CIO Letter – Nov 2023: 🧭 Manoeuvring through an uncertain macro backdrop

Highlights:

#1

For October 2023, the Airo-BOCA composite declined by -1.13%. Once again, it continued to maintain a performance edge over both the MSCI All Country World Index (ACWI) and S&P500 Index (SPX) which were down by -2.54% & -2.20% respectively. The resilience of the Airo-BOCA composite was mainly attributed to our strategic allocation in gold, which underscores our robust risk management approach in safeguarding asset value during periods of economic uncertainty.

#2

Macro data have been mixed of late where hard data like factory orders & durable goods orders had a positive growth trajectory. Conversely, soft data like ISM Manufacturing & Services PMIs saw a sudden reversal that reversed the previous months’ hopeful rebound.

#3

Likewise, October’s NonFarm Payrolls saw a huge downward reversal to 150k coupled with unemployment rate ticking up to 3.9%. These pointed to a softening labour market growth condition whereby further labour market deterioration may persist in the coming months.

#4

Translating the macro data rhetoric into a broader growth perspective, the relentless nominal yield’s rally has stopped & is reversing together with the crude oil prices. Both yields and crude oil are important macro growth’s proxies that are hinting an incoming slowing macro growth!

#5

Airo remains steadfast in its conservative approach to strategic and tactical asset allocations, emphasizing the dual objectives of capital preservation and the pursuit of alpha generation amidst a challenging market environment. The decision to increase equity exposure will be judiciously measured against our ongoing analysis of the global macroeconomic climate, with forthcoming quarters offering critical data points to make an informed asset allocation decisions.

– – –

Dear Valued Investors,

For October 2023, the Airo-BOCA composite declined by -1.13%. Once again, it continued to maintain a performance edge over both the MSCI All Country World Index (ACWI) and S&P500 Index (SPX) which were down by -2.54% and -2.20% respectively. The resilience of the Airo-BOCA composite was mainly attributed to our strategic allocation in gold, which underscores our robust risk management approach in safeguarding asset value during periods of economic uncertainty. The detractors for the month were South-East Asia equity and U.S Treasury exposures.

Table 1: On a year-to-date basis, Airo-BOCA returned -7.75% in USD Term (As of October 2023)

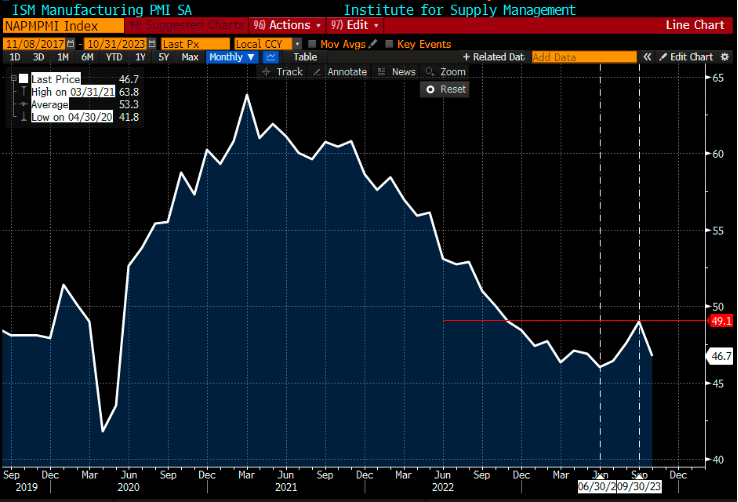

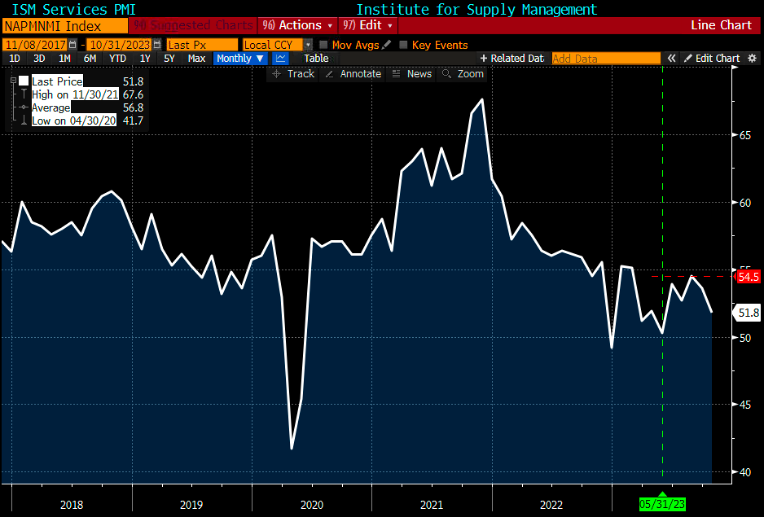

Macro data have been mixed of late where hard data like factory orders & durable goods orders saw positive growth of +2.8% MoM and +4.6% MoM respectively in September. Conversely, soft data like ISM Manufacturing & Services PMIs saw a sudden reversal that reversed the previous months’ hopeful rebound. In October, ISM Manufacturing PMI contracted to 46.7 from 49.0 while ISM Services PMI softened to 51.8 from 53.6 respectively. It would be interesting to see if the hard data follow-through with more weakness as seen in the ISM PMIs.

Chart 1: ISM Manufacturing PMI ~ contracted to 46.7 from 49.0

Chart 2: ISM Servics PMI ~ softened to 51.8 from 53.6

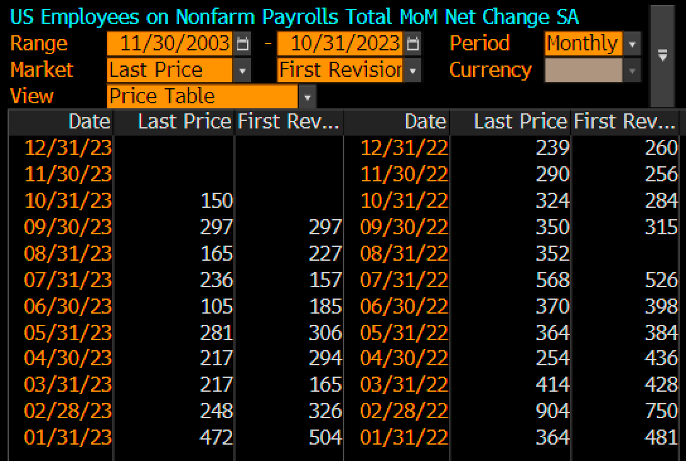

Likewise, October’s NonFarm Payrolls saw a huge downward reversal to 150k from 297k in September. Unemployment rate also ticked up to 3.9% from 3.8%. These data pointed to a softening labour market growth condition whereby further labour market deterioration may persist in the coming months. If this is indeed the case, labour recession could be incoming and can promptly imply a boarder economic recession that is currently not being priced by the equity market.

Table 2: U.S NonFarm Payrolls ~ reversed to 150K after a strong spike in September

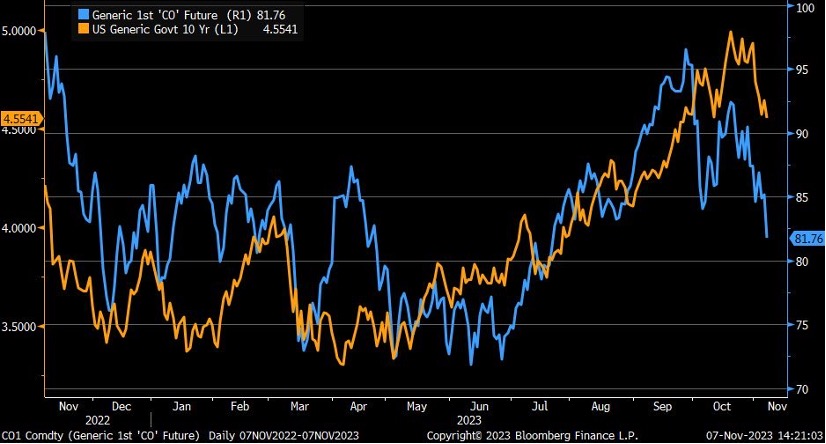

Translating the above macro data rhetoric into a broader growth perspective, the relentless nominal yield’s rally has stopped where the U.S Treasury 10-Year yield peaked at 5.0% & is now reversed to 4.5%. Concurrently, the recent crude oil prices’ spike to $95 has plunged to $78 per barrel! Both yields and crude oil are important macro growth’s proxies that are attempting to price-in a slowing global-macro growth ahead.

Chart 3: U.S Treasury 10-Year Yield & Crude Oil Prices ~ reversing lower!

Airo remains steadfast in its conservative approach to strategic and tactical asset allocations, emphasizing the dual objectives of capital preservation and the pursuit of alpha generation amidst a challenging market environment. This prudent stance underscores our commitment to protecting the investment base while also seeking opportunities for outperformance.

The decision to increase equity exposure will be judiciously measured against our ongoing analysis of the global macroeconomic climate, with forthcoming quarters offering critical data points to make an informed asset allocation decisions. Our team is dedicated to a disciplined investment process that balances potential risks and rewards, always with an eye toward the evolving economic indicators and trends that will shape the long-term investment landscape.

Nov 8th, 2023

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.