Part 1: Laying the Groundwork – Understanding the Fundamentals of Retirement in Malaysia

In today’s fast-paced world, retirement may seem like a distant horizon, especially for the young workforce.

However, with Malaysians living longer and the ever-evolving financial landscape, starting early on retirement planning has never been more crucial. This article aims to break down the basics and introduce you to the primary pillars of Malaysia’s retirement system, all while showing how modern tools, like Airo, can make the journey smoother.

Why Retirement Planning Matters

First and foremost, we need to address the why.

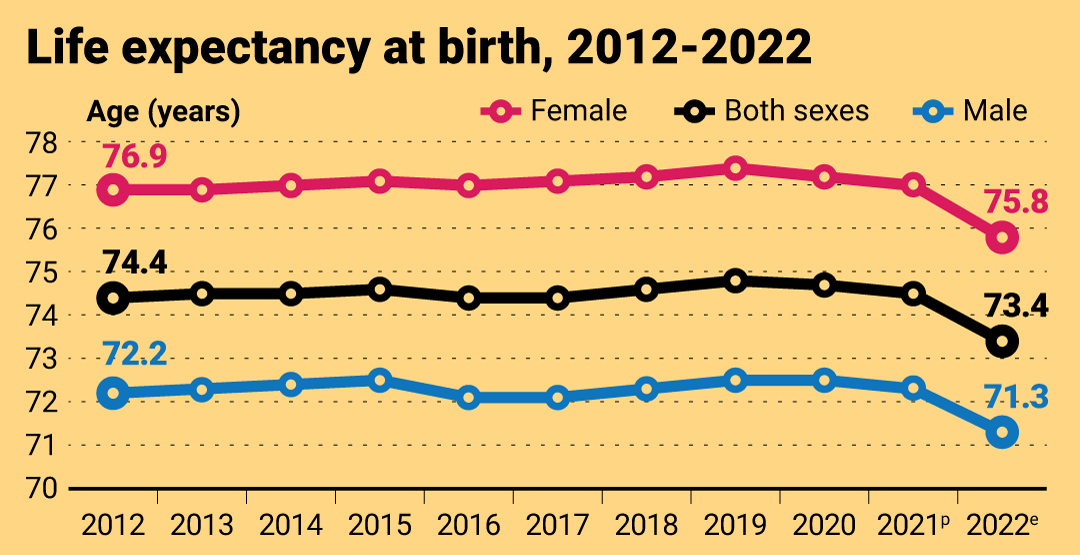

Despite the hit in the nation’s life expectancy due to the pandemic, Malaysians average life expectancy at birth is 71.3 years for males and 75.8 years for females.

How do we ensure that we have enough savings to last through our retirement years?

Consider this: the EPF suggests that to live comfortably in retirement, a Malaysian would need approximately RM2,700 monthly. That equates to a hefty RM648,000 to sustain oneself for 20 years in retirement.

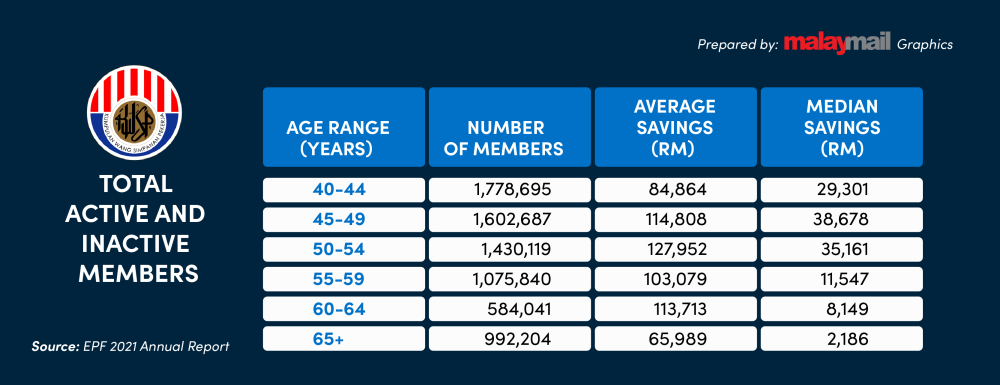

However, the EPF revealed that two million members aged between 40 and 54 have less than RM10,000 in their savings in their accounts.

Understanding the Malaysian Retirement System

When it comes to retirement in Malaysia, several key components anchor the system:

- Employees Provident Fund (EPF): Almost every working Malaysian is familiar with the EPF. As a compulsory savings scheme for salaried individuals, both the employee and the employer contribute regularly. It’s the primary retirement savings for most, but is solely relying on it enough? Given the above-mentioned figures, it’s clear that diversifying retirement strategies can be essential.

- Private Retirement Schemes (PRS): Think of PRS as a supplementary savings net. These voluntary contribution schemes offer diversified investment opportunities and come with the added perk of tax incentives.

- Government Pensions: Specifically for the civil servants among us, government pensions provide a steady post-retirement income, ensuring a degree of financial security.

Factors Influencing Retirement Savings

Several factors can shape the trajectory of your retirement savings:

- Expected Retirement Age: The standard age might be 60, but what if you wish to retire earlier? It means recalibrating your savings strategy.

- Lifestyle Expectations: We all have aspirations. Whether it’s traveling, pursuing a hobby, or living in a particular neighbourhood, these choices will influence how much you need to save.

- Medical and Healthcare Costs: It’s an unfortunate reality that as we age, we may face increased medical expenses. Anticipating these costs is crucial to avoid financial strain later.

- Inflation: Money’s value isn’t static. What RM10 buys today might be very different in 30 years. When planning, always account for inflation to ensure your savings maintain their purchasing power.

The Role of Modern Tools

Enter robo advisors, like Airo. These platforms harness algorithms to provide tailored financial advice. Designed to optimize returns while considering individual risk tolerance, they offer a fresh, tech-forward approach to managing retirement savings. With their efficiency, cost-effectiveness, and user-friendly interfaces, they’re rapidly becoming an essential tool in the modern retiree’s arsenal.

Conclusion

Retirement planning is not just a task for the future; it’s a journey that starts now. By understanding the fundamental pillars of Malaysia’s retirement landscape and leveraging modern tools like Airo, you’re setting the stage for a secure, fulfilling retirement.

Eager to dive deeper? The groundwork is just the beginning.

In ‘Part 2: Maximizing Your Golden Years: Smart Strategies for Malaysian Retirement Investments’, we’ll explore advanced strategies to grow your retirement funds, ensuring they work as hard for you as you did for them. Stay tuned for insights that could reshape your retirement landscape!