CIO Letter – Sep 2024: Expecting U.S. Equity Correction To Resume

Highlights:

#1

After the initial volatility from covering Yen short positions subsided, global equities staged a relief rally, finishing the month on a positive note. The S&P500 and MSCI ACWI were up 2.28% and 2.50%, respectively.

#2

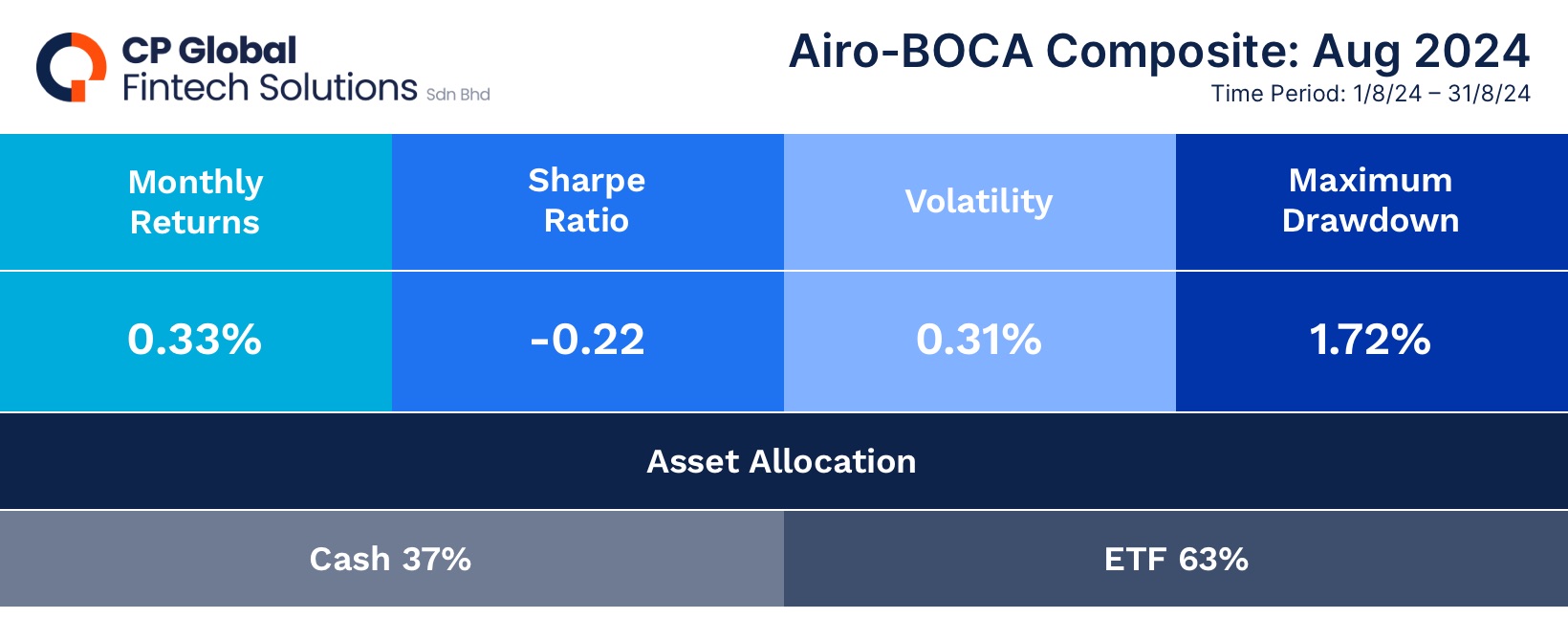

Similarly, the Airo-BOCA composite ended the month with a 0.33% gain. Key contributors to this performance included China, the agriculture sector, Japanese Yen, and bond holdings. However, the overall performance was weighed down by the hedging position in the U.S technology sector.

#3

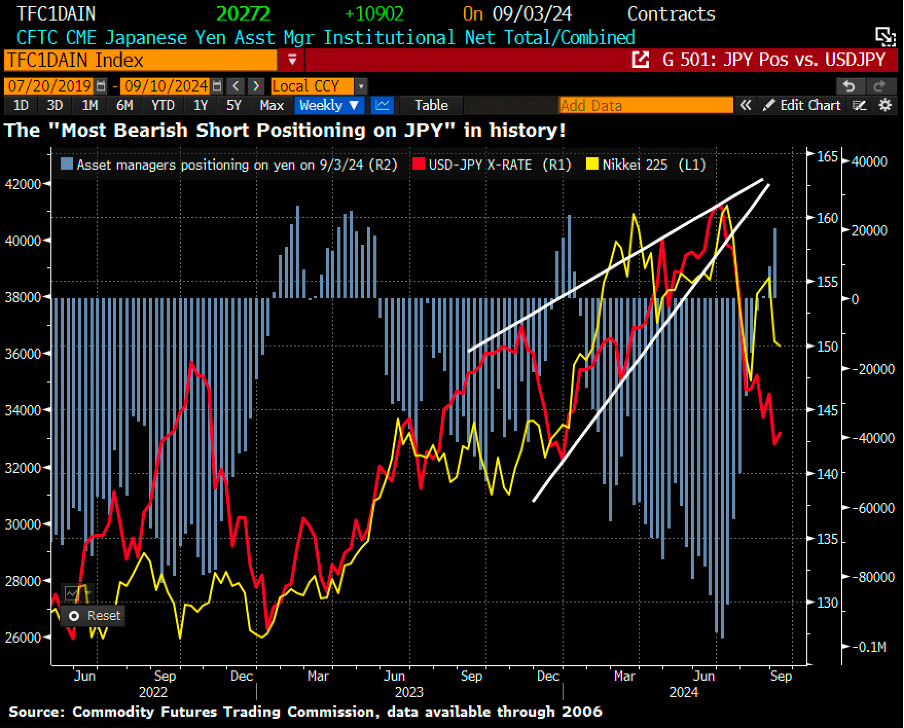

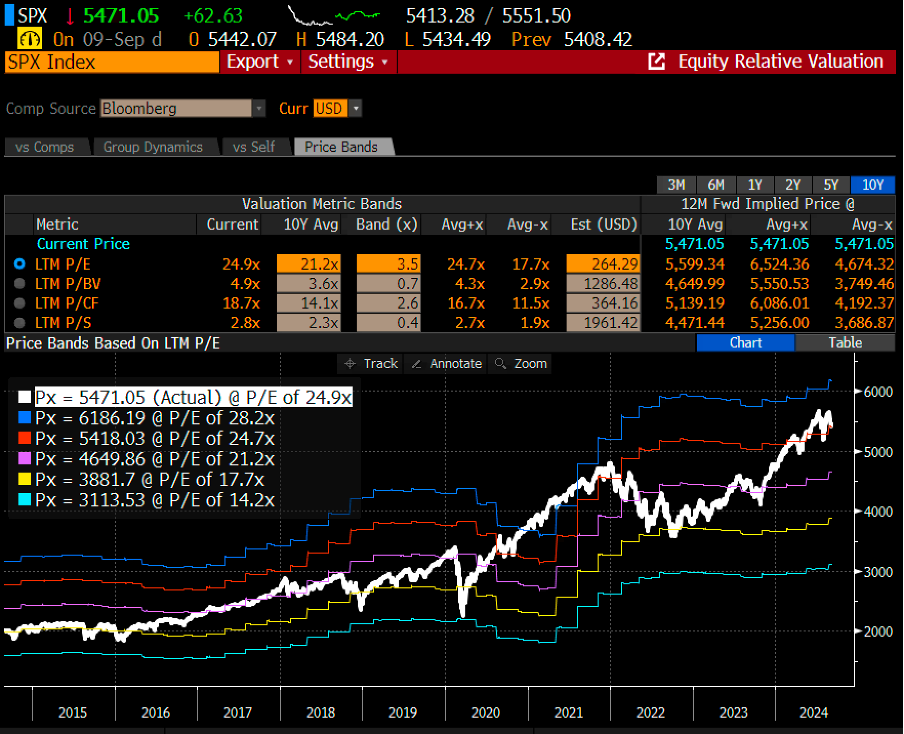

The short covering in Yen has actually shifted to a net long position, which could still have negative implications for global asset classes. From a valuation perspective, we maintain the view that the U.S equities, particularly the S&P500, remain pricey and have further room for correction in the near term.

#4

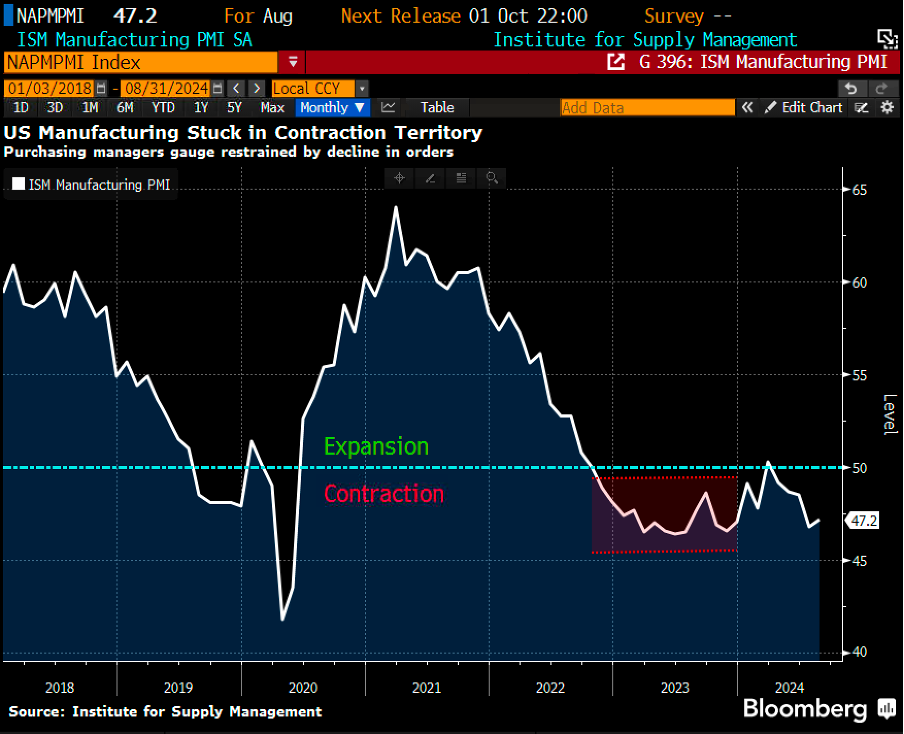

Looking ahead, the U.S. macroeconomic growth trajectory continues to show signs of reversal. The ISM Manufacturing PMI has contracted five consecutive months, while the labour market growth has also been steadily weakening.

#5

Given the potential deterioration of U.S. macroeconomic growth, Airo remains agile in managing its overall equity exposure and continues to diligently implement tactical hedging strategies.

– – –

Dear Valued Investors,

Global equities were initially negatively impacted by the massive volatility associated with the Yen short-covering trades. However, a relief rally followed shortly, with the S&P500 index and MSCI ACWI closing higher in August, at 2.28% and 2.50%, respectively.

As for the Airo-BOCA composite, it recorded a modest 0.33% gain in August, though the overall performance was dampened by the hedging position in the technology sector. Key contributors for the month’s performance included China, the agriculture sector, Japanese Yen, and bond holdings.

Table 1: Airo-BOCA Aug 2024 Performance (in USD)

As a result of the Yen short coverings, speculators have recently shifted to a net long position on the Yen. This indicates that the Yen may continue to strengthen, potentially exerting further negative pressure on global asset classes due to a continuing risk of global Yen carry-trade unwinding activities.

Chart 1: The massive Yen (JPY) short trades had just turned net long recently

From a valuation perspective, the S&P500 is currently trading at more than +1x standard deviation above its 10-year historical average P/E range. Given the negative macroeconomic backdrop, we maintain our view that the U.S equities have further room for correction in the near term.

Chart 2: S&P500 has further room for correction

On the U.S macro front, the ISM Manufacturing PMI saw its fifth consecutive month of contraction, indicating a consistent downward trend in manufacturing activities.

Chart 3: U.S ISM Manufacturing PMI saw its fifth consecutive month of contraction

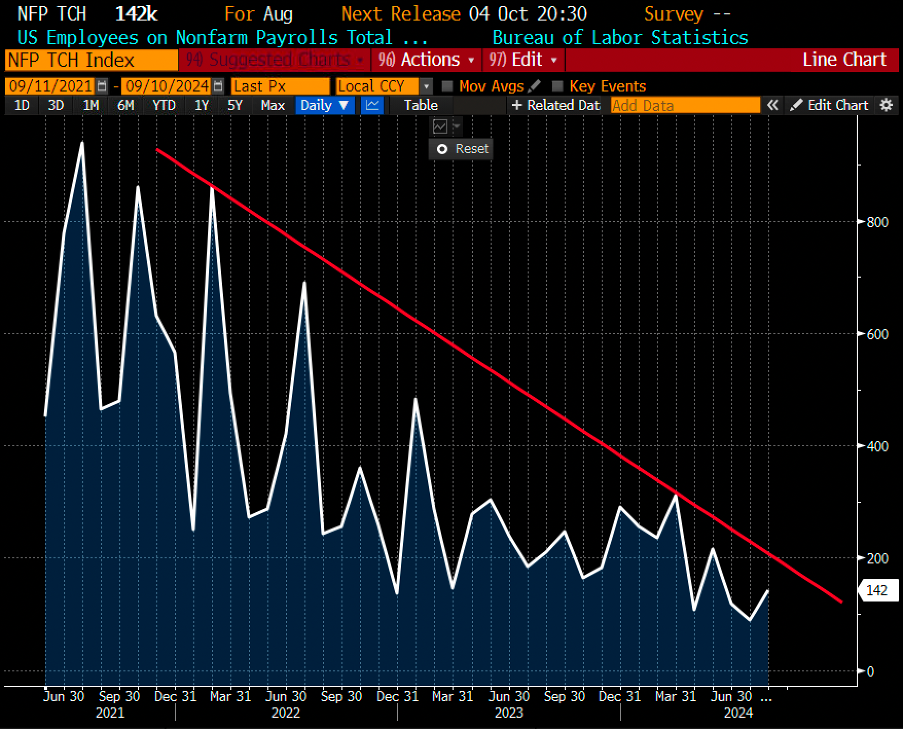

Although the U.S’ Nonfarm Payrolls showed a net gain of 142,000 in August, the employment figures for June and July were revised downward by 89,000. This significant revision suggested that the labour market has been weaker than initially reported and may be subjected to further downward adjustments in the coming months.

Chart 4: NonFarm Payrolls trending lower continuously

In short, given the potential for continued deterioration in U.S. macroeconomic growth, Airo remains agile in managing its overall equity exposure and continues to diligently implement tactical hedging strategies.

September 10th, 2024

William Yii

CIO, CP Global Fintech Solutions

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realized by you.