Sep 2022: Positioning our portfolios to seize opportunities as they arise

Highlights:

#1

Airo-BOCA composite closed the month of August at -2.03% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) at -4.36% and -4.24% respectively. On a YTD basis as of August 2022, Airo-BOCA composite slipped into negative territory at -1.30% versus ACWI & SPX at -18.79% & -17.02% respectively.

#2

Seasonality speaking, September tends to be a nasty month from a broad market performance perspective. And, given the upcoming September FOMC meeting, following a hawkish Jackson Hole meeting in August, markets could be setting up for another selloff opportunity!

#3

Looking ahead, however, assuming inflationary pressure as proxied by PCE Deflator & CPI can show any signs of peaking, markets may take this as an excuse to engineer another relief rally towards the end of the year.

#4

On the growth trajectory, August’s ISM PMIs showed a slight improvement in the orders & a sizable jump in employment while price pressure continued to decline. These may bode well for equity markets from a growth perspective assuming the improvement is sustainable over the coming months.

#5

Based on market conditions, Airo will likely be maintaining high cash levels towards the end of the year. However, we remain nimble in our approach and will seize opportunities if they arise, such as another relief rally if that is deemed probable. Our tactical allocation strategy will be titled towards a tactical long positioning (instead of a short) where we could take advantage of a possible year-end rally.

Dear Valued Investors,

Airo-BOCA composite closed the month of August at -2.03% versus MSCI All Country World Index (ACWI) and S&P500 Index (SPX) at -4.36% and -4.24% respectively. On a YTD basis as of August 2022, Airo-BOCA composite slipped into negative territory at -1.30% versus ACWI & SPX at -18.79% & -17.02% respectively.

Table 1: Airo-BOCA YTD Performance – As of August 2022

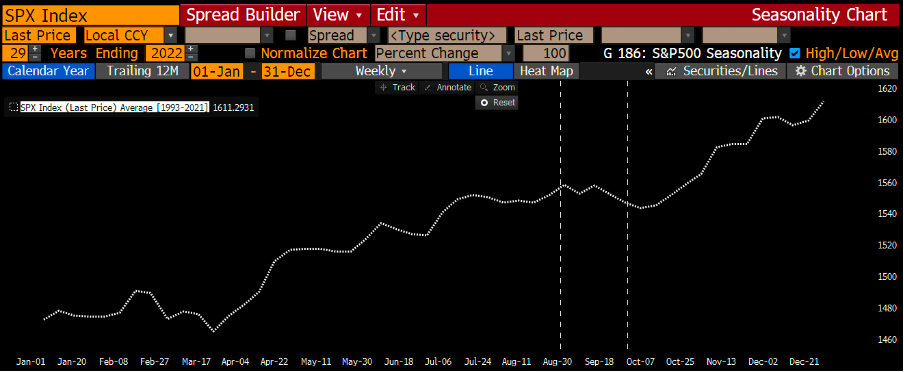

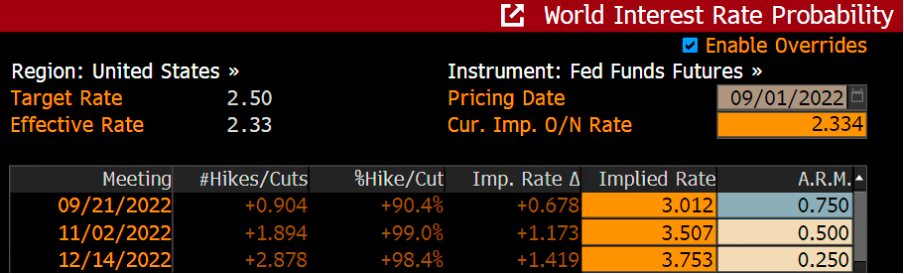

Seasonality speaking, September tends to be a nasty month from a broad market performance perspective. Over the past 30 years, S&P500 have seen sizable corrections during the September month. And, given the upcoming September FOMC meeting, following a hawkish Jackson Hole meeting in August where another 0.75% rate hike is currently priced with a 90% probability, markets could be setting up for another selloff opportunity!

Chart 1: Seasonality of S&P500 in September – Tends to be a nasty month.

Source: Bloomberg, Airo Malaysia

Table 2: Probability of 0.75% September Rate Hike – At 90%.

Source: Bloomberg, Airo Malaysia

Looking ahead, however, assuming inflationary pressure as proxied by PCE Deflator & CPI can continue to show signs of peaking, markets may take this as an excuse to engineer another relief rally towards the end of the year. PCE Deflator (year-on-year change) has declined in July to +6.3% since reaching its peak in June of +6.8%, albeit it is still churning at an elevated high level. If August figures (to be reported by the end of September) can continue to soften, it may just provide another respite to the equity market going into the last quarter of the year.

Chart 2: PCE Deflator – Year-on-Year Change Showing Sign of Peaking?

Source: Bloomberg, Airo Malaysia

Chart 3: CPI – Year-on-Year change peaked in June 2022 – at 9.1%?

Source: Bloomberg, Airo Malaysia

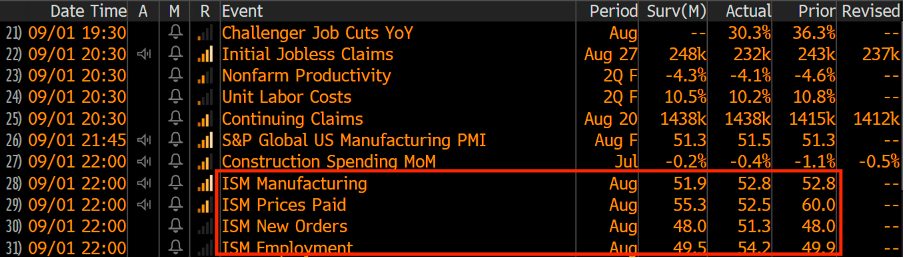

On the growth trajectory, August’s ISM Manufacturing PMI was flat at 52.8 versus July. However, ISM Orders has shown a slight improvement to 51.3 vs. 48.0 in July while ISM Employment saw a sizable jump to 54.2 vs. 49.9 in July. In addition, the ISM Price Paid has shown a continuous decline in the price pressure to 52.5 from 60.0 in July. If this macro growth can consistently continue, we may have seen an early green shoot in the U.S macro growth space. Otherwise, this could be just an isolated growth rebound event.

Chart 4: ISM PMIs – Flat for manufacturing but improvement in orders, employment & price

Source: Bloomberg, Airo Malaysia

Taking the above factors into consideration, Airo will likely be maintaining high cash levels towards the end of the year. However, we remain nimble in our approach and will seize opportunities if they arise, such as another relief rally if that is deemed probable. Our tactical allocation strategy will be titled towards a tactical long positioning (instead of a short) where we could take advantage of a possible year-end rally.

Sep 2nd, 2022

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.