Oct 2022: Airo composite closed Sep with +2.42% 🎯

Highlights:

#1

Airo-BOCA composite closed September with +2.42% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) with -9.39% and -9.34% respectively. On a YTD basis as of September 2022, Airo-BOCA composite flipped back into positive territory at +1.09% versus ACWI & SPX at -26.41% & -24.77% respectively. Airo’s big outperformance was contributed by the timely tactical hedging / short allocation & gold miners’ exposure.

#2

September’s severe equity correction forcefully ensued after the release of the U.S August’s inflation data where its Core CPI has gone higher from +5.9% to +6.3% year-on-year and +0.3% to +0.6% month-on-month. This had titled the consensus’ expectation that the inflationary pressure had peaked previously and is in-line with September’s FOMC meeting’s hawkish guidance.

#3

On a macro growth perspective, ISMs continued to churn lower and in particular the ISM New Orders has resumed into negative growth at 47.1 from 51.3. ISM Manufacturing is also nearing growth contraction zone at 50.9 from 52.8. Our expectation is that the macro growth shall continue to deteriorate and negatively impact corporate earnings’ growth trajectory.

#4

Lastly, despite the relatively fast pace of global central banks’ interest rate tightening measures on a year-to-date basis, global real rates / yields are still at low levels from a historical perspective. The implication is that real yields look set to go higher with more incoming interest rate hikes and this has a negative impact to equity valuations.

#5

Given the very volatile investment backdrop coupled with deteriorating inflation & growth narratives, rest assured that Airo shall continue to actively maneuver our strategic & tactical asset allocation to safely navigate our investors through this challenging period.

– – –

Dear Valued Investors,

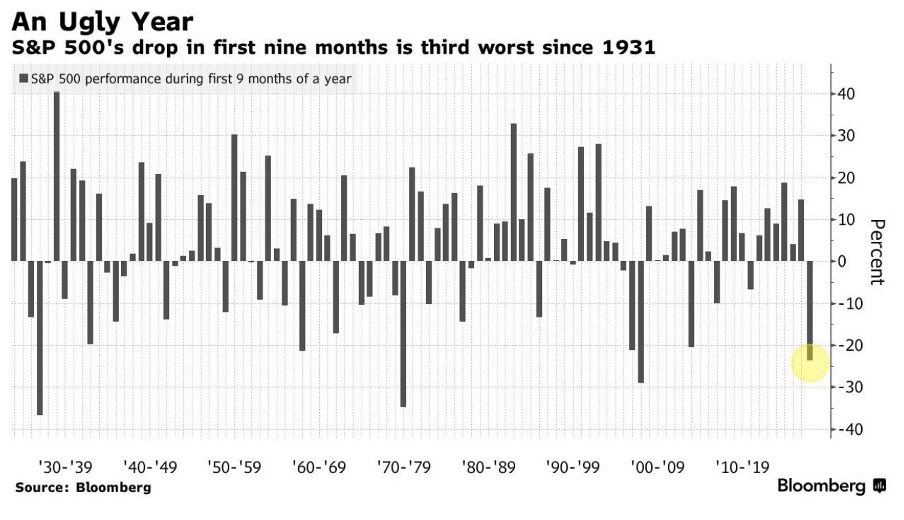

Airo-BOCA composite closed September with +2.42% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) with -9.39% and -9.34% respectively. On a YTD basis as of September 2022, Airo-BOCA composite flipped back into positive territory at +1.09% versus ACWI & SPX at -26.41% & -24.77% respectively. Airo’s big outperformance was contributed by the timely tactical hedging / short allocation & gold miners’ exposure. Incidentally, for perspective, year-to-date as of September 2022 was the third worse performing period for S&P500 Index since 1931.

Table 1: Airo-BOCA YTD Performance – As of September 2022

Source: Interactive Brokers, Airo Malaysia.

Chart 1: Year-To-Date September Performance From A Historical Perspective

Source: Bloomberg, Airo Malaysia.

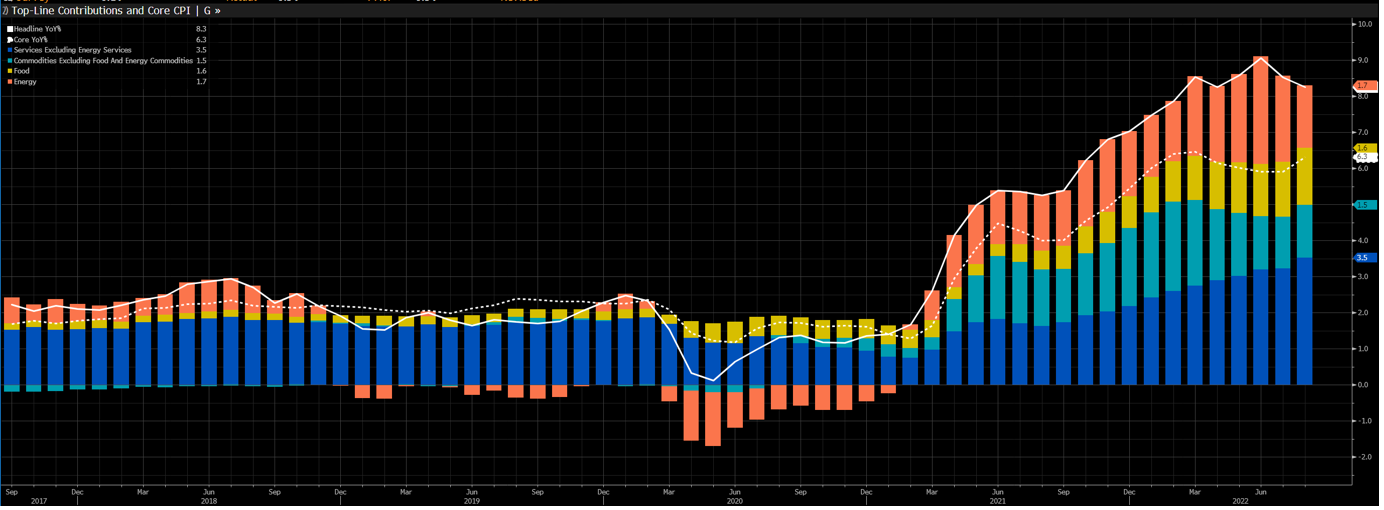

September’s severe equity correction forcefully ensued after the release of the U.S August’s inflation data where its Core CPI has gone higher from +5.9% to +6.3% year-on-year and +0.3% to +0.6% month-on-month. Although the Headline CPI cooled off slightly due to lower energy prices in the U.S, the services inflation has ticked up and contributed to the increase in the Core CPI. The simple truth is that services inflation tends to be sticky as once the services prices went up, it usually would not come down easily i.e., it behaves differently from a goods inflation. As a result, this had titled the consensus’ expectation that the inflationary pressure had peaked previously and is now in-line with September’s FOMC meeting’s hawkish guidance.

Chart 2: U.S Inflation – Services Inflation Caused The Core Inflation To Tick Up

Source: Bloomberg, Airo Malaysia.

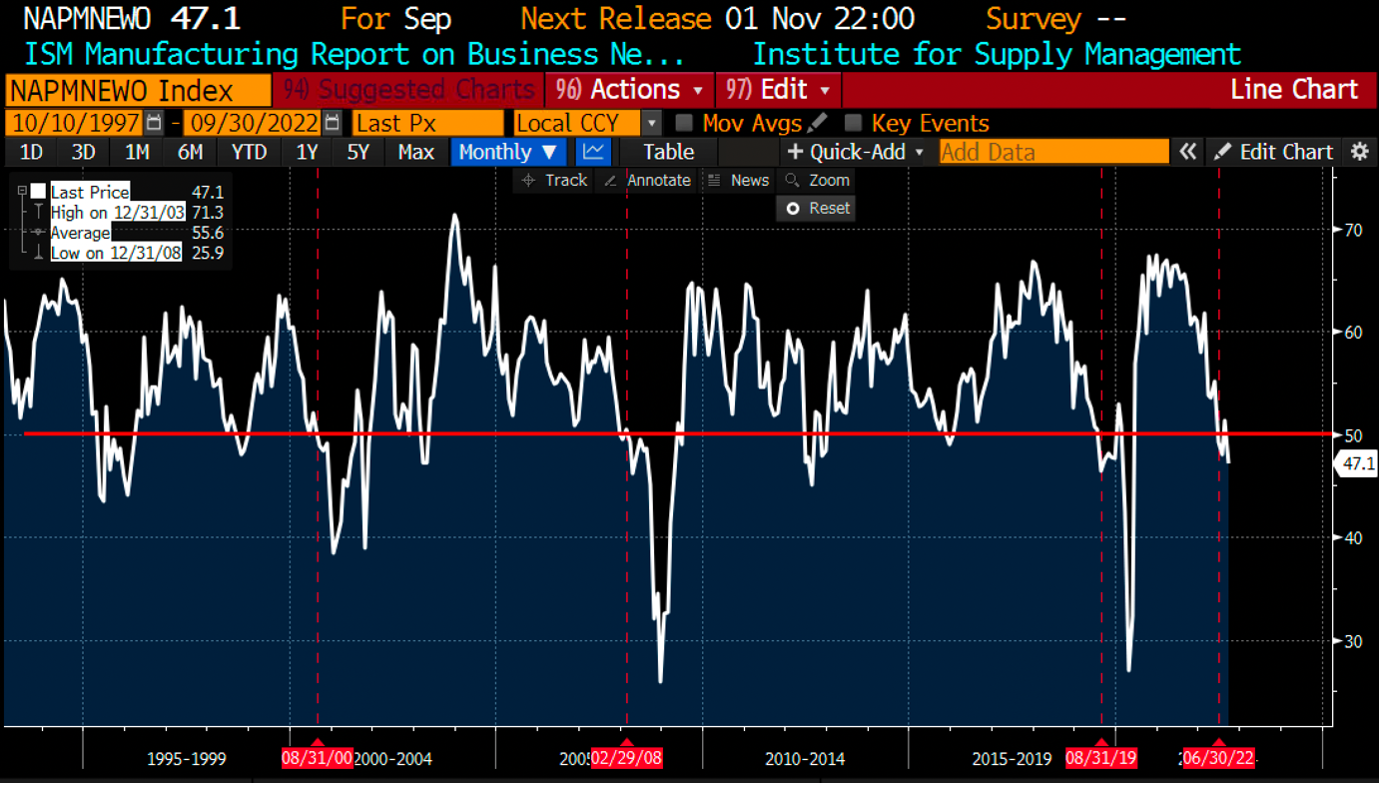

On a macro growth perspective, ISMs continued churning lower and in particular the ISM New Orders has resumed into negative growth at 47.1 from 51.3. ISM Manufacturing is also nearing growth contraction zone at 50.9 from 52.8. Our expectation is that the macro growth shall continue to deteriorate and potentially negatively impact corporate earnings’ growth trajectory.

Chart 3: ISM New Orders – Resuming Its Negative Growth Since June 2022

Source: Bloomberg, Airo Malaysia.

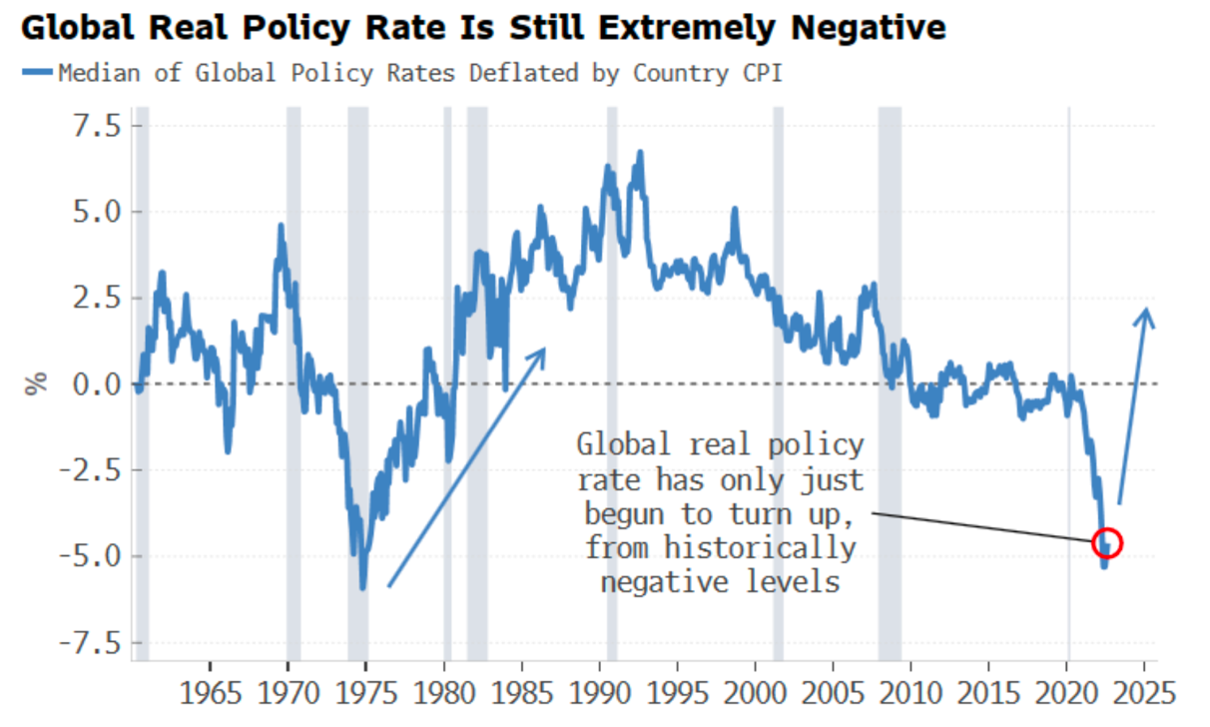

Lastly, despite the relatively fast pace of global central banks’ interest rate tightening measures on a year-to-date basis, global real rates / yields are still at low levels from a historical perspective. What this means is that the real yields are looking set to go higher with more incoming interest rate hikes. The direct implication to equity valuation on higher nominal and real yields would be lower equity prices assuming corporate earnings’ growth continue to disappoint.

Chart 4: Global Real Rates / Yields Has Ample Upside Room

Source: Bloomberg, Airo Malaysia.

Looking ahead, given the very volatile investment backdrop coupled with deteriorating inflation & growth narratives, rest assured that Airo shall continue maneuvering its strategic & tactical asset allocation diligently to safely navigate our investors through this challenging period.

October 4th, 2022

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.