CIO Letter – Sep 2023: A weakening U.S job market?

Highlights:

#1

For August 2023, Airo-BOCA composite was down -1.36% but outperformed MSCI All Country World Index (ACWI) and S&P500 Index (SPX) that were down -2.91% & -1.77% respectively. Airo’s outperformance was mainly attributed to its tactical short position in the U.S Technology sector.

#2

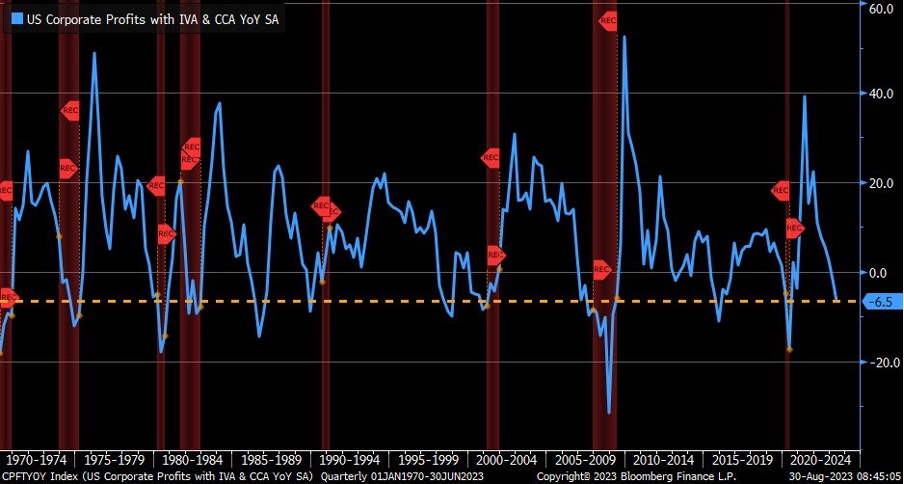

U.S corporate profit growth contraction accelerated to -6.5% year-on-year for the 2Q2023 reporting that was just completed. This was a worsening contraction from the 1Q2023 of -1.8% year-on-year. This trend highlights the alarming disparity between equity valuations and their underlying earnings growth trajectory.

#3

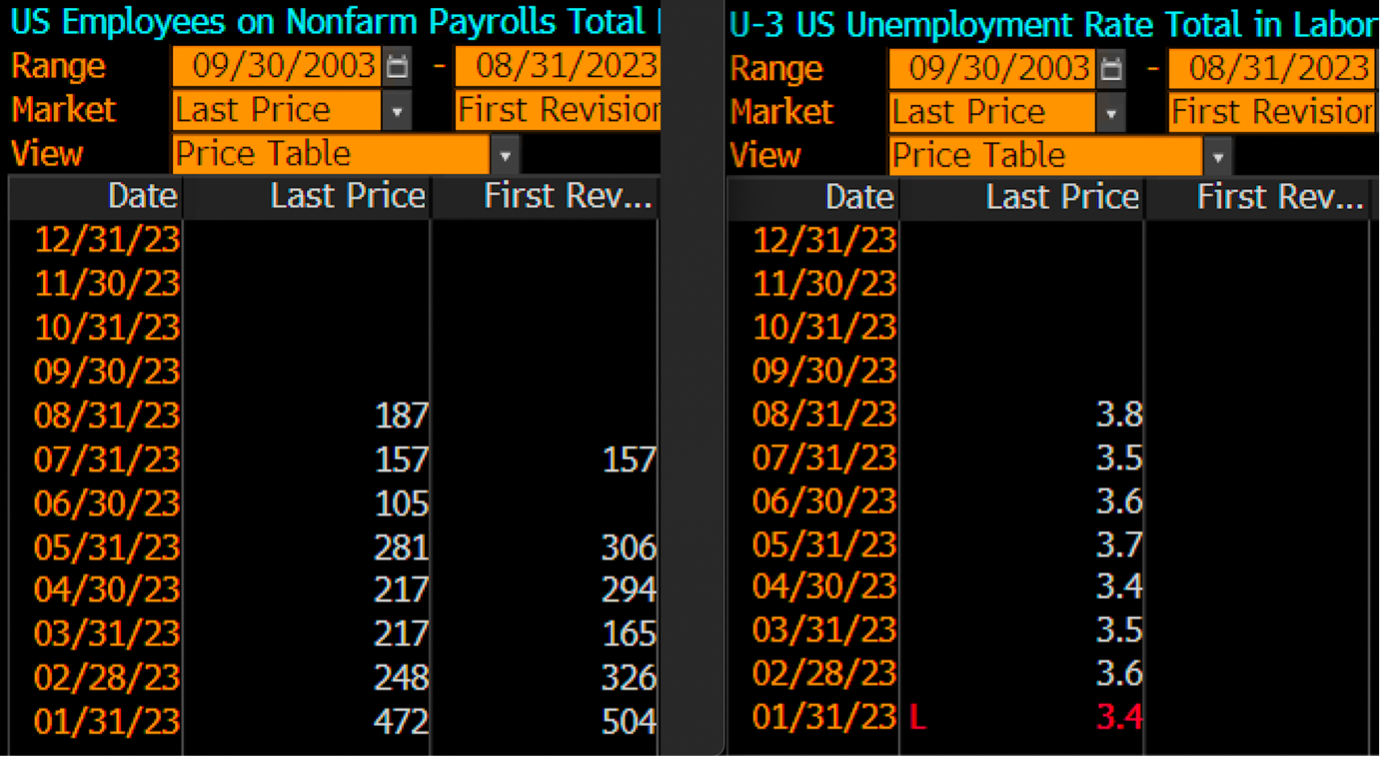

The Nonfarm Payrolls report indicated a softening in the U.S job market, with consecutive months of downward revision below the 200k mark. Coupled with the unemployment rate rising to 3.8%, there are increasing hints of a potential recessionary risk incoming.

#4

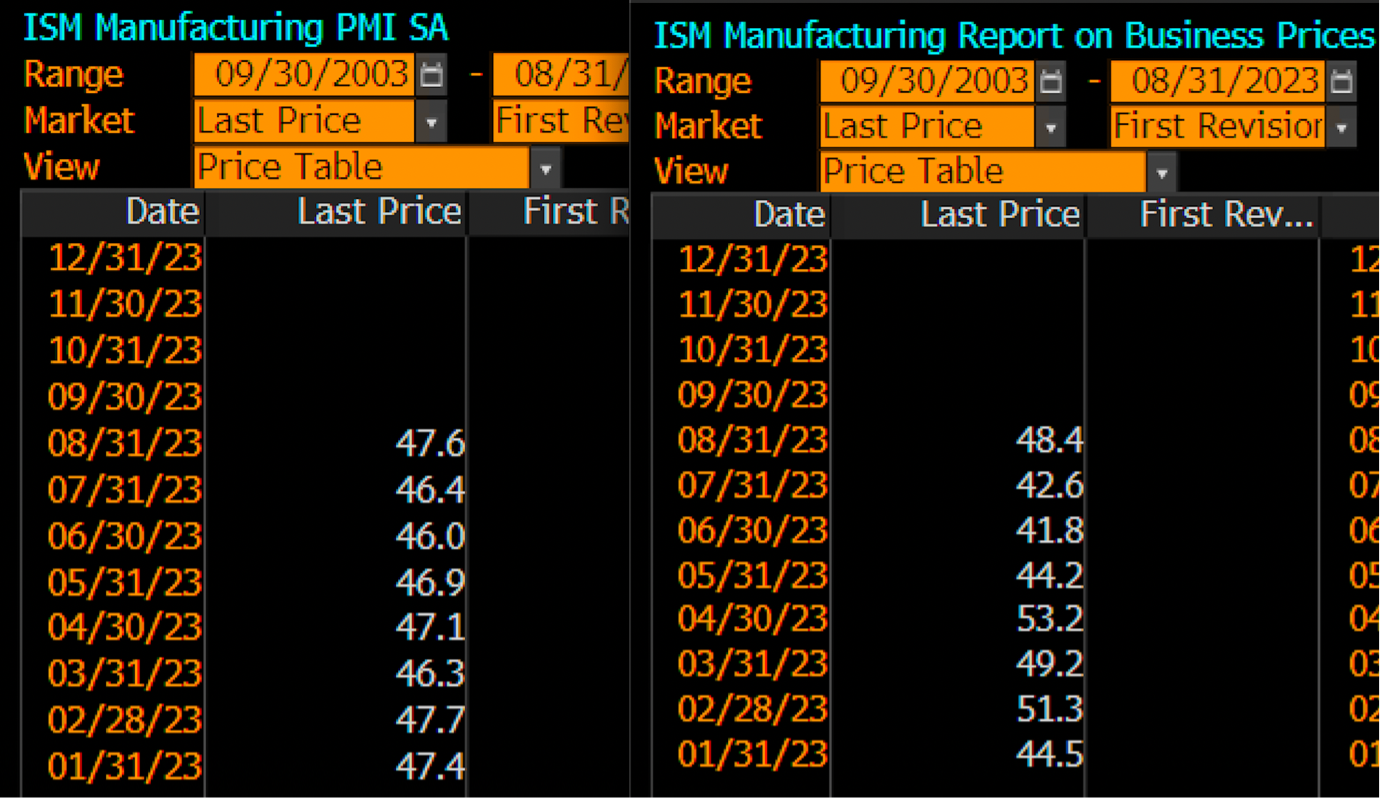

In August, the ISM Manufacturing PMI displayed modest growth. In contrast, the ISM Prices Paid experienced a significant increase, suggesting a likely price pressure within the manufacturing sector. Moreover, both the PCE Deflator and CPI saw an up-tick in their July figures, highlighting a potential resurgence of increased consumer price pressures.

#5

Airo is committed to maintaining agility in its asset allocation strategy to uphold the capital preservation of your investments. By vigilantly monitoring market conditions and adapting to changes, we aim to protect and enhance the value of your investments.

– – –

Dear Valued Investors,

For August 2023, Airo-BOCA composite was down -1.36% but outperformed MSCI All Country World Index (ACWI) and S&P500 Index (SPX) that were down -2.91% & -1.77% respectively. Airo’s outperformance was mainly attributed to its tactical short position in the U.S Technology sector.

Table 1: On a year-to-date basis, Airo-BOCA returned -3.82% (As of August 2023)

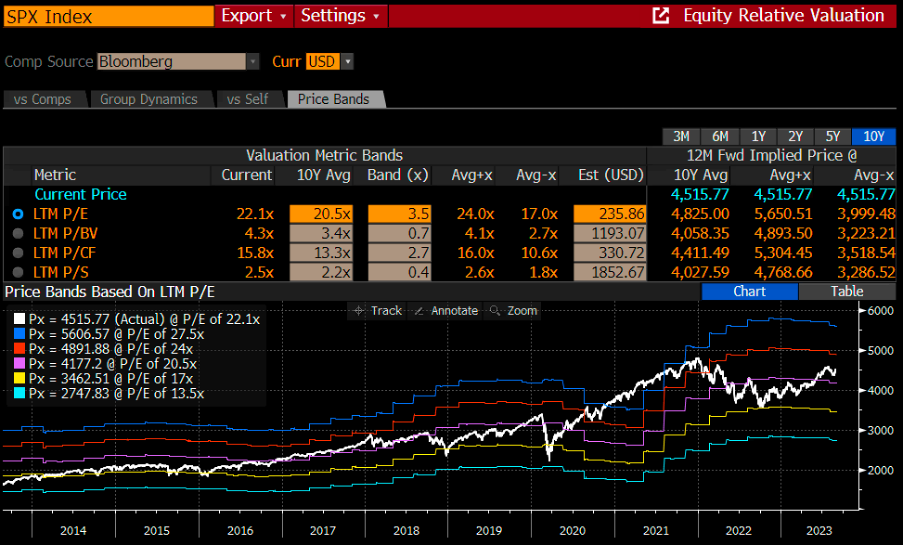

U.S corporate profit growth contraction accelerated to -6.5% year-on-year for the 2Q2023 reporting that was just completed. This was a worsening contraction from the 1Q2023 of -1.8% year-on-year. Using S&P500 index as a proxy for the U.S market, its current valuation at 22x PE remains pricey given the alarming disparity between equity valuation versus its actual earnings’ growth trajectory.

Chart 1: U.S Corporate Profit Growth ~ continued to contract at -6.5% yoy in 2Q2023

Chart 2: S&P500’s Valuation ~ remains pricey at 22x PE given the overall negative earnings’ growth

While August’s NFP has beaten its expectation at 187k, the underlying weakness in the job market is apparent as the July’s NFP was markedly revised down again to 157k from 187k after June’s big downward revision to 105k from 209k. These indicate a softening in the U.S job market, with consecutive months of downward revision below the 200k mark. Coupled with the unemployment rate jumping to its new high for the year at 3.8%, there are increasing hints of a potential recessionary risk incoming.

Chart 3: U.S Nonfarm Payrolls & U.S Unemployment Rate

The ISM Manufacturing PMI was muted in August at 47.6 i.e., a marginal growth from 46.4 in July. In contrast, the ISM Prices Paid experienced a significant increase to 48.4 from 42.6, suggesting a likely price pressure within the manufacturing sector. Moreover, both the PCE Deflator and CPI saw an up-tick in their July figures, highlighting a potential resurgence of increased consumer price pressures.

Chart 4: ISM Manufacturing PMI & ISM Manufacturing Prices Paid

Airo is committed to maintaining agility in its asset allocation strategy to uphold the capital preservation of your investments. By vigilantly monitoring market conditions and adapting to changes, we aim to protect and enhance the value of your investments.

Sep 5th, 2023

William Yii

CIO, Airo Malaysia

– – –

Disclaimer: Airo is a brand of BH Global Fintech Solutions Sdn Bhd (“BHFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. BHFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. BHFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by BHFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.