CIO Letter – Oct 2023: The concern of relentless rising bond yields

Highlights:

#1

For September 2023, the Airo-BOCA composite declined by 2.99%. However, it still outperformed both the MSCI All Country World Index (ACWI) and S&P500 Index (SPX) which were down -4.28% & -4.87% respectively. Airo’s outperformance was mainly attributed to our nimble asset allocation strategy of equity versus cash.

#2

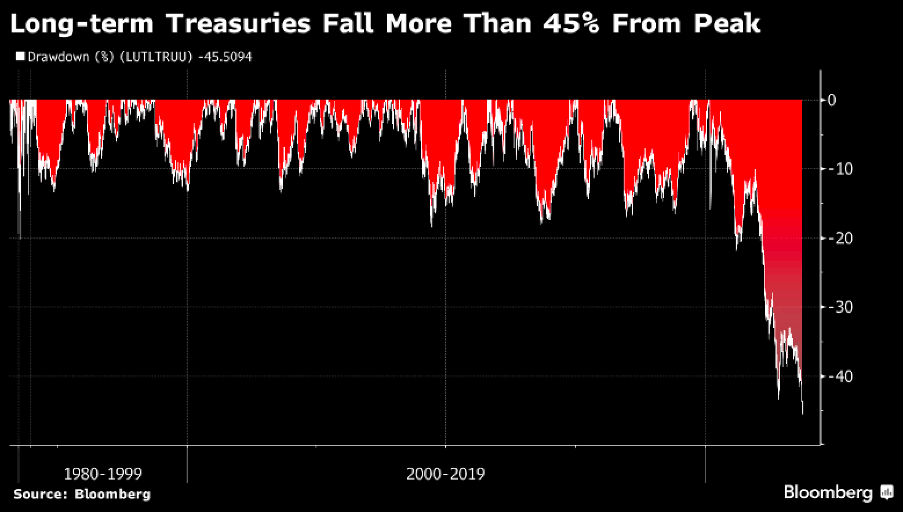

The relentless U.S Treasury yields’ rally of late has caused havoc to the U.S bond markets. Since peaking in March 2020, U.S bonds with maturities of 10 years and longer have seen a 46% decrease in market value. This represents the most severe bond market rout in history.

#3

One key concern is why has the demand for U.S Treasury weakened so noticeably, especially when the U.S Treasury 10-year yield jumped from 3.8% at the end of July to its current high of 4.8%? The primary cause might not necessarily be related to the expectation of higher incoming inflation or growth trajectory.

#4

Instead, the recent sell-off in bonds could very well be due to the technical dynamics of the U.S Treasury issuing a substantial volume of new bonds while the U.S Fed. continues its quantitative tightening agenda. With the People’s Bank of China (PBOC) consistently offloading its holdings and the Bank of Japan (BOJ) intending to end its Yield Curve Control (YCC) measures, all major holders are concurrently selling the U.S Treasury bonds.

#5

What’s next? From a macro-fundamental perspective, elevated bond yields can largely be sustained by a higher inflation or an upward growth trajectory. Considering the cooling inflationary pressures in major developed economies, namely, the U.S, Japan and the EuroZone, the relentless surge in bond yields might not have a strong fundamental basis.

#6

Airo continues to remain vigilant in its asset allocation strategy for the capital preservation of your investments. The conviction to deploy more capital into equities will be guided by our assessment of the global macroeconomic landscape in the upcoming quarters.

– – –

Dear Valued Investors,

For September 2023, the Airo-BOCA composite declined by 2.99% but outperformed both the MSCI All Country World Index (ACWI) and S&P500 Index (SPX) which were down -4.28% & -4.87% respectively. Airo’s outperformance was mainly attributed to our nimble asset allocation strategy of equity versus cash.

Table 1: On a year-to-date basis, Airo-BOCA returned -6.70% (As of September 2023)

The relentless U.S Treasury yields’ rally of late has caused havoc to the U.S bond markets. Since peaking in March 2020, the U.S bonds with maturities of 10 years and longer have seen a 45% decrease in market value. This represents the most severe bond market rout in history, rivaling the U.S equity correction during the Dot-com bubble at -49%.

Chart 1: U.S Bonds ~ percentage of correction from the respective peaks since 1980s

Given the severe bonds’ correction lately as the U.S 10-year treasury yield jumped from 3.8% at the end of July to its current high of 4.8%, one key concern is why has the demand for U.S Treasury weakened so noticeably? The answer could lie in the technicality of the U.S Treasury bonds market as opposed to the expectation of higher incoming inflation or higher growth trajectory.

Chart 2: U.S Treasury 10-Year Yield ~ rallied from 3.8% to 4.8% in the past one month

As the U.S Treasury Department issues a significant volume of new bonds to finance the government’s fiscal initiatives, it heavily relies on its largest buyers to bolster demand. Unfortunately, the U.S Fed. being the largest holder of U.S Treasury bonds, has consistently pursued its quantitative tightening agenda, meaning they’re selling off bonds to reduce the liquidity in the financial market. Meanwhile, the Bank of Japan (BOJ), the second-largest holder, has only marginally increased its bond purchases in recent months. To make the situation worse, the People’s Bank of China (PBOC) as the third largest holder has consistently been offloading bonds since the onset of the COVID-19 pandemic.

Chart 3: U.S Fed., PBOC ~ are net sellers while BOJ is marginal buyer of the U.S Treasury bonds

From a macro-fundamental perspective, elevated bond yields can largely be sustained by either a higher inflation expectation or an upward growth trajectory. Considering the cooling inflationary pressures in major developed economies, namely, the U.S, Japan and the EuroZone, and a current muted inflation expectation, a relentless surge in bond yields might not have a strong fundamental basis. As such, assuming incoming inflation data continues to cool, current high bond yields i.e., low bond prices present a good buy-the-dip opportunity.

Table 2: U.S, EuroZone & Japan ~ cooling core inflation

Airo continues to remain vigilant in its asset allocation strategy for the capital preservation of your investments. The conviction to deploy more capital into equities will be guided by our assessment of the global macroeconomic landscape in the upcoming quarters.

Oct 5th, 2023

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.