.6% YoY. In addition, Core PCE Deflator was also hawkish at +0.5% MoM and +5.1% YoY.

#4

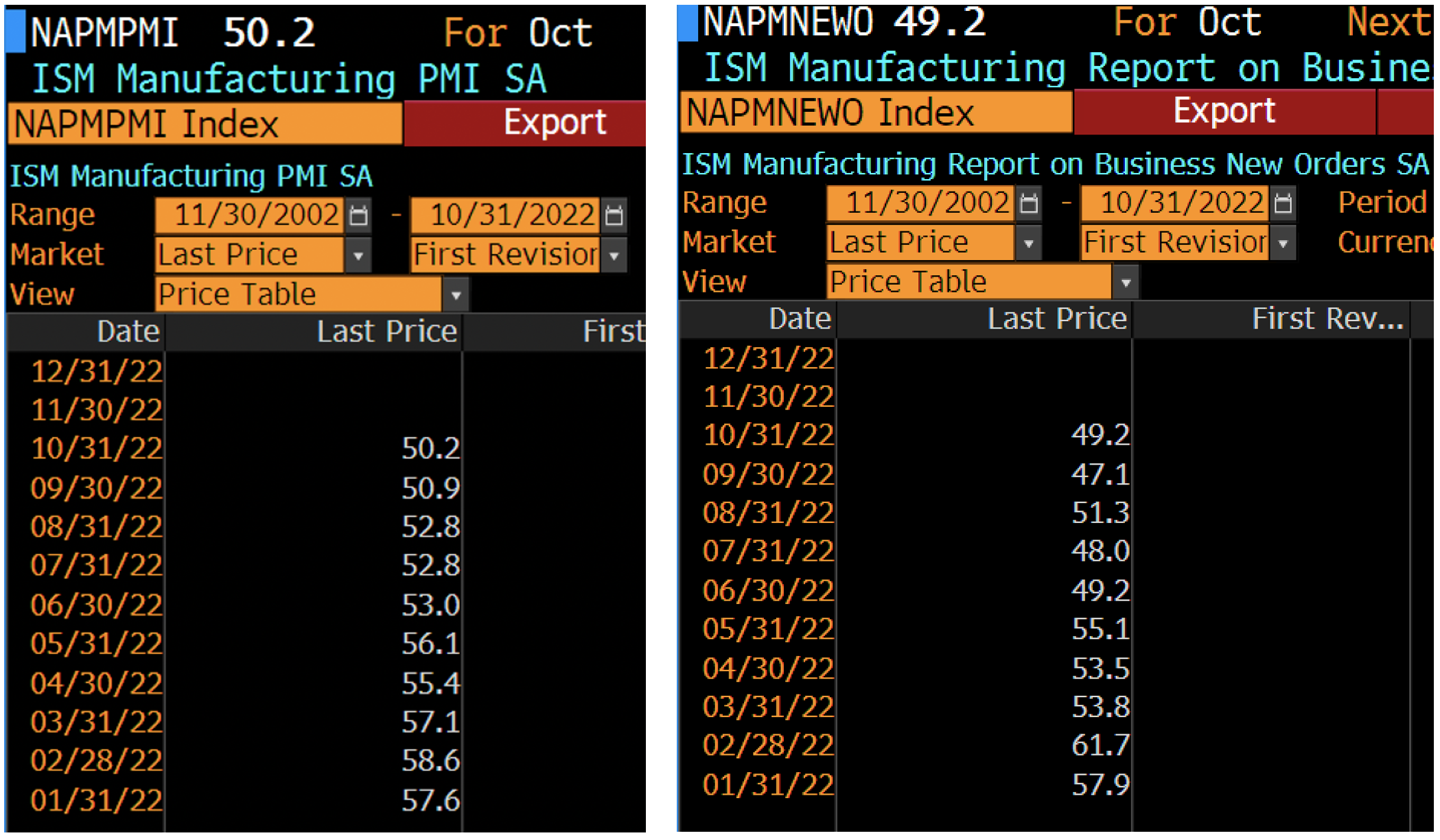

Likewise, U.S. macro growth deteriorated further where ISM Manufacturing PMI inched closer to contraction at 50.2 from 50.9. While ISM New Orders unexpectedly improved to 49.2 from 47.1, it remained in contraction zone i.e. below 50. The dwindling U.S. manufacturing output would have a direct repercussion on corporate earnings’ growth trajectory in general, albeit with some lag.

#5

3Q2022 U.S corporate earnings result was uninspiring with a central theme of revenue & earnings peaking a few quarters ago. FAAMG stocks reported slower or negative revenue/earnings on a sequential and year-on-year basis. Although corrections had already ensued on a YTD basis, given the high PE base and negative growth outlook in 2023, valuations remain a tad pricey for now.

#6

Given the very volatile investment backdrop as well as critical inflation & growth narratives, rest assured that Airo shall continue to actively maneuver our strategic & tactical asset allocation to safely navigate your portfolios throughout this challenging period.

– – –

Dear Valued Investors,

Airo-BOCA composite closed October with -3.91% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) with +6.35% and +7.99% respectively. The negative return in October was solely due to the hedging positioning. On a YTD basis as of October 2022, Airo-BOCA composite flipped back into negative territory at -2.86% but remained solidly outperforming ACWI & SPX at -21.74% & -18.76% respectively.

Table 1: Airo-BOCA YTD Performance – As of October 2022

Source: Interactive Brokers, Airo Malaysia.

Airo’s October performance underlies a very challenging environment driven by the unrelated macro-fundamentals. Specifically, S&P500 was largely flat until Oct 21st when Fed. Daly dovishly remarked on the need to start considering a slow-down in rate hikes followed swiftly by a Wall Street Journal’s article whispering that the Fed. might be pausing/pivoting for future rate hikes. Consequently, S&P500 rallied almost +7% by the end of October.

This rally, however, did not make any fundamental sense as macro data had worsened during the month with the hawkish September headline of CPI at +0.4% MoM and 8.2% YoY while Core CPI was at +0.6% MoM and 6.6% YoY respectively. In addition, Core PCE Deflator was hawkish at +0.5% MoM and +5.1% YoY respectively.

Chart 1: S&P500 engineered a bear market rally of 7% after the Fed. Daly & WSJ’s dovish whisper

Source: Bloomberg, Airo Malaysia.

On U.S. macro growth proxy, likewise, the ISM Manufacturing PMI inched closer to contraction at 50.2 from 50.9. While ISM New Orders unexpectedly improved to 49.2 from 47.1, it remained in contraction zone i.e., below 50. The dwindling U.S. manufacturing output would have a direct repercussion on corporate earnings’ growth trajectory in general, albeit with some lag.

Table 2: ISM Manufacturing PMI & ISM New Orders PMI

Source: Bloomberg, Airo Malaysia.

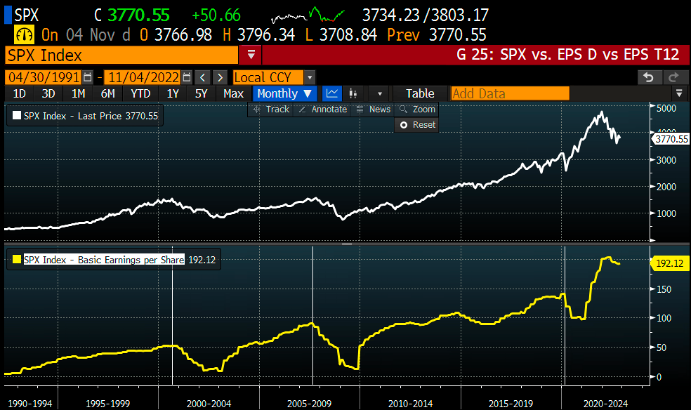

The 3rd quarter U.S corporate earnings was uninspiring for FAAMG with a central theme of revenue & earnings peaking a few quarters ago: Facebook (Meta)’s EPS imploded -33% QoQ; Apple reported +4% EPS YoY; Amazon reported -9% EPS YoY; Microsoft’s adjusted EPS growth was at +4% YoY; Google (Alphabet) reported a single digit quarterly revenue growth for the first time at +7%. More importantly, the forward revenue guidance is bleak while Apple failed to give any guidance citing global economic uncertainty.

Chart 2: S&P500 Index vs. Earnings Per Share’s Trend

Source: Bloomberg, Airo Malaysia.

Given the very volatile investment backdrop as well as critical inflation & growth narratives, rest assured that Airo shall continue to actively maneuver our strategic & tactical asset allocation to safely navigate your portfolios throughout this challenging period.

November 5th, 2022

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.