CIO Letter – Sep 2025: Positive Sentiment Continues

Highlights:

#1

The U.S. interest rate cut expectation continued to drive the global equity rally in August 2025. The S&P500 and ACWI Index ended July with gains of +1.91% and +2.36% respectively.

#2

The Airo-BOCA Composite gained +2.81% in August, driven mainly by exposure to gold miners and the solar energy sector, from which we subsequently took profit in September. We also closed our short position in the technology sector and shifted the allocation into the same sector. The Airo-Shariah Composite gained +2.13% in August, with performance supported by the U.S. equity market and exposure to the healthcare sector.

#3

In the near term, positive sentiment may persist, driven mainly by expectations of U.S. interest rate cuts amid a weaker labour market. At the September FOMC meeting, the U.S. Fed. resumed its rate-cutting cycle with a 0.25% cut and signaled two additional 0.25% cuts by year-end.

#4

China’s A-share equity market also rose strongly in August (+11.4% in USD terms), fueled largely by cash-rich investors seeking better returns in equities over bonds as China’s interest rates continue to drift lower. On the macro front, the Chinese government remains supportive with various stimulus policies aimed primarily at boosting domestic consumption.

#5

Looking ahead, while global equities may continue to climb, we will closely monitor macro growth and inflation risks that could alter underlying market conditions.

—

Dear Valued Investors,

Expectations of U.S. interest rate cuts remained a key driver of the global equity rally in August 2025. The S&P 500 and ACWI Index closed July with gains of +1.91% and +2.36% respectively.

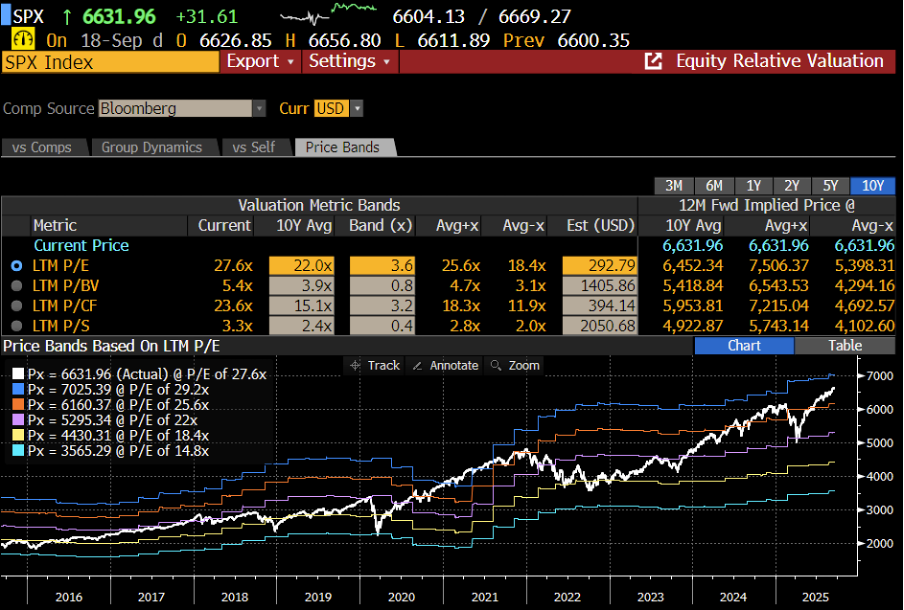

Chart 1: S&P500 is currently trading at 10Y average trailing PE band of 28x.

The Airo-BOCA Composite gained +2.81% in August, with strong returns mainly contributed by exposure to gold miners and the solar energy sector, from which we subsequently took profit in September. We also closed our short position in the technology sector and shifted the allocation into the same sector. The Airo-Shariah Composite gained +2.13% in August, supported by the U.S. equity market and exposure to the healthcare sector.

Table 1: Airo-BOCA Composite (Aug 2025) Performance in USD Term

Table 2: Airo-Shariah Composite (Aug 2025) Performance in USD Term

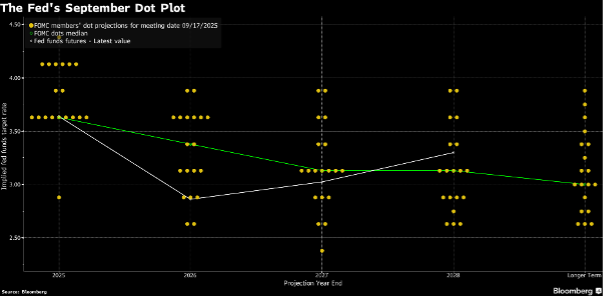

In the near term, positive sentiment may persist, driven primarily by expectations of U.S. interest rate cuts amid a weaker labor market. At the September FOMC meeting, the U.S Fed. resumed its rate-cutting cycle with a 0.25% cut and signaled two additional rate cuts of 0.25% by year-end. From a macro perspective, the rate-cutting cycle will remain a key driver of the equity market.

Chart 2: Fed’s September dot plot showed another two cuts of 0.25% are expected by the end of 2025

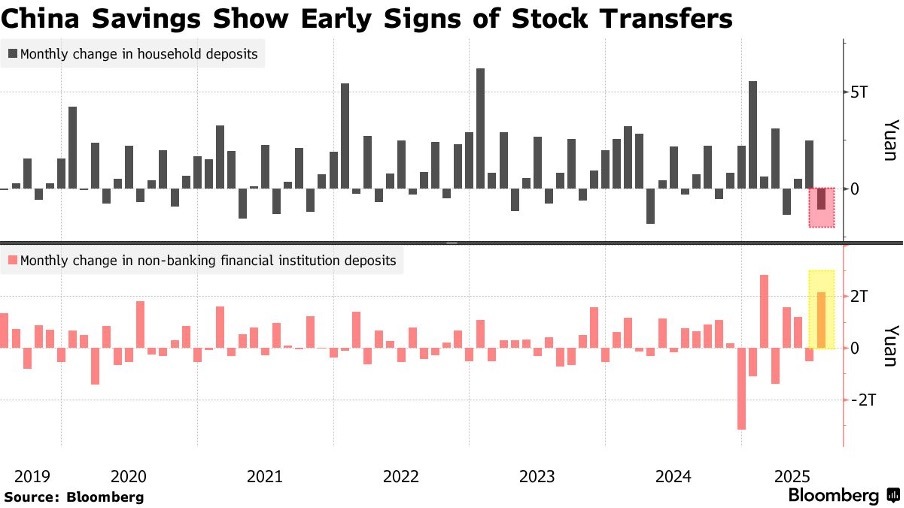

China’s A-share equity market also rose strongly in August (+11.4% in USD terms), largely fueled by cash-rich investors seeking better returns in equities over bonds as China’s interest rates continue to drift lower. On the macro front, the Chinese government remains supportive with various stimulus policies aimed primarily at boosting domestic consumption.

Chart 3: China A-share rose +11.4% in August driven mainly by high-net-worth clients

Chart 4: A green shoot of shifting from household’s savings into China equity market

Looking ahead, while global equities may continue to edge higher, we will closely monitor macro growth and inflation risks that could alter underlying market conditions.

September 19th, 2025

William Yii

CIO, CP Global Fintech Solutions

– – –

Disclaimer: Airo is a brand of CP Global Fintech Solutions Sdn Bhd (“CPFS”), licensed by the Securities Commission of Malaysia as a Digital Investment Management company. CPFS is authorised to carry out the business of fund management incorporating innovative technologies into automated discretionary portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. CPFS assumes no responsibility for liability for your trading and investment results. It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable, or that they will not result in losses. Past results of any trading system published by CPFS, are not indicative of future returns by that system, and are not indicative of future returns which will be realised by you.